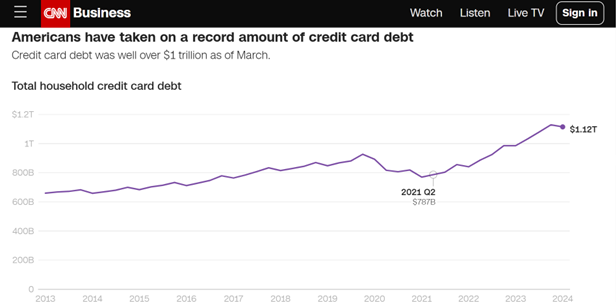

CNN published an article today titled “What happened to the U.S. economy?”. Most of the views are conventional, but one chart is interesting – Credit Card Debt:

source: CNN.

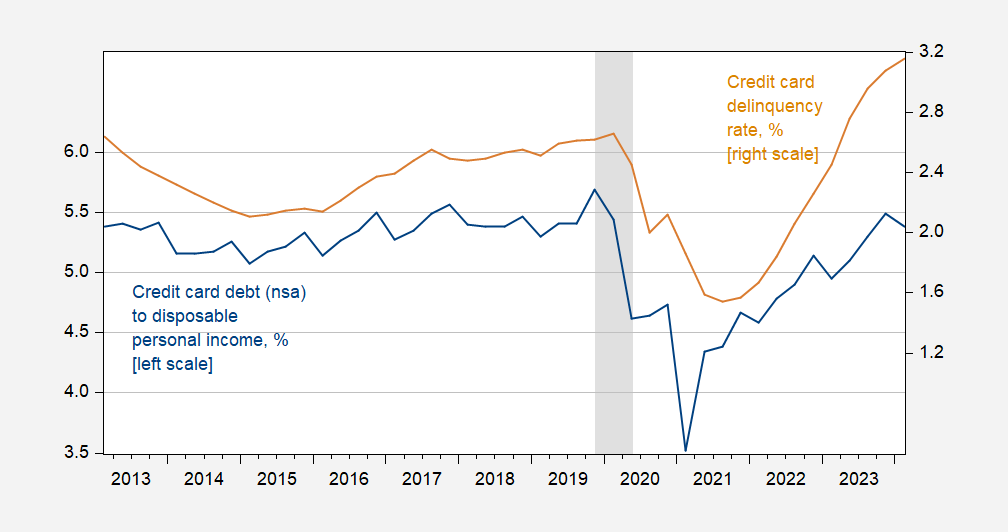

Aside from the usual complaint that this number is not normalized to personal disposable income (GDP), I find this an interesting metric. This is the normalized credit card debt and delinquency rate.

figure 1: Credit card debt (nsa) as a percentage of personal disposable income (blue, left axis), and credit card delinquency rates for all commercial banks, % (tan, right axis). NBER-defined recession peak-to-trough dates are in gray. source: Fed; Fed and BEA via FRED, NBER and author's calculations.

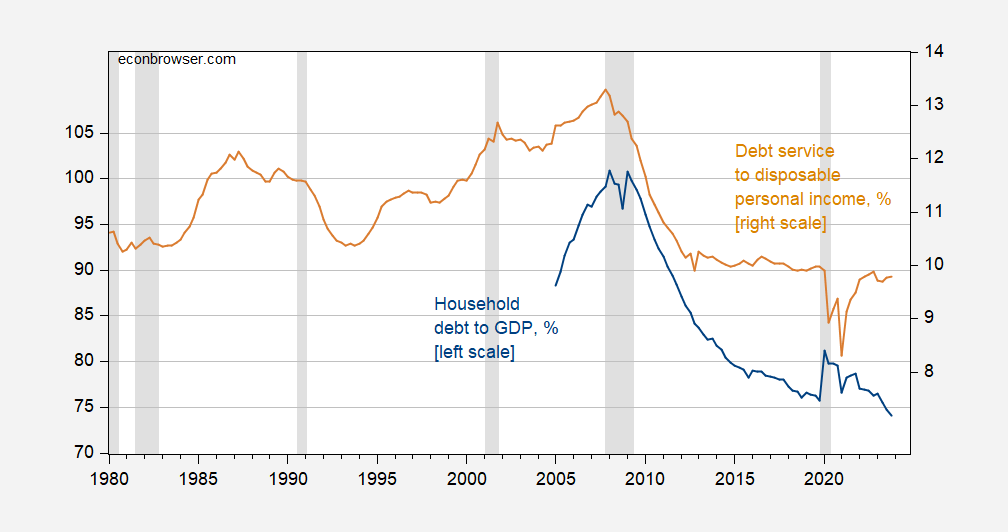

As a result, normalized credit card debt fell in the second quarter, but delinquency rates rose. This suggests that, although household debt to GDP ratios and household debt service to disposable income ratios are falling, for some groups something is happening.

figure 2: Household debt as % of GDP (blue, left scale), debt service ratio as % of disposable income (tan, right scale). NBER-defined recession peak-to-trough dates are in gray. Sources: International Monetary Fund (via FRED), Federal Reserve (via FRED), NBER.

Due to the prevalence of fixed-rate mortgages, debt payments are likely to remain the same even if interest rates rise. The credit crisis may therefore be more pressing for some income groups than others.

{kind=link}

{kind=link}