One way to assess external financial stress is to look at foreign exchange market stress (EMP) – changes in exchange rates, changes in reserves and changes in interest rates, possibly weighted by the inverse of the standard deviation. or others (see e.g., several different versions of Patnaik et al. (2017)).

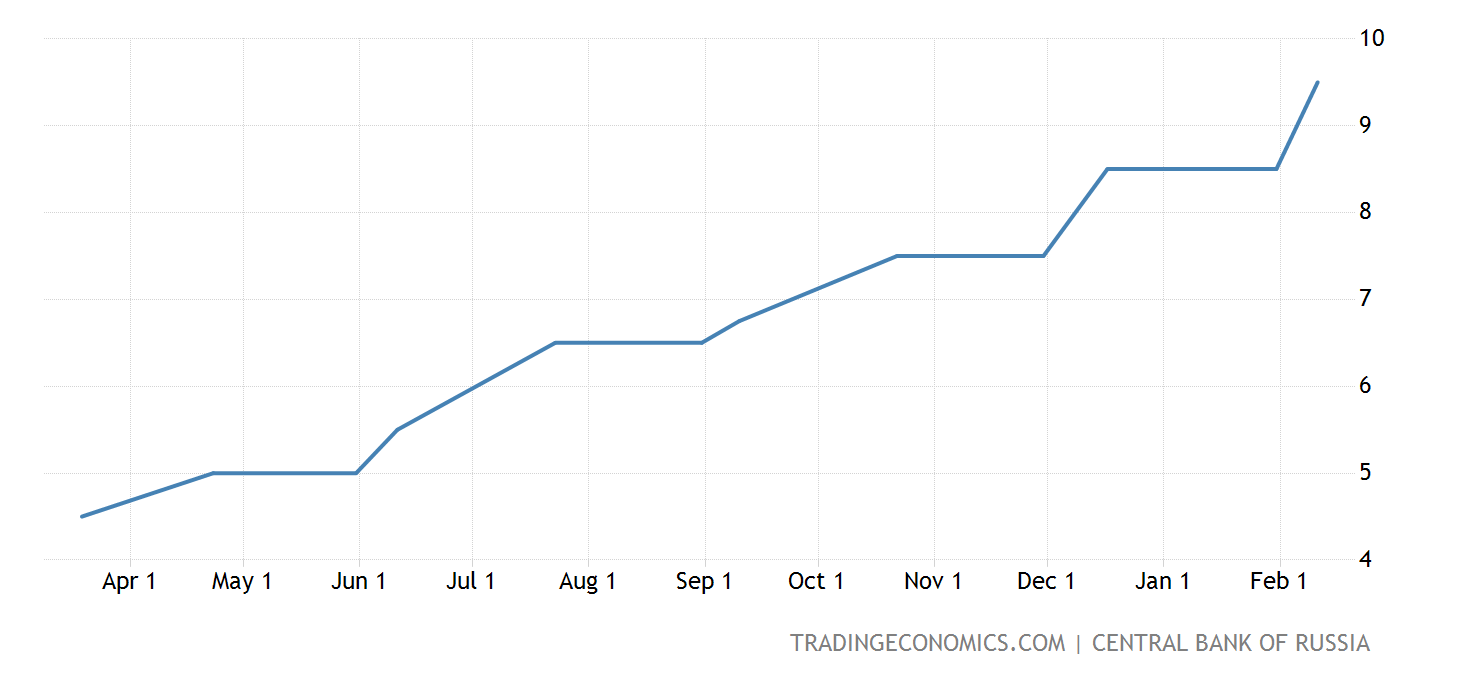

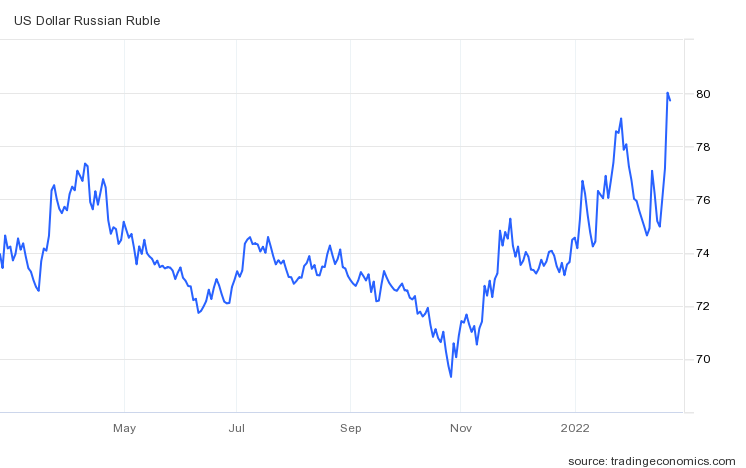

Without calculating the index (I don’t have access to some relevant variables), this is what we’ve seen today over the past year.

