The debt servicing cost does not need to keep the prime minister awake at night, maybe the environment should collapse?

Not long ago, the state of public finances was considered to be given to the Minister of Finance Rishi Sunak “Sleepless night”, As he struggled with Britain’s growing debt levels and how to repay all debts.but Then it becomes clear The Bank of England is funding the Coronavirus Act, almost in the blink of an eye, as if the devastating cuts in public spending over the past decade may have been futile, and the public finances that we have been told may be flawed, or worse, by politics. Tamper to prove its rationality Narrow ideology.

With the drop of a penny, most public commentaries are beginning to feel that debt and deficits (the negative difference between government revenue and expenditure) are not as good as The actual cost of debt repayment (That is, the interest we paid for the debt). Net interest payments fell fourfold, from 3.8%-81 of gross domestic product (GDP) in 1980 to 0.9% in 2020-21, although the debt-to-GDP ratio increased from 40% to 97% during the same period.

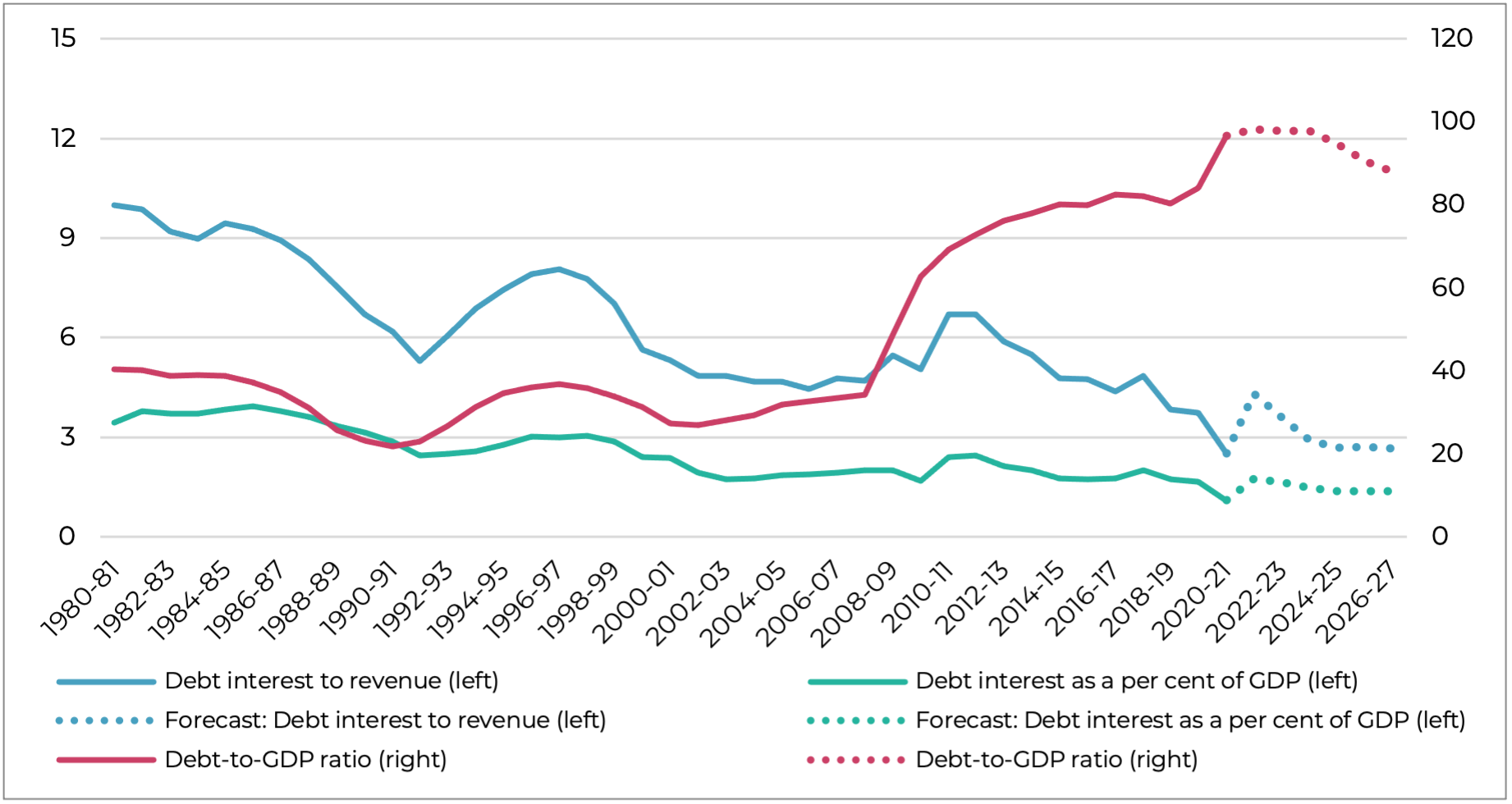

Government debt servicing costs are at historically low levels

Government interest payments: total and net asset purchase facilities (APF) as a percentage of GDP, from 1955 to 2026

