Most discussions of the macro impact of Russia’s expanded invasion of Ukraine assume higher oil prices (eg, [1]). This makes sense, certainly in the short term. However, if oil prices rise enough (remember, Brent has risen from around $70/bbl to $90/bbl), they will cause an economic slowdown. Economic slowdowns tend to drive down oil prices. I think it’s the chart; that’s how I see it in the short and (probably) medium term.

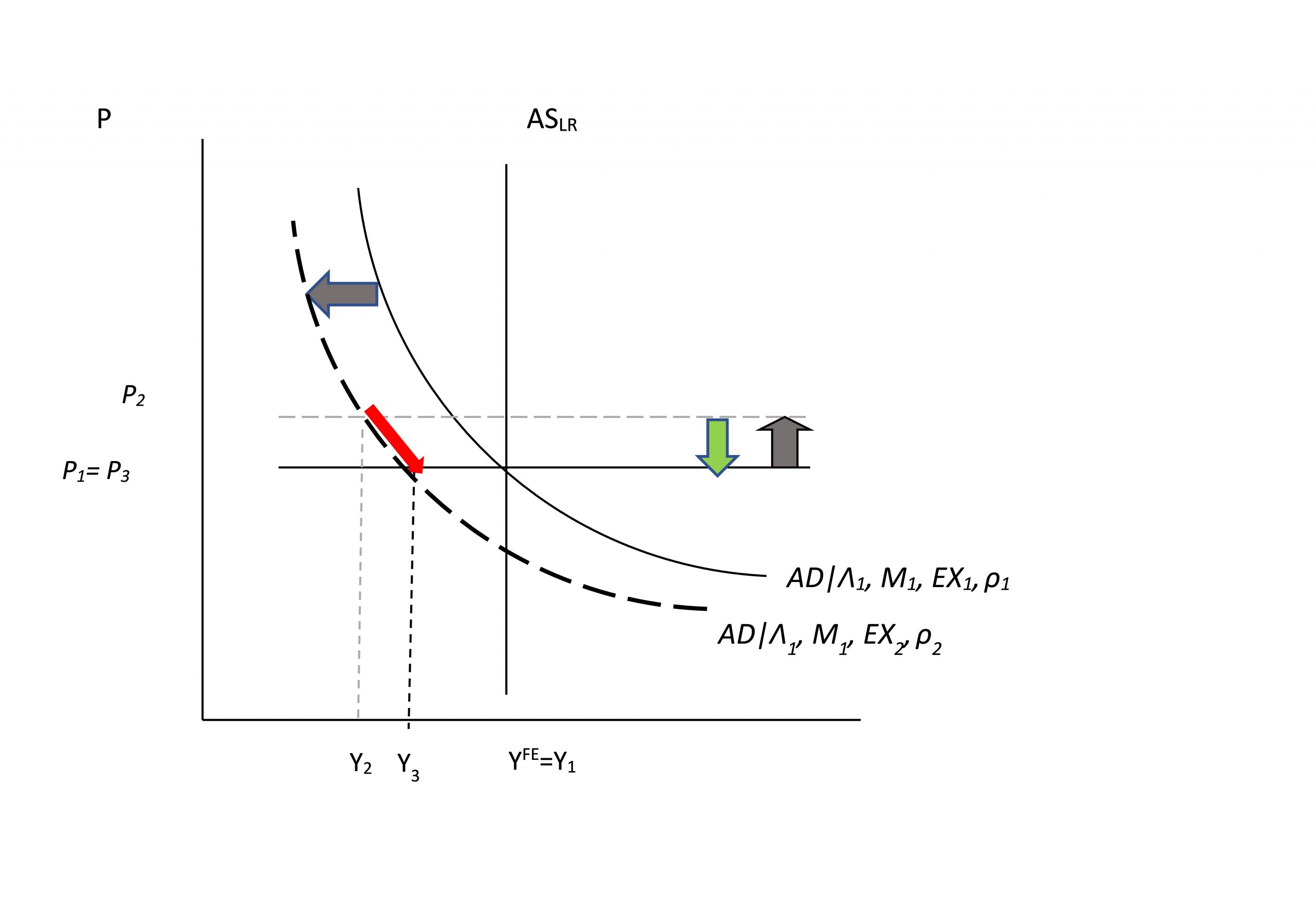

In the short term, in the AD-AS framework, conflict increases uncertainty and risk, thereby depressing aggregate domestic demand at home and abroad. The AD curve shifts inward (exports fall, model assumes financial friction, so investment falls, dark grey arrows). Oil prices surged (light grey arrows), leading to cost-push inflation. predecessor is an export, ρ is risk.

figure 1: Oil prices rose, output fell in the rest of the world, and risks rose.

output drops to Y2 The price rises to P2 – Stagflation at least in period 2. The red arrows indicate the path of price levels and output.