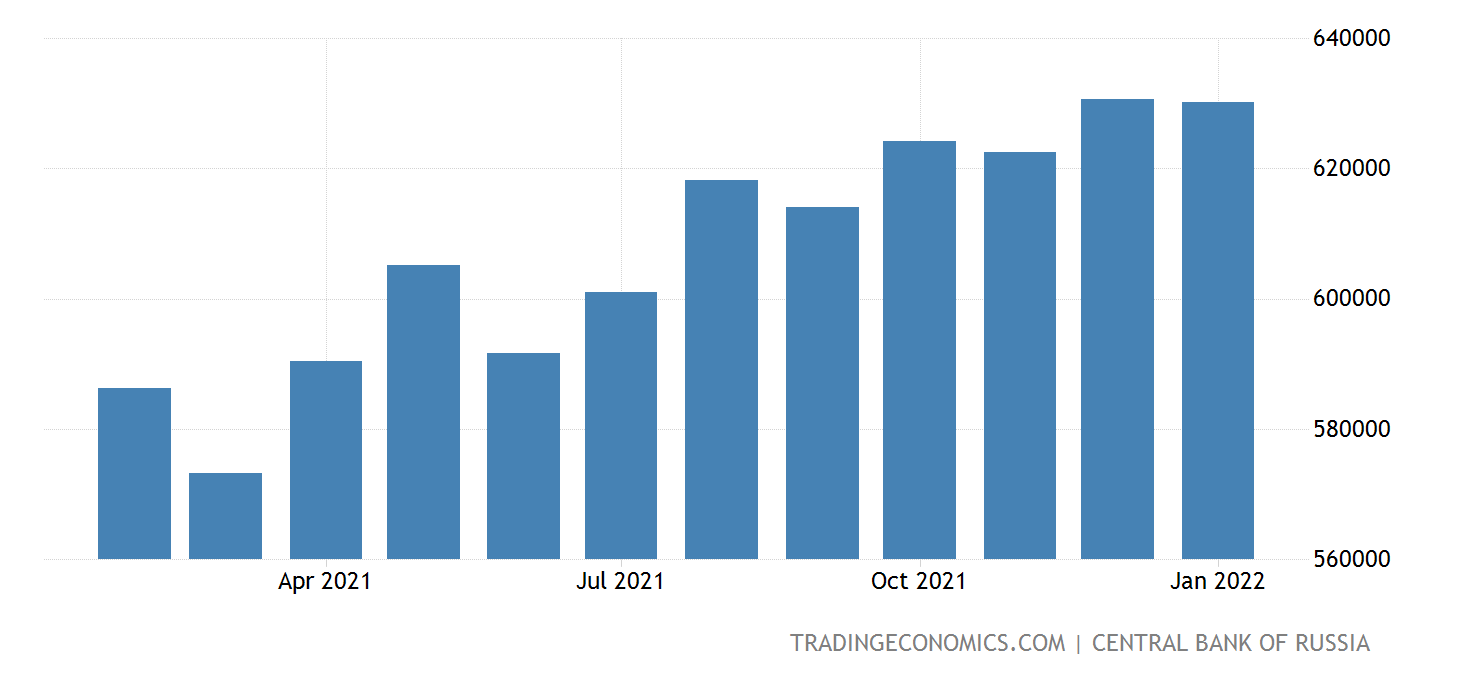

On a monthly basis, reserves declined slightly in January.

Obviously, we (or I) don’t see reserves every day, so we don’t know what’s going on on the intervention side.

More broadly, confidence in stock market summaries is plummeting.

The figures predate the announcement of sanctions today. Looking ahead, the ruble is expected to depreciate, reserves dry up and interest rates rise. How much depends on how strict the economic sanctions are and how successfully Russia has isolated economic and financial sanctions. Higher oil prices ($120/bbl is a number I hear a lot) will reduce pressure by increasing foreign exchange earnings, so it’s unclear what the net effect will be.

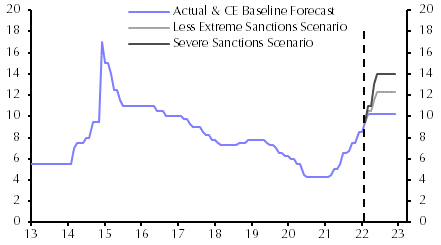

Capital Economics pointed out:

- There are so many permutations that putting a number on the impact is almost impossible. For what it’s worth, we estimate that sanctions imposed in 2014 reduced Russia’s GDP growth by about 1%. This appears to be the correct range for the sanctions described above (although the risk may be skewed towards impacts greater than 1%). There will be greater impact in areas that are particularly dependent on Western goods and services (eg software, some capital goods).

- As for the impact on financial markets, Russian financial markets now appear to be pricing in more seriousness than the 2014 annexation of Crimea (and subsequent sanctions). But even so, there may be room for further declines if sanctions are imposed, as there is uncertainty about the need for further tightening of sanctions to influence Russian policy. We suspect that the ruble could fall another 10% in this scenario, further pushing up inflation and prompting the central bank to hike rates by at least 200bps to 12.0%. (See Exhibit 2.)

