I teach unconventional monetary policy in the financial system course. Here are some interesting graphs (not brand new) related to the effectiveness of forward guidance.

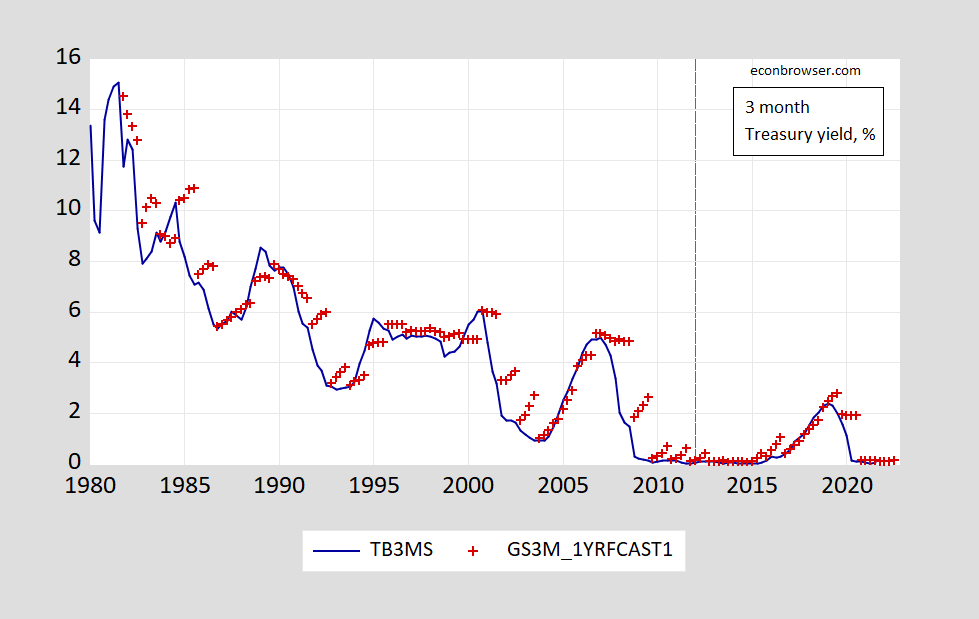

figure 1: The three-month Treasury bond yield (blue) and the average forecast of the survey of professional forecasters as of the third quarter survey (red +). The three-month yield comes from the secondary market. The blue dotted line implements forward guidance on the federal funds rate. Source: FRED, Philadelphia Federal Reserve SPF.

Since forecasts are related to short-term interest rates, forecasters are basically predicting the behavior of the Federal Reserve. Please note that after the announcement of clear forward guidance (January 25, 2012), expectations for future short-term interest rates fell.

In the most recent episode, the expected response is more clear.

figure 2: The three-month Treasury bond yield (blue) and the average forecast of the professional forecaster survey are as of the third quarter survey (red +) and as of the first quarter survey (blue-green +). The three-month yield comes from the secondary market. The blue dotted line implements forward guidance on the federal funds rate. Source: FRED, Philadelphia Federal Reserve SPF.

Please note that the forecast interest rate for the second quarter of 2020 (as of the first quarter of 2020) seems to be abnormally high; however, the survey for the first quarter was conducted in the last week of January/the first week of February-as early as Covid Before the news of -19 had a major impact on the United States (and also before the blockade in mid-March 2020).

As of the forecast for the third quarter (end of July/early August), interest rates are expected to be close to zero.

{kind=link}

{kind=link}