However, this could boost world demand for oil as production falls. With oil’s low price elasticity, it doesn’t take much to push prices back to where they started.

figure 2: Falling oil prices and output in the rest of the world remain subdued, raising risks.

output returns to Y3The price level falls to P3 (in the absence of stimulative fiscal and monetary policies).

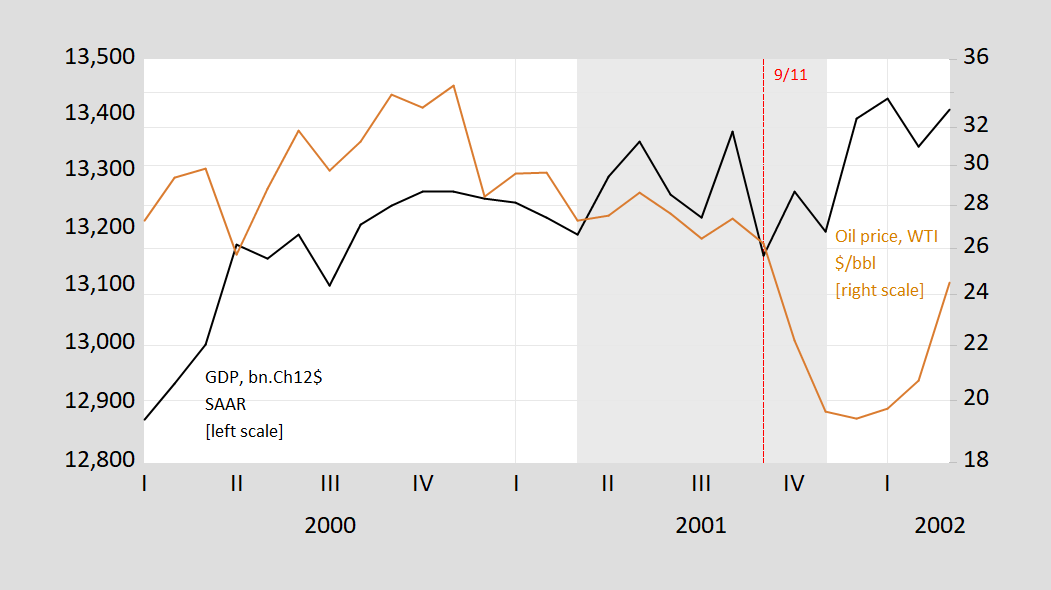

Will oil prices fall as economic activity declines, and if so, by how much? One can take a cue from the unusually mild recession of 2001; by the time the recession ended (the trough), oil prices had fallen 28% from the beginning (the peak) of the recession.

image 3: GDP, bn.Ch.2012 $ SAAR (black, left log scale) and oil prices, WTI, $/bbl (brown, right log scale). Recession dates as defined by NBER are shaded from peak to trough in gray. Source: IHS-Markit, EIA via FRED, NBER.

