As pointed out Jeff Frankel:

In terms of what the president can actually control to reduce inflation, one tool that has been overlooked is trade policy. Former President Donald Trump imposed these tariffs on aluminum and steel and all the goods we import from China-all kinds of goods. Tariffs raise prices for consumers. In my opinion, removing these obstacles is easy. Biden should be able to make China and other countries equal to lower some of the barriers to us. But whether that is the case or not, the removal of tariffs may immediately reduce consumer prices and the prices of steel and aluminum companies and various inputs. This is the fastest thing the government can control.

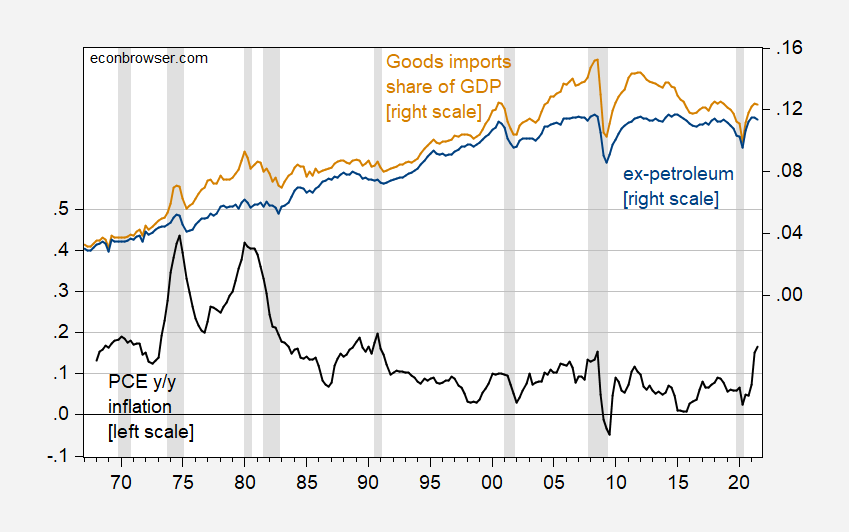

Related to the discussion of inflation, one of the differences between the 1970s and 2020s is the degree of openness of the U.S. economy:

figure 1: Personal consumption expenditure deflator index inflation, year-on-year (black, left scale), and the share of merchandise imports in GDP (brown, right scale), and the share of merchandise imports other than oil in GDP (blue, right scale). NBER-defined recession dates are shaded gray from peak to trough. Source: BEA 2021Q3 advance release, NBER and author’s calculations.

Before the inflation spike in 1974, imports of non-oil commodities accounted for approximately 4.1% of GDP (third quarter of 1972). Before the trade war, the ratio was 11.4% (first quarter of 2018).Although it is not clear whether external influences will always ease inflation-after all, the prices of our trading partners may rise faster (or may The narrowing world output gap is now more important), otherwise the dollar may depreciate. However, if it is not entirely or mainly dependent on domestic suppliers and foreign suppliers are exerting competitive pressure, then opening up tends to reduce inflationary pressures.At least, if quotas and tariffs and their combinations do not limit competitive pressure from abroad, it would be more real (see this postal; It’s not that changes in import prices will translate into a broader price index, but for Iron and steel, This is implied).You can also take a look Fran and Pierce (2019) The estimated impact of tariff barriers on producer prices in 2018.

For me, removing the Section 232 tariffs, which are mainly aimed at US allies (mainly gifts to US Steel), should be a breeze.

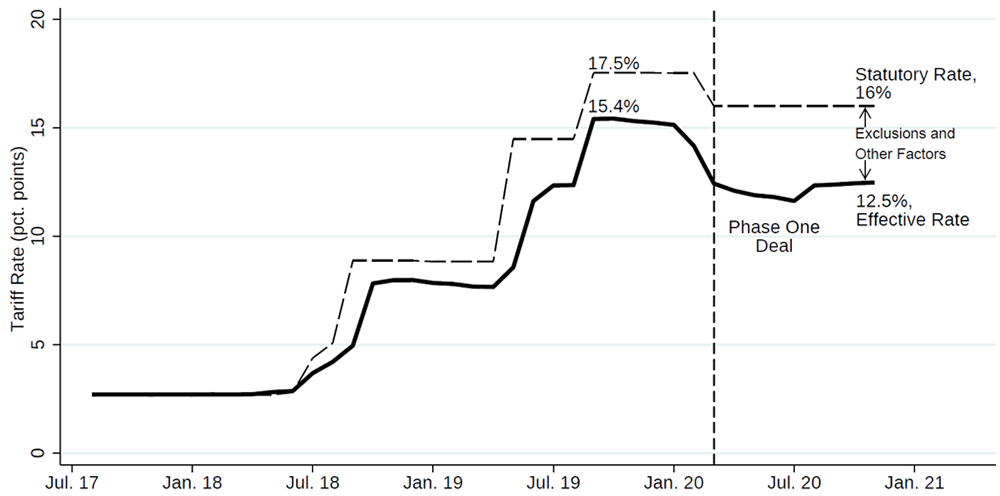

By the way, this is an interesting graph showing the effective tariff rate for imports from China, from Fran, Langmeier and Pierce (2021) (The new tariff is the 301 tariff because most steel/steel imports from China have already been sanctioned by anti-dumping/countervailing measures).

{kind=link}

{kind=link}