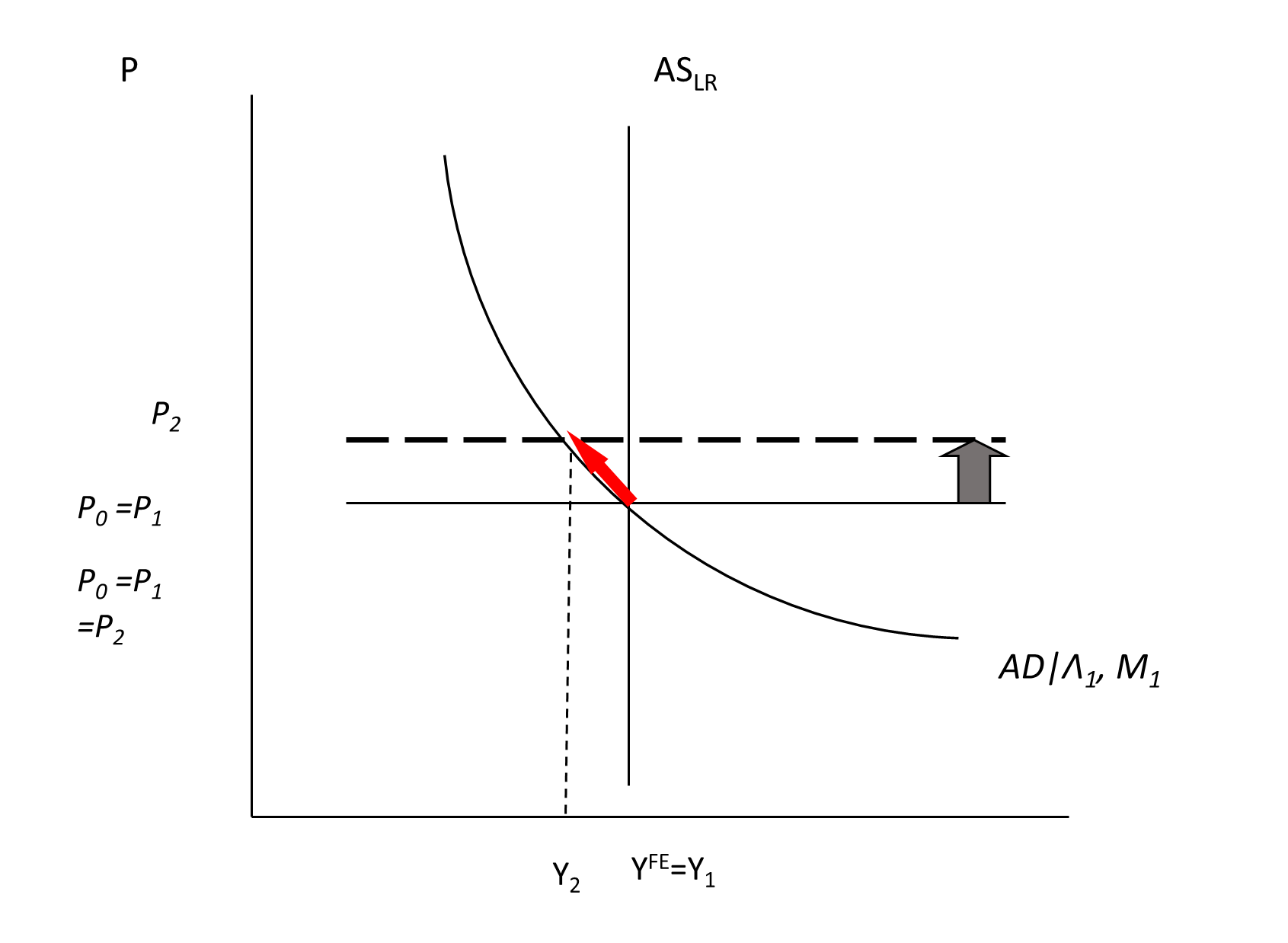

When assessing the course of inflation in the United States, there is a model that is helpful; I use the AD-AS model described here LocationTon. The cost of imported inputs can be interpreted as cost-driven shocks (rather than economic overheating caused by high aggregate demand relative to low potential GDP). In this context, China—as the main supplier of American inputs and commodities—is particularly important. Therefore, development there is imminent. The initial discovery that the Chinese vaccine is not particularly effective against omicron variants, coupled with the Chinese authorities’ zero tolerance for new coronavirus infections, means that the interruption of imports from China may continue for some time.

From Moze and Liu of the New York Times:

A new study studied blood samples from people who received two doses of the Covid-19 vaccine produced by the Chinese pharmaceutical company Sinovac. The study showed that the vaccine cannot prevent infection with the new, highly infectious variant of Omicron.

This study analyzed the blood of 25 people who had been vaccinated with Konoshine, which is the latest sign of the new challenges that Omicron faces as it spreads globally. Scientists at the University of Hong Kong found that in laboratory experiments, none of the 25 samples produced enough antibodies to prevent the variant from invading cells. The researchers said that it is not yet clear whether the third needle Kexing will improve the results.

These studies are preliminary, and the level of antibodies does not fully reflect a person’s immune response. It is not clear whether the Sinovac vaccine can protect against serious illness or death from Omicron, but it is likely to provide some protection.

