With the earlier recovery of industrial production and the slight acceleration of consumption growth, NBER is a key indicator that follows closely. BCDC Looks better than or even better A week ago.

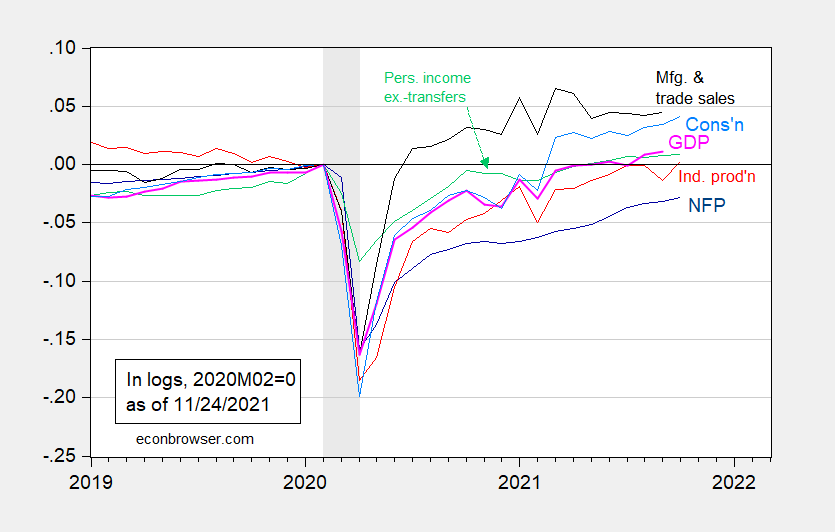

figure 1: Non-agricultural employment (dark blue), industrial production (red), excluding personal income transferred in 2012 (green), manufacturing and trade sales in 2012 (black), consumption in 2012 (light blue), and Ch .2012$ monthly GDP (pink), all logarithms are normalized to 2020M02=0. NBER defines the date of the recession, from peak to trough, in shades of gray. Source: BLS, Federal Reserve, BEA, calculated by FRED, IHS Markit (nee Macroeconomic Advisers) (released 11/1/2021), NBER and author.

Since March 2021, consumption growth has not been so fast (0.7%), when the chain growth rate was 4.5% (not calculated on an annual basis, but calculated on a logarithmic basis).

IHS MarkIt pointed out that consumption (along with trade and inventory data) collectively pushed up the tracking estimate for the fourth quarter from 4.9% to 6.8% (other data pushed up the tracking estimate to 7.4%). The newly released consumption data alone accounted for a 0.3% increase (both q/q SAAR).

{kind=link}

{kind=link}