Source: OBR 2021 and the author’s own calculations

But many people still believe that although borrowing costs have reached historical lows, the situation is still very fragile, because the potential rise in inflation and the rise in the relevant interest rate of the Bank of England (BoE) will increase the government’s debt servicing costs. This is why the government’s goal is Reduce the level of borrowing. E.g, Borrowing in the next five years It is expected to be 6% lower than the March 2021 estimate.Therefore, the government will only Deployed a net zero of 25.5 billion pounds Expenses between 2021-22 and 2024-25, when should they be spent At least £30 billion per year.

To some extent, the government’s debt servicing costs may increase because the interest rate paid by certain government borrowing instruments (index-linked Phnom Penh bonds) is linked to inflation (as inflation increases, government debt payments will also increase ). At the same time, the government’s public finances are more sensitive to rising interest rates because the Bank of England pays interest on the central bank reserves it creates (the Bank of England’s policy interest rate)—that is, it currently represents the 895 billion pounds of currency created through it. Pay 0.1%. Quantitative easing plan. If it raises interest rates to help control inflation, say 0.25%, it will have to pay more interest to banks holding central bank reserves.

All this means that the cost of government interest services is more sensitive to changes in interest rates and inflation.Earlier this year, in the Prime Minister’s Fall budget speechSome people suggest that inflation and a 1% rise in interest rates will increase debt service costs by 23 billion pounds.Taking into account higher inflation and interest rate expectations in the future, the Office of Budget Responsibility now predicts that debt servicing costs will rise to the total 40 billion pounds in 2022 and 2023.

Although these numbers should not be taken lightly, there are many reasons why we should not rush the panic button.

First of all, these numbers are A little misleading If it is not expressed in terms of the proportion of economic scale and/or the percentage of taxes (which indicates debt affordability) and the broader historical context. Debt service costs in 2022 and 2023 will still account for only 1.6% and 1.7% of GDP in the economy, and 4.3% and 3.6% in tax revenue respectively-similar to 2018-2019 levels, but still lower than The time of the first three centuries of any period (see picture below). In fact, despite inflation and rising interest rates, debt servicing costs will still account for three times the proportion of the economy and taxes compared to the early 1980s.

This shows that by supporting low-carbon transitions and high-paying green jobs, there is more room for borrowing to enable the economy to achieve full output capacity.

Expenses and debt have risen sharply, but the amount spent on debt financing has fallen

Left hand side: The ratio of government interest payments to net asset purchase instruments in GDP (%) and the ratio of debt interest to government revenue.Right: Debt to GDP ratio (%), excluding the Bank of England, 1980-2026

Source: OBR 2021 and the author’s own calculations

A separate question is whether interest rates will have to rise because of their sudden appearance. Loss of investor confidence. It seems Extremely unlikely In view of the fact that the financial market is currently very keen to provide loans to the British government.Indeed, in It recently sold green gilts for £6 billion Due to maturity in 2053, the UK Debt Management Office (DMO) has received £74 billion in subscriptions. In other words, the number of bids received by the DMO in the Ministry of Finance auction is 12 times the number sold-there is no shortage of demand there!

At the same time, what if the Bank of England decides to raise interest rates? The first answer is that banks should not raise interest rates, especially if they should not exceed the OBR forecast- To deal with supply-side crises that are largely affected by external conditions And give The fragility of the British economic recoveryInflation is not driven by domestic pressures—for example, wage increases (see chart below), and may be temporary.The central bank will raise interest rates Doesn’t help solve global supply Or reduce any pain caused by the labor shortage associated with Brexit. Conversely, for households that have felt price increases, energy prices soaring, and living standards decline, this will translate into higher costs and will increase business costs, weaken economic recovery and possibly increase unemployment. The Eurozone raised interest rates prematurely after the 2008 global financial crisis and learned a bitter lesson. It would be foolish to make the same mistake.