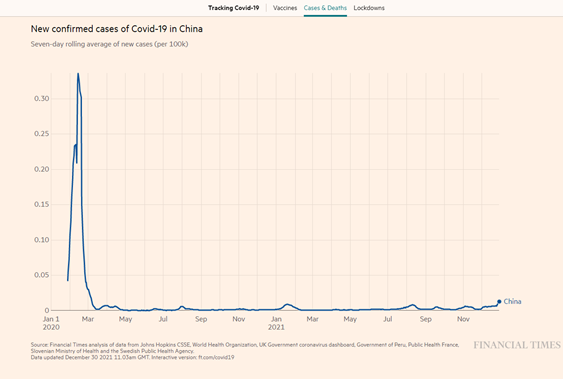

The zero tolerance policy clearly paid off in (at least reported) deaths and cases.

source: Financial Times, Visited on December 30, 2021.

China has achieved this result by using extensive lockdowns to deal with the fewest detected cases. These lockdowns may be appropriate—especially if Chinese vaccines are not very effective for omicron in reducing hospitalizations or deaths—but they will certainly reduce production. This means reduced exports to the United States and/or more expensive exports. This in turn will exacerbate the pressure of price increases.

figure 1: Cost drives the shock.

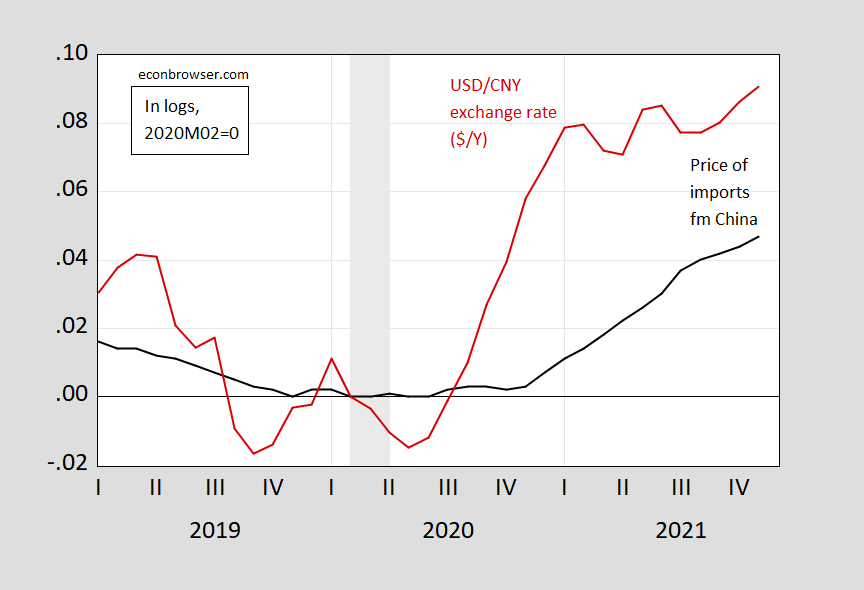

So far, since February 2020 (on a logarithmic basis, to November), the price of imports from China has risen by approximately 4.7%. Given that the U.S. dollar has depreciated against the renminbi by approximately 9.1% during the same period, the prices of Chinese goods exported to the United States may fall.

figure 2: The prices of imported goods from China, in U.S. dollars (black), and the exchange rate of U.S. dollars/renminbi, in U.S. dollars/yuan, are all in the 2020M02=0 log. NBER-defined recession dates are shaded in gray from peak to trough. Source: FRED, NBER and author’s calculations by BLS and Federal Reserve Board.

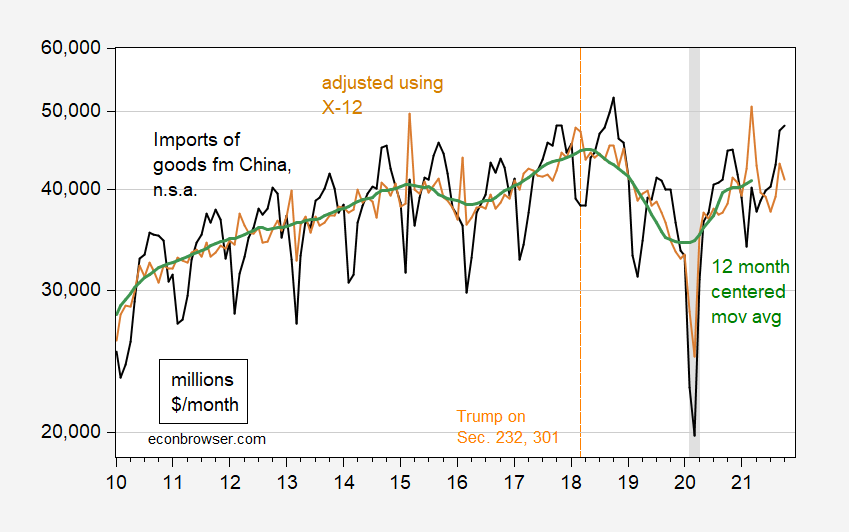

The price index does not reflect the disruption caused by unimported goods. We can only get some impression from China’s total imports.

image 3: For goods imported from China, without seasonal adjustment (black), the full sample (brown) and the 12-month central moving average (green) are adjusted using the multiplication Census X-12, both in millions of USD/month. , On a logarithmic scale. NBER-defined recession dates are shaded in gray from peak to trough. Source: BEA/Census via FRED, NBER and author’s calculations.

How big is the impact of China’s interruption on the United States? sound Don’t risk guessing.Various higher frequency (ie monthly) indicators were only available before November (see Yardney’s compilation), so the most recent group closure will not be reflected. But at least, when considering the inflation process in 2022, the international dimension needs to be kept in mind.

{kind=link}

{kind=link}