funny quotes from 2020 IMF Article IVAnnex III: External Sector Evaluation (distributed February 2021):

evaluate. International reserves in 2020 are estimated at 365 percent of the IMF’s reserve adequacy indicator. While well above the 100-150% adequate range, the level of reserves is still appropriate given Russia’s vulnerability to oil price shocks and sanctions.

After selectively excluding Russian banks from the SWIFT system and sanctioning the Russian central bank, Russia appears to be well-positioned to deal with the situation – rather rare, as it is essentially “stop suddenly” (see textbook discussion here) encounter severe financial sanctions – will be tested (economist). Two observations:

- The $639 billion figure for international reserves referred to as foreign exchange in colloquial discussions is a bit misleading, giving the impression that they are highly liquid. In fact, of this figure, $463 billion is in foreign exchange; $132 billion is in gold, and $24 billion is in special drawing rights (as of January 2022, As MinFin reports to the IMF).

- $463 billion is big or small. Given that Russia has a current account and a trade surplus (to the third quarter), the latter of which is likely to increase as oil prices rise (if oil can be sold and paid for), then it depends on how quickly financial capital can leave the country. countries. This also depends on the central bank’s interest rate policy).That is, it is measured Exchange Market Pressure (EMP) It will depend on how open Russia is to finance.

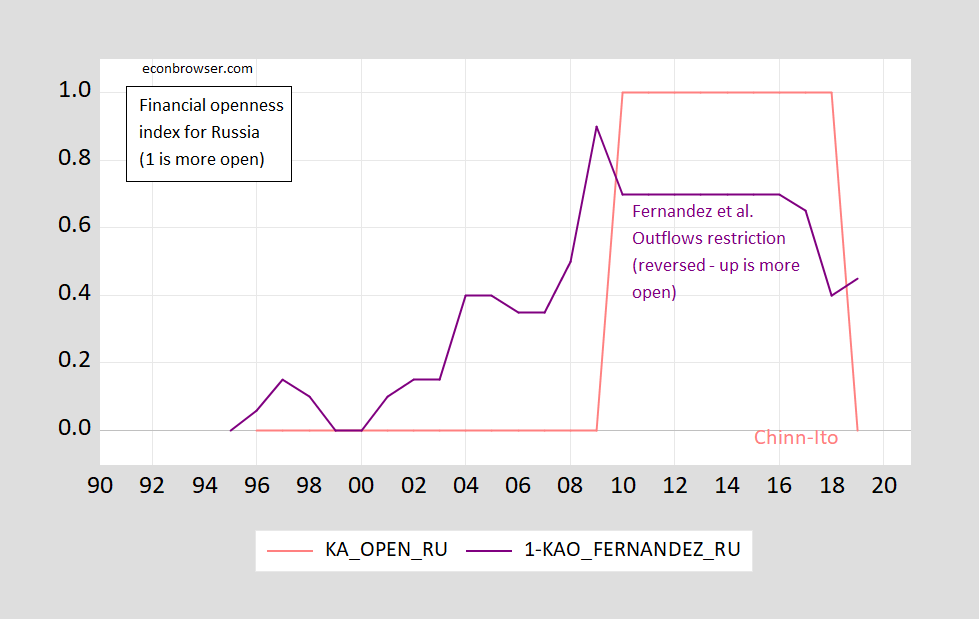

legally The measures (from Chinn-Ito) only last until 2019:

figure 1: The Chinn-Ito Financial Openness Index for Russia (salmon), Turkey (green), South Africa (light blue), China (dark red) is normalized on a scale of 0 to 1 (most open). resource: Ito and Chin (2021).

As of 2019, according to information reported to the International Monetary Fund, current regulations make Russia one of the most financially closed economies.

More relevant are restrictions on outflows.There are better metrics, including Pasricha et al. and Fernandez et al. Only the latter has been updated to 2019, so here is a comparison:

figure 2: The Chinn-Ito Financial Openness Index for Russia (salmon), normalized to 0 to 1 (most open), inverts Fernandez’s capital account restrictions on outflows (purple). Up is more open to both. resource: Ito and Chin (2021)and Fernandez, Klein, Rebucci, Schindler, and MUribe (2016 update).

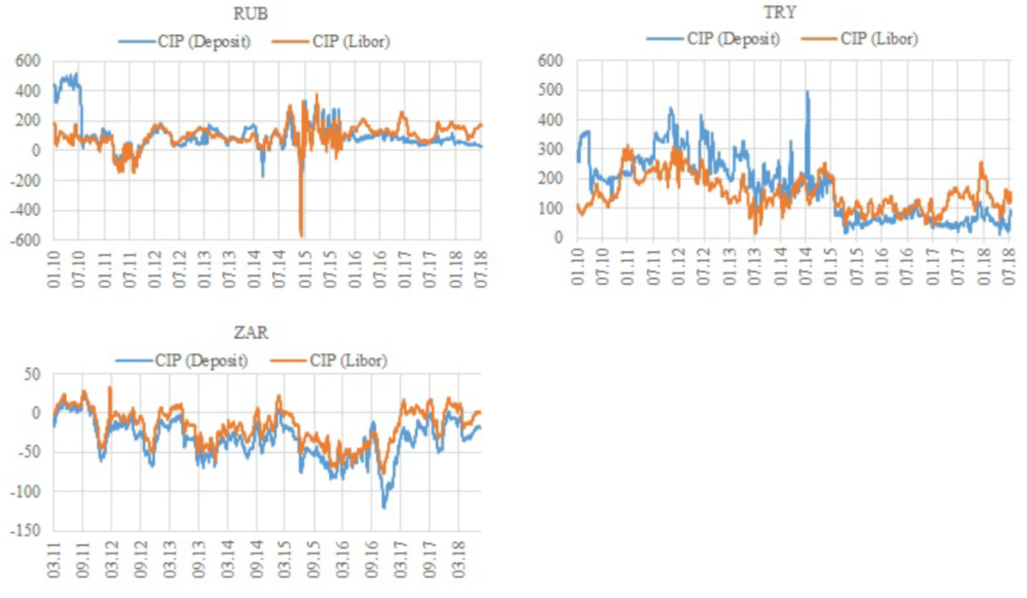

If the regulations are the same as in 2019 (which I doubt), then at least on paper significant controls are in place. Whether these regulations are effective in restricting flows in practice is another question; we need de facto capital controls. usually, Use Covered Spreads.

image 3: Covers spreads in Russia, Turkey and South Africa. resource: Geyikçi and Özyıldırım (2021).

.

Russia’s 2014-18 difference was roughly comparable to Turkey’s over the same period. However, differences in default risk and liquidity complicate interpretation. So the question of how much money outflows can be stopped is still an open question for me.

However, my guess is that given the severity of the sanctions, FX market stress (by any measure) will soar.

{kind=link}

{kind=link}