Economists’ expectations and forecasts continue to differ from consumer-based expectations.

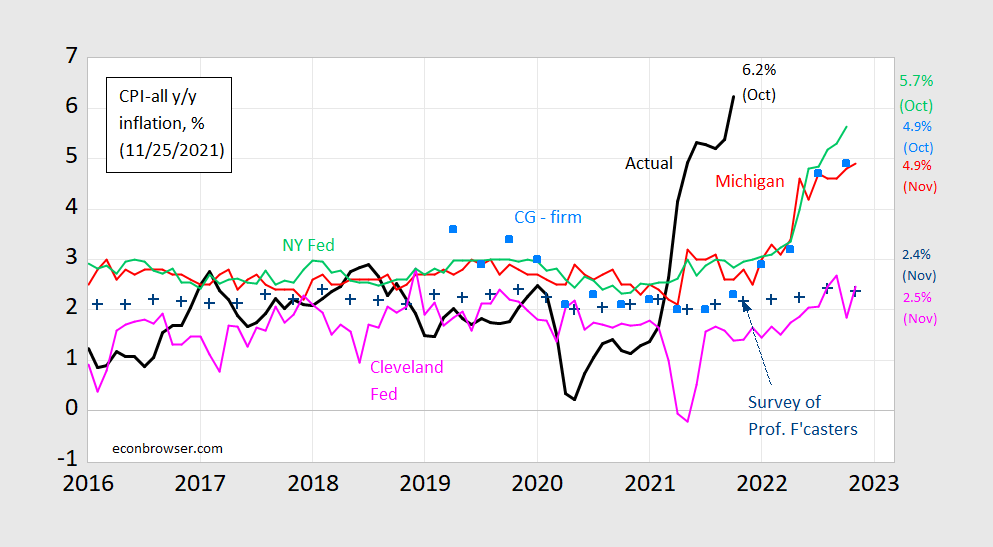

figure 1: CPI year-on-year inflation (black), the expected median of the survey of professional forecasters (blue +), the expected median of the Michigan Consumer Survey (preliminary) (red), the median of the New York Federal Reserve Consumer Expectation Survey (light green), Cleveland Federal Reserve’s forecast (pink), from the average of the Coibion-Gorodnichenko company expectation survey [light blue squares]Source: BLS, University of Michigan through FRED and Investment Net, Reuters, Survey of professional forecasters by the Federal Reserve Bank of Philadelphia, Federal Reserve Bank of New York, Cleveland Federal Reserve with Kobion and Gorodnichenko.

Which predictions are more unbiased (separate from which predictions are more representative of the agent’s expectations). During the period 1986-2021, the following results apply:

PITon = 0.022 + 0.128 It-12 + youTon

Adjust R2 = 0.00, SER = N = 428, the rejection unit slope is zero

PITon = 0.022 + 0.542 Clevelandt-12 + youTon

Adjust R2 = 0.166, SER = 0.012, N = 428, the rejection unit slope is zero

PITon = 0.004 + 0.788 SPFt-12 + youTon

Adjust R2 = 0.259 SER 0.011, N = 143, fail Reject unit slope null

All results use HAC robust standard errors.

In other words, the forecasts of professional economists are more accurate, even including the most recent period.

{kind=link}

{kind=link}