recent New York Times article Note that Russia has taken steps to shield itself from economic sanctions, including building foreign exchange reserves. Real reserves are high, and relatively speaking, once nominal GDP is thought to be less than 2014.

figure 1: Russian international reserves (millions of dollars).

About the reserve (now):

“This is what gives Putin strategic freedom of action,” writes Columbia University economic historian Adam Tooze.

Under normal circumstances, with limited external debt (about 2/3 of reserves), the country appears to be fairly safe from a traditional run. On the other hand, currencies are already depreciating even when nominal policy rates are fairly high.

figure 2: RUB/USD, up is the appreciation of the ruble.

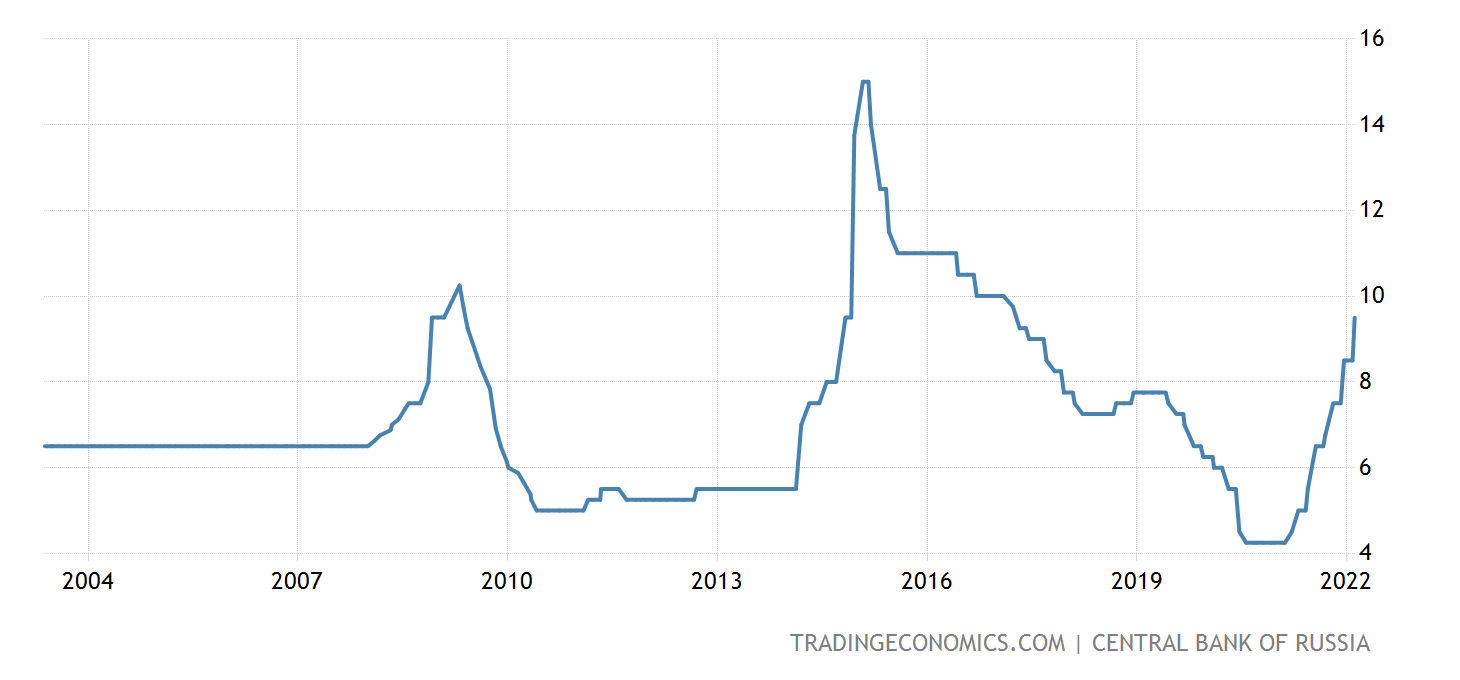

image 3: Central Bank of Russia policy rate, %.

Russia’s external accounts came under pressure back in 2014 when Russia was sanctioned for a proxy war over the illegal annexation of the Crimea and Donbas regions, as discussed here. Sanctions could be tougher if conventional force strikes elsewhere in Ukraine. Whether the larger reserves are enough to allow the Russian economy to withstand retaliation depends on many factors. In a narrow sense, the fact that Russia has trade and current account surpluses helps.Declining ruble holdings by non-residents may make them less vulnerable to flight [1] (Though one can well imagine well-connected residents trying to achieve capital flight). Russia’s financial openness stood at 0.48 as of 2019, down from 0.72 in 2014, according to the Chinn-Ito Index, so authorities may be better positioned to stem this flight.

Despite this, the System for International Transfers (SWIFT) remains suspended, Or, as it now seems more likely, sanctions on state-owned banksEssentially different from stopping suddenly for fear of loss.

Anyway, look for some interesting moments in Russia’s external accounts and currencies.

{kind=link}

{kind=link}