That is a Quote from Ecobrowser reader Who is wrong on almost all issues related to economics, but to me, it seems useful to provide empirical evidence about futures as a predictive indicator, especially in recent postal Rising commodity prices put upward pressure on the inflation rate. In addition, over time, the efficiency of the futures market may change and become more financialized.

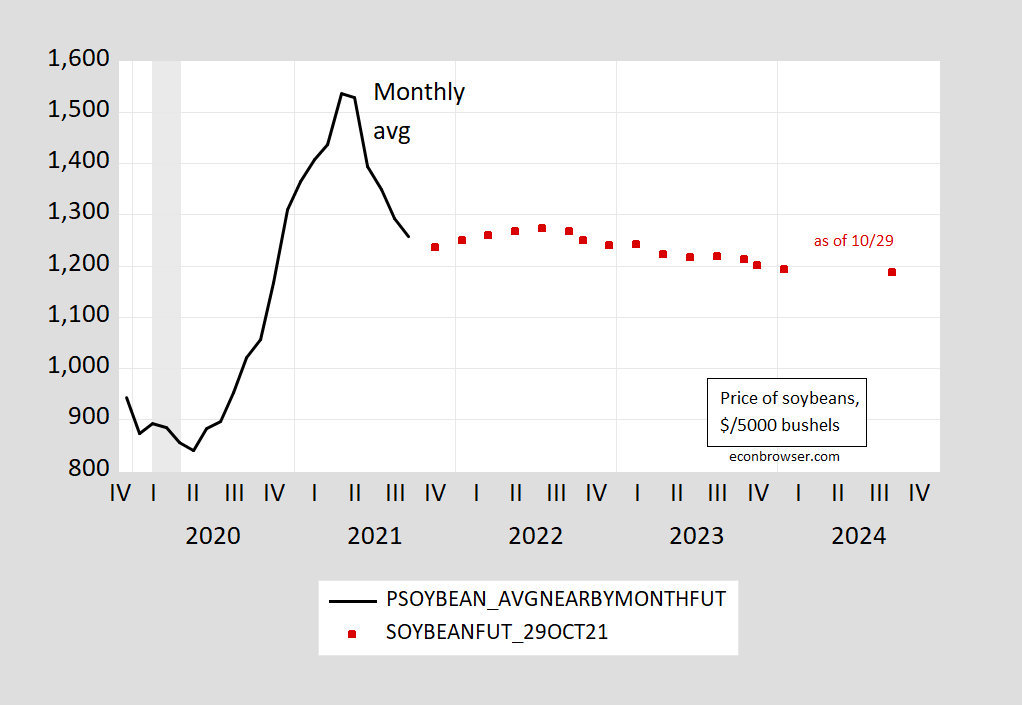

figure 1: Soybean prices, recent month futures, monthly averages of daily data (black) and soybean futures prices as of 10/29 (red squares) are all calculated in $/5000 bushels. source: Investment Net, ino.com (Accessed October 30, 2021).

Before, I noticed that Olivier Coibion and Olivier Coibion (JFutures Market Magazine, 2014), in which we evaluate-and other commodities-soybean prices. V. Fernandez (Resource Policy, 2017) We have updated our work. Kwas and Rubszek (forecast, 2021) The forecasting capabilities of futures as of March 2021 have been checked (sampling from 2000) (but no soybeans have been checked).

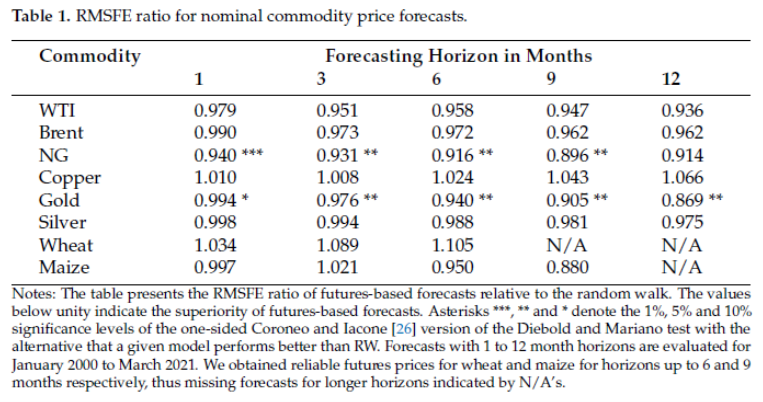

Table 1 shows the ratio of the root mean square prediction error (RMSFE) of futures to random walk. A value less than 1 indicates that futures is better than a random walk, and an asterisk indicates significance (one-sided test).

source: Kwas and Rubszek (2021).

Note that, with the exception of natural gas and wheat, futures perform better than random walks.

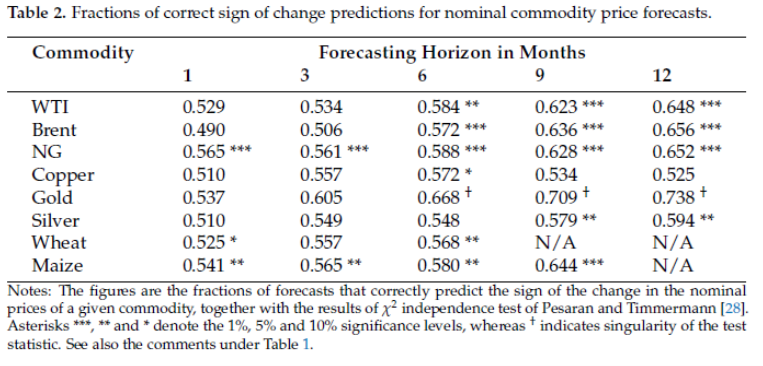

Another traditional method of evaluating predictive performance is to see if the indicator indicates the correct direction of change. When the statistic in Table 2 is greater than 0.50, then futures is better than a coin toss; the asterisk again indicates statistical significance.

source: Kwas and Rubszek (2021).

Please note that with one exception, the correct direction of futures forecasts and no change forecasts. Admittedly, not all instances are statistically significant—but there are quite a few instances that are statistically significant.

As I mentioned earlier, neither of these two studies specifically looked at soybean futures. However, in a 2019 paper (Yellow, Sierra, Garcia, Euro. Pastor agriculture. economy.) [ungated working paper version], The author wrote:

Using quantile regression, we evaluated the forecasting performance of soybean complex futures prices. Compared with the mainstream methods that only focus on the measurement of central tendency, this program provides a more complete forecast distribution map. The forecast performance varies depending on the location of the futures price distribution. Futures forecasts perform well in the center of the distribution. However, the futures price tends to be overestimated when the futures price is high, and underestimated when the futures price is low, which indicates that the futures price tends to underestimate the reversal of the price to the center of the distribution. When the futures price is high, the forecast error is greater.

At that time Reader CoRev is discussing the amount of information on soybean futures, The price is 814, placing the price at the upper end of the lower price range, that is, roughly in the center of the distribution, is where the author finds soybean futures to be a relatively good predictor of future soybean prices.

{kind=link}

{kind=link}