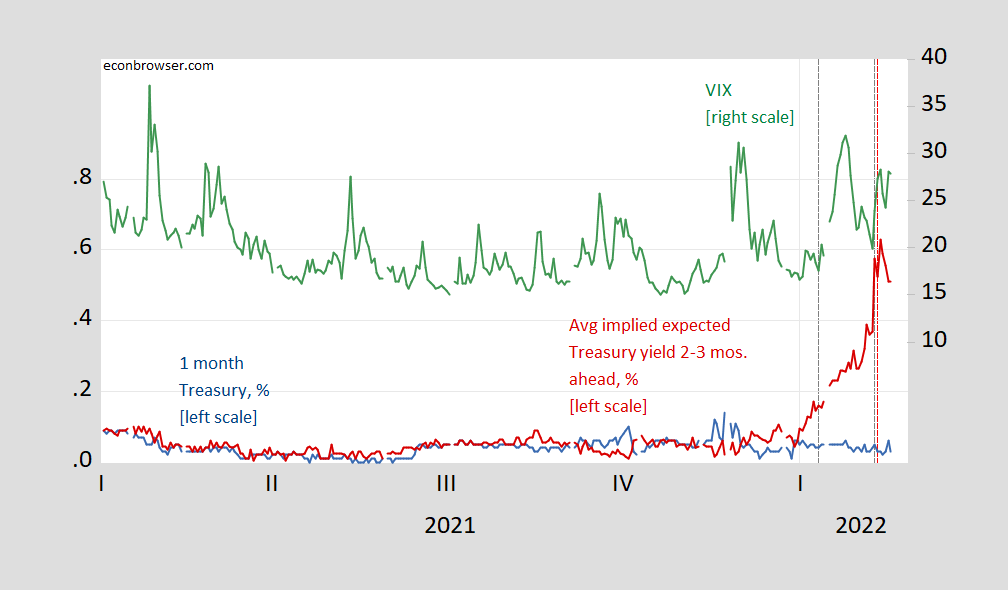

The more likely it is that oil prices will rise sharply, the more likely the central bank will react. While interest rates are expected to be rising (inferred from the yield curve and elsewhere), it is difficult to distinguish the motives – rising inflation due to ongoing cost-push pressures, or potentially higher oil prices due to Russia’s threat to Ukraine.

image 3: 1-Month Treasury Yield, % (blue, left scale), Implied Average Treasury Yield over 2-3 months, % (red, left scale), VIX (green, right scale). Red dotted line for seconds. Blinken’s press conference on 2/11, grey dotted line for CPI releases on 1/12 and 2/12. Source: Treasury via FRED, CBOE via FRED, and author’s calculations.

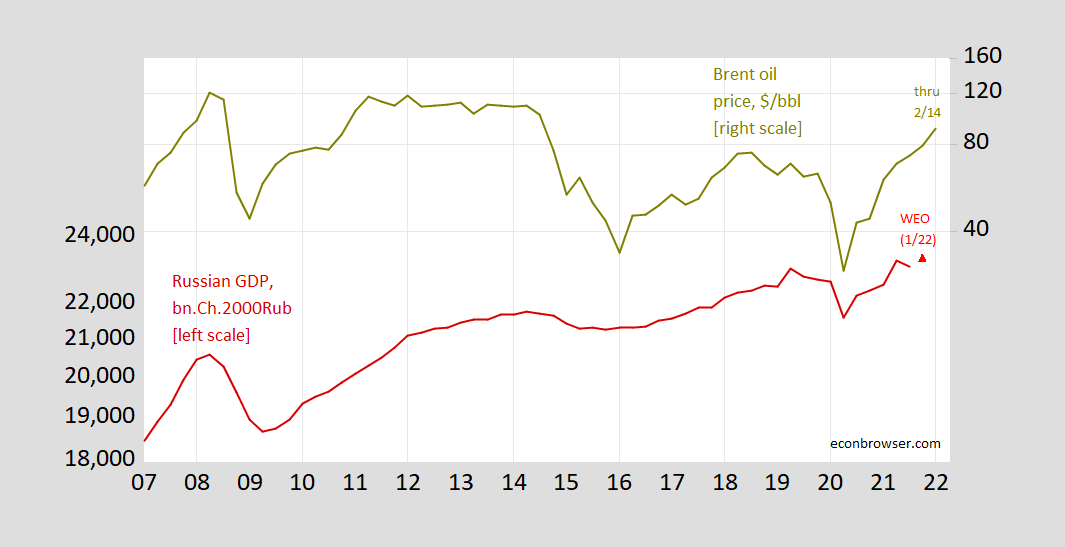

Falling oil prices and the impact on Russia’s GDP are issues that Russian policymakers should consider.

Figure 4: Russian GDP in RUB bn, seasonally adjusted (red, left log scale), IMF forecast level for the fourth quarter of 2021 (red triangle, left log scale), and oil prices (cloth rent), USD/barrel (yellow-green, right logarithmic scale). 2022Q1 is the first half of the quarter. Sources: OECD via FRED, IMF January WEO Update, EIA via FRED, author’s calculations.

{kind=link}

{kind=link}