Interestingly, if the implied forward is to be believed, the Fed won’t raise rates too quickly.

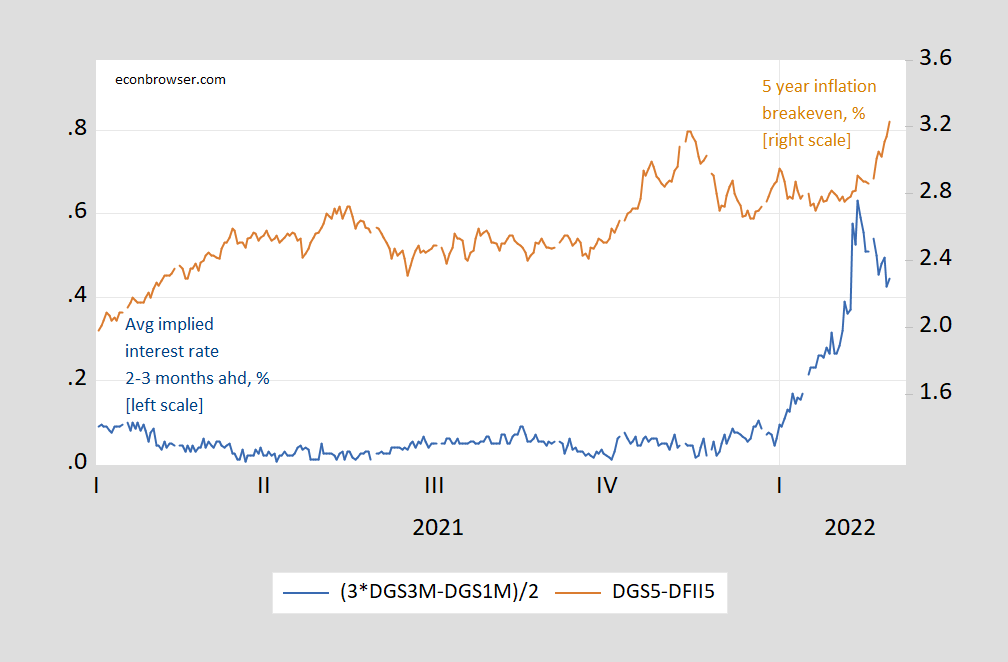

First, as the 5-year inflation breakeven rises, forward.

figure 1: Implied Treasury yields for the next 2-3 months, as a percentage (blue, left scale) and 5-year inflation breakeven, calculated as the simple difference between Treasury and TIPS yields (brown, right scale). Source: Treasury via FRED, and author’s calculations.

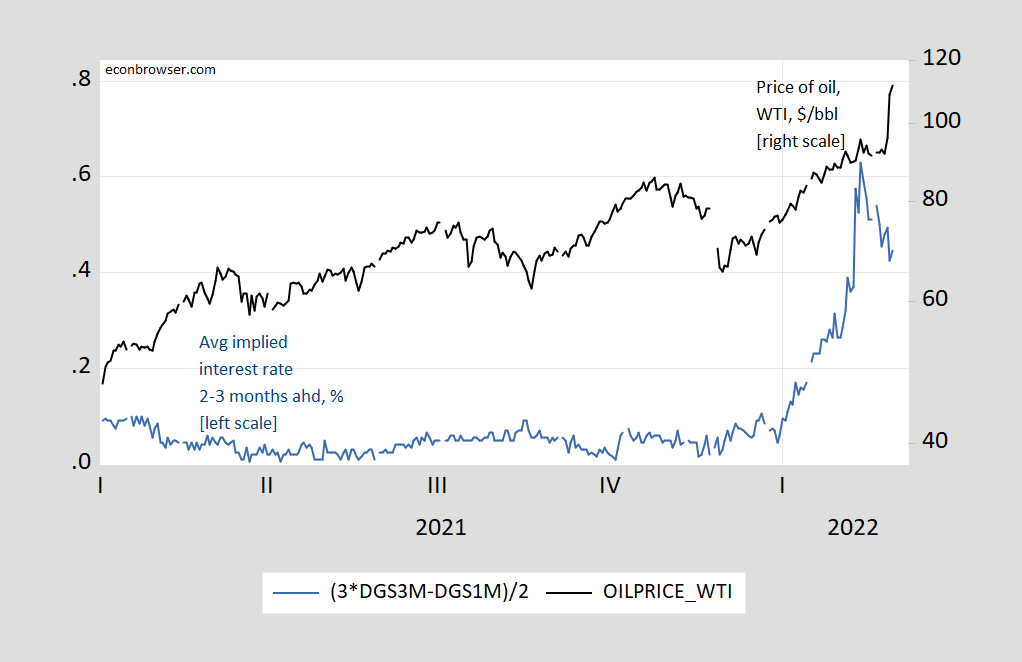

Second, forward as the price of oil (WTI) rises.

figure 2: Implied Treasury yields for the next 2-3 months, % (blue, left scale) and oil prices, WTI, USD/bbl (black, right log scale). The 3/1 and 3/2 observations are front month futures. Sources: Treasury, EIA through FRED, NYMEX, and author’s calculations.

Of course, forward calculations are drawn from any term premium, while inflation breakeven calculations are drawn from both term and liquidity premiums (see here postal).

{kind=link}

{kind=link}