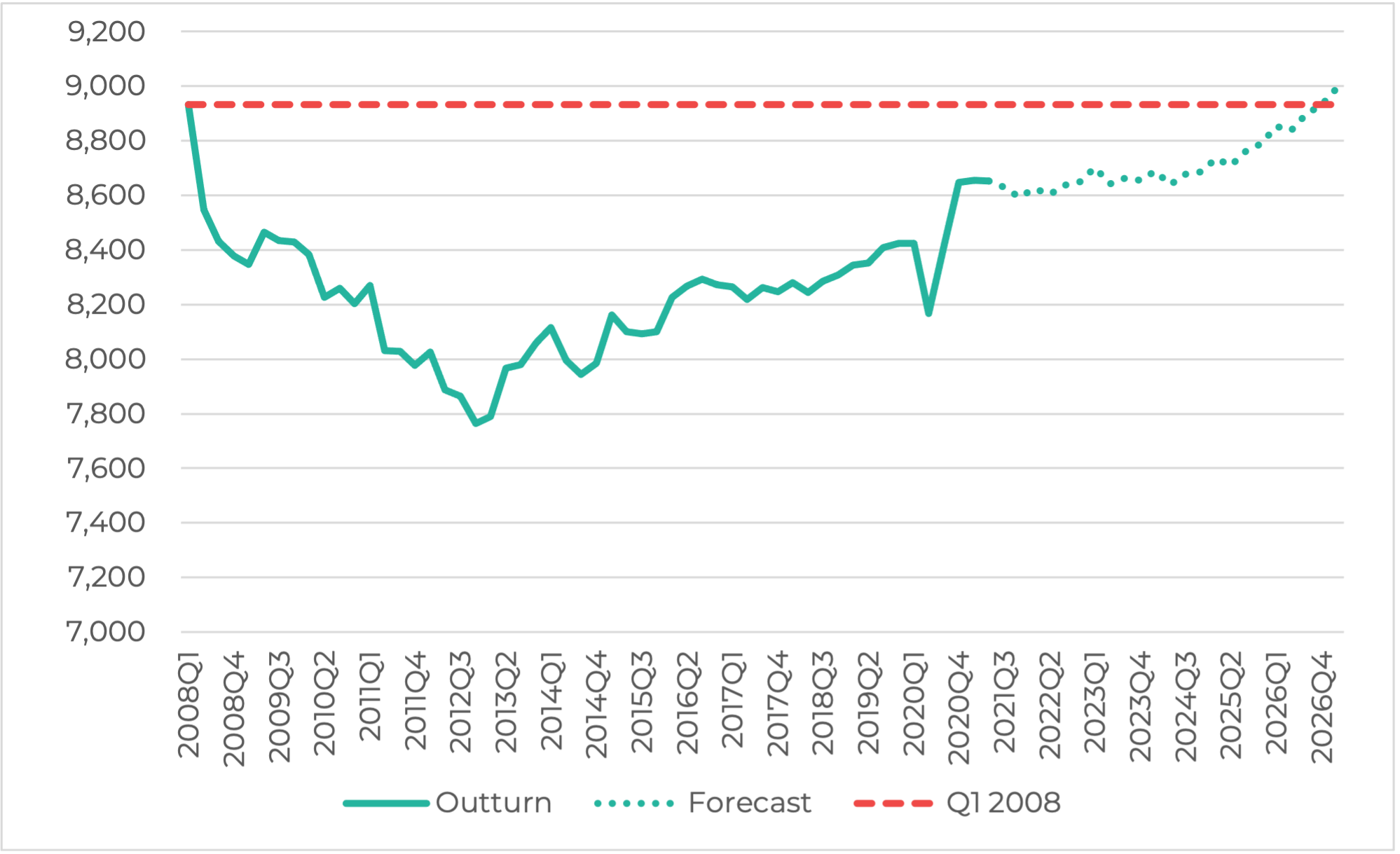

Inflation is not driven by continued domestic pressure, and may be temporary

Average revenue (GBP in billions, prices in the third quarter of 2021), from the first quarter of 2008 to the first quarter of 202

Source: NEF calculations based on OBR supplementary data, October 2021

However, the situation in which the benchmark interest rate rises beyond the OBR forecast is a situation in which the economy is recovering, employment and household income increase, and overall demand is boosted. This means that tax revenues have increased, while unemployment and other income transferred to the private sector have decreased at the same time.If necessary, the Bank of England can deploy other Credit Guidance Tool To curb aggregate demand, otherwise the Ministry of Finance can increase taxes when needed.Finally, as the forthcoming NEF working paper indicates, the Bank of England may move towards Hierarchical reserve system, Which greatly reduces the government’s debt servicing costs.

Inflation and its impact on debt service costs should not be taken lightly. But for now, these problems can be managed even if they cannot be resolved.The environmental emergency is in front of us, and there is a serious shortage of green investment, which will only make us pay more In the long term – There are other more pressing issues that keep us awake at night.

{kind=link}