An article on signaling the yield curve appears in Reuters, NBC Finance Channel, Fox Business, Bloomberg, CNN . Here is a related image:

