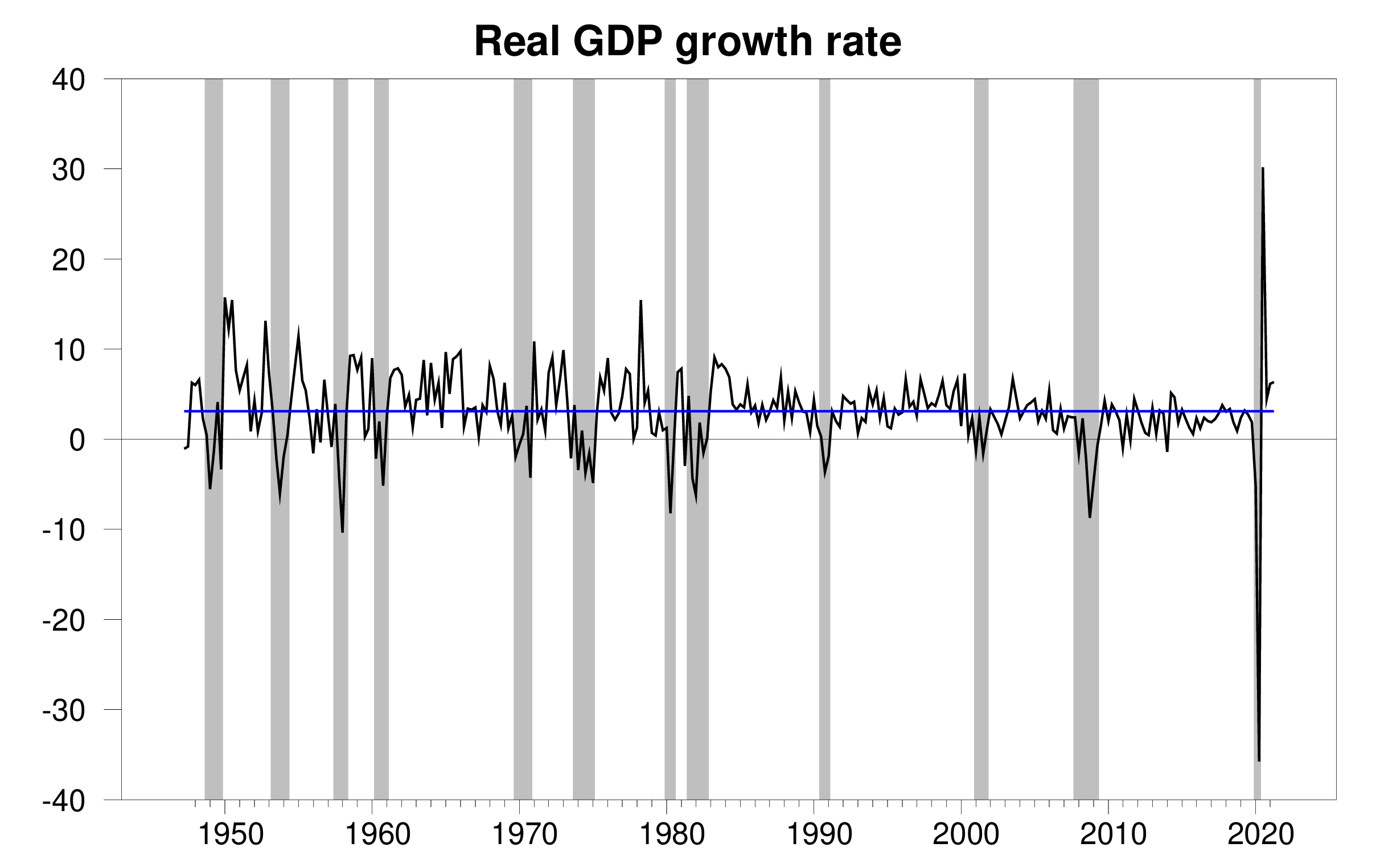

This Bureau of Economic Analysis It was announced today that the seasonally adjusted US real GDP growth rate for the second quarter was 6.5%. This is much higher than the US average growth rate of 3.1% between 1947 and 2019.Thanks to Patrick Higgins, an economist at the Federal Reserve Bank of Atlanta, for his Nowcasting 6.4% Meng Xi emphasized yesterday The nose is expected to be released today.

The annual real GDP growth rate, from the second quarter of 1947 to the second quarter of 2021, the historical average (3.1%) from 1947 to 2019 is blue. Calculated as 400 times the difference between the natural logarithm of GDP and the previous quarter.

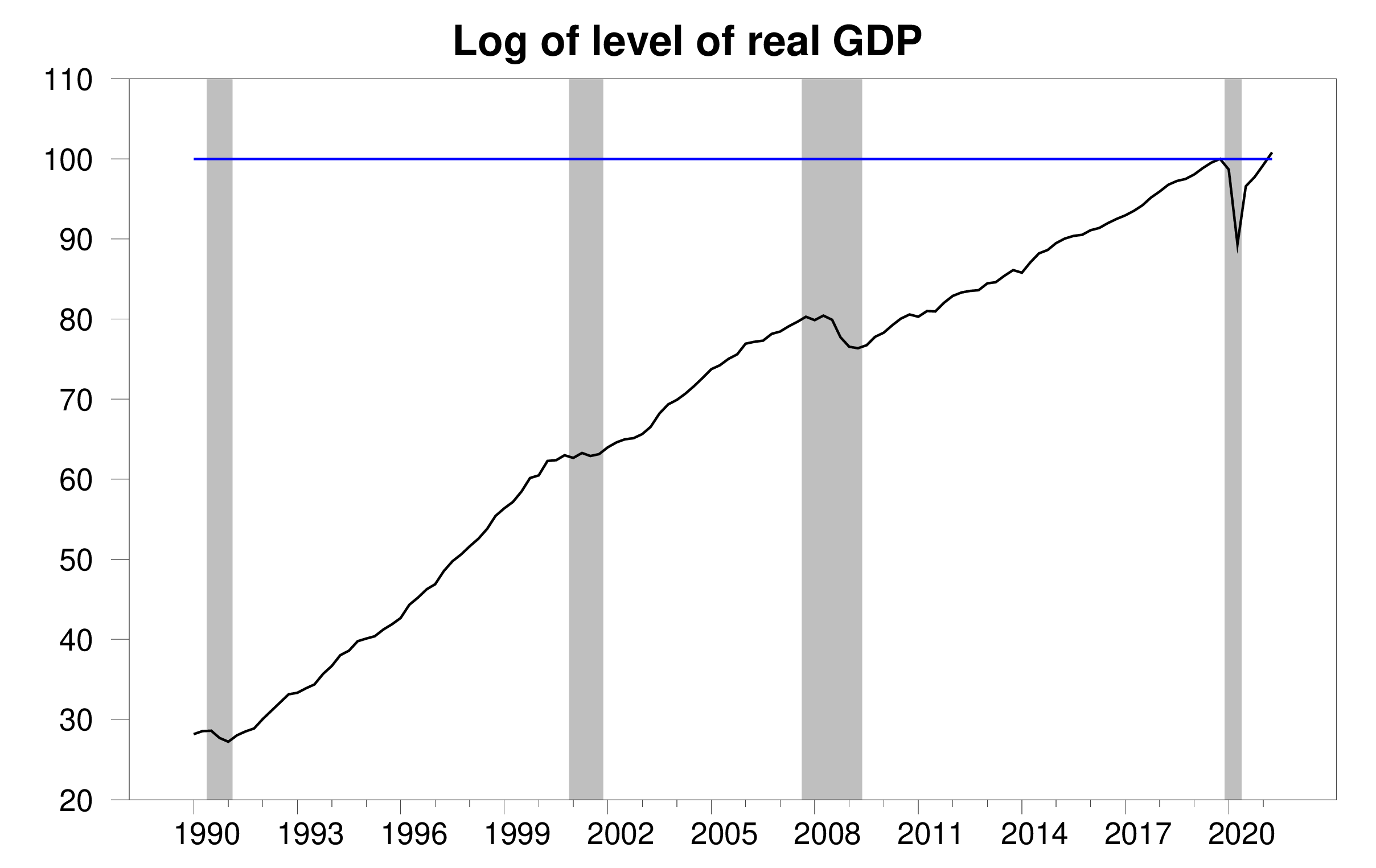

The growth in the second quarter brought GDP levels to a new high, 0.8% higher than the peak reached in the fourth quarter of 2019, before the COVID recession began.

100 times the natural logarithm of the real GDP level from the first quarter of 1990 to the second quarter of 2021, normalized to the fourth quarter of 2019 = 100. A movement of 1 unit on the vertical axis corresponds to a 1% change in the level of real GDP. The value for the second quarter of 2021 is 100.8, indicating that the real GDP in the second quarter of 2021 is 0.8% higher than the value in the fourth quarter of 2019.

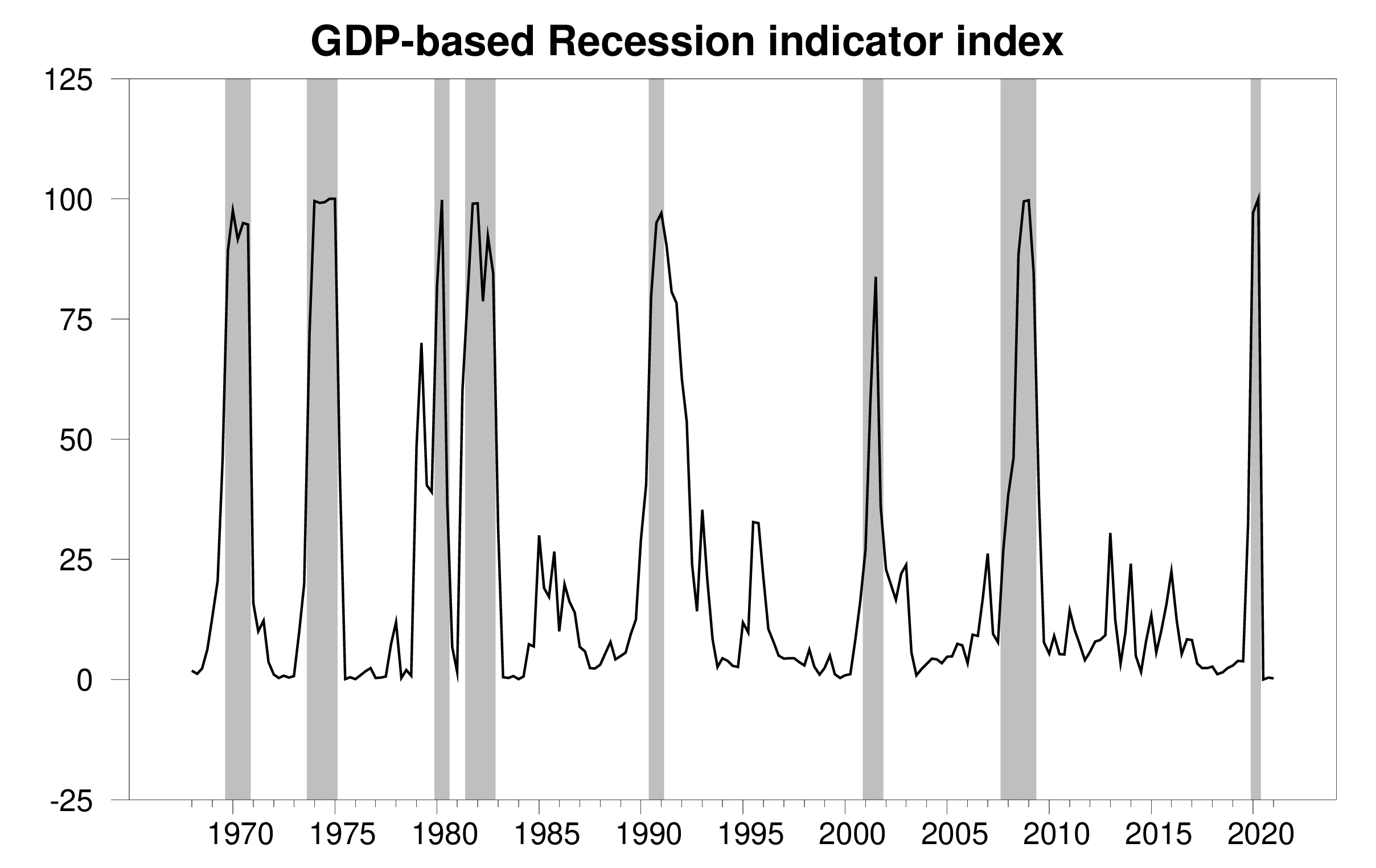

The new data shows Economic Browser Recession Index 0.2% is a very low value in history. The figure released today (0.2%) is an assessment of the economic situation in the previous quarter (i.e. the first quarter of 2021). We use the additional quarters to revise the data and obtain better accuracy. The index provides an automated procedure that we have implemented for 15 years to assign the dates of the first and last quarters of the recession.As we announced January 28, The COVID recession ends in the second quarter of 2020. The NBER Business Cycle Dating Committee subsequently July 19.

Index of recession indicators based on GDP. The plotted value for each date is based only on the published GDP figures up to one quarter after the specified date. The last date shown in the figure is 2021:Q1. The shaded areas represent the NBER decline dates, which were not used in any way to construct the index.

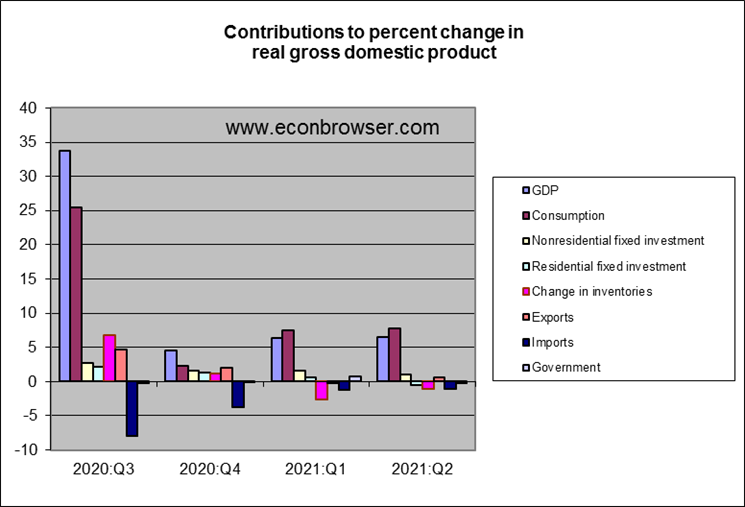

In terms of the breakdown of the GDP data for the second quarter, consumer spending is in a leading position under the stimulus of fiscal stimulus payments. It is a bit disappointing to see that residential fixed investment (from new home construction) actually fell in the second quarter. Monetary stimulus with low interest rates successfully stimulated housing price increases. Tobin’s Q investment theory predicts that this should stimulate new construction and promote GDP growth through this mechanism.

I have a new Research Papers In it, I think that potential GDP, I define it as the level of output that would be produced if wages and prices are fully flexible, not only depends on traditional factors such as available workers, capital stock, and production technology, but also depends on the specialization and specialization of these factors. Match between the configuration of product requirements. I see many statements that are consistent with the view that supply issues, not shortages of demand, are currently the key factors hindering overall growth.

{kind=link}

{kind=link}