I have reproduced their Figure 2 below.

resource: W. Jackson, “Russia and the Possible Impact of Sanctions,” Capital Economics, 2/22/22.

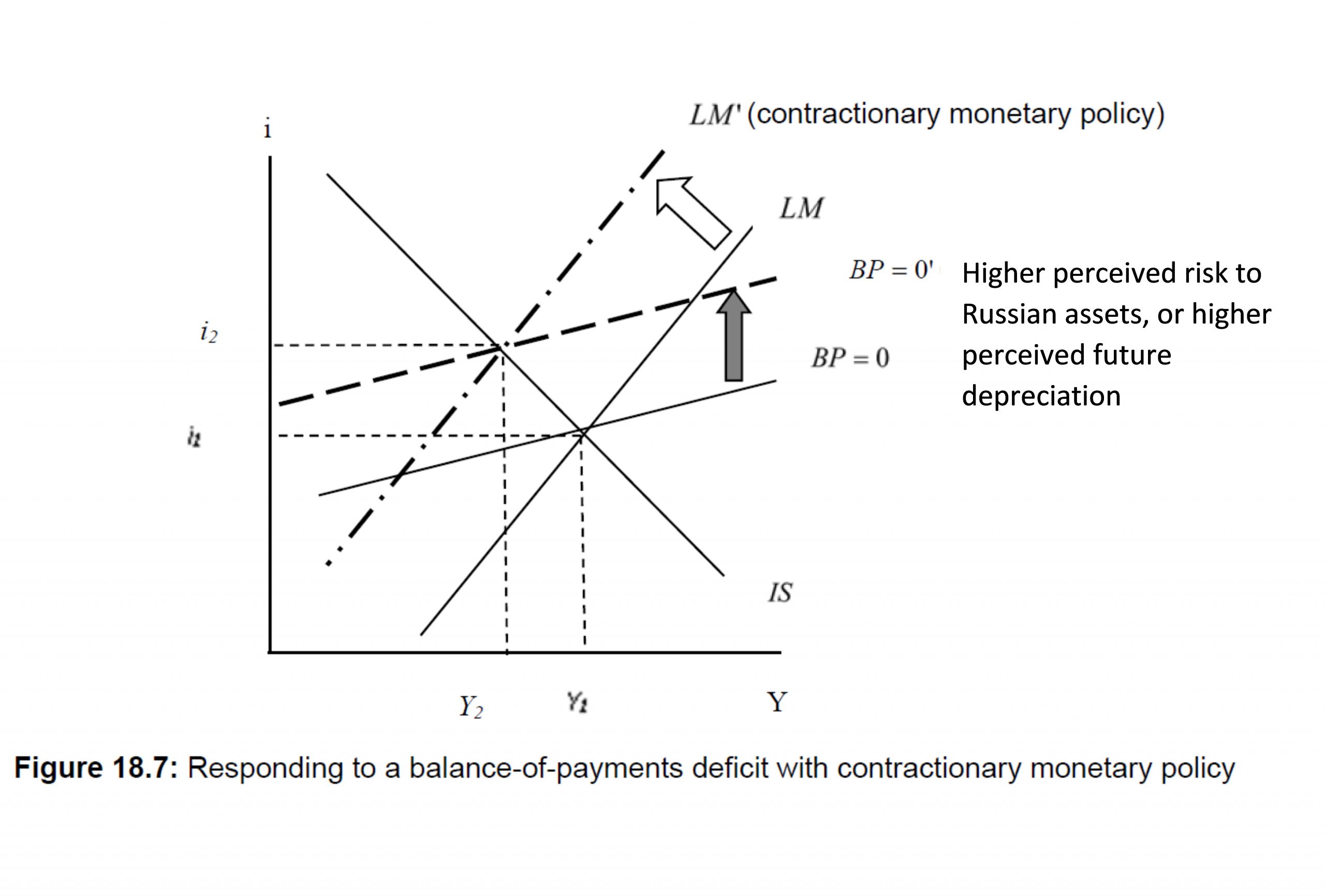

In other words, if the Russians don’t want to burn their reserves to prevent the ruble from free-falling, then interest rate defense is the way to go (so this motive is added to the fact that they may have to suppress inflationary pressures).

Graphically, in Mundell-Fleming:

Higher interest rates would indeed prevent a balance of payments crisis caused by heightened risk aversion, transaction costs or expectations of currency devaluation – but at the cost of a recession (I ignore the complexities of second-generation multiple equilibrium equilibria) la Obstfeld, The Payment Crisis of Jeanne et al). Oh, and raising U.S. interest rates in response to inflationary pressures would also exacerbate Russia’s balance of payments challenges.

{kind=link}

{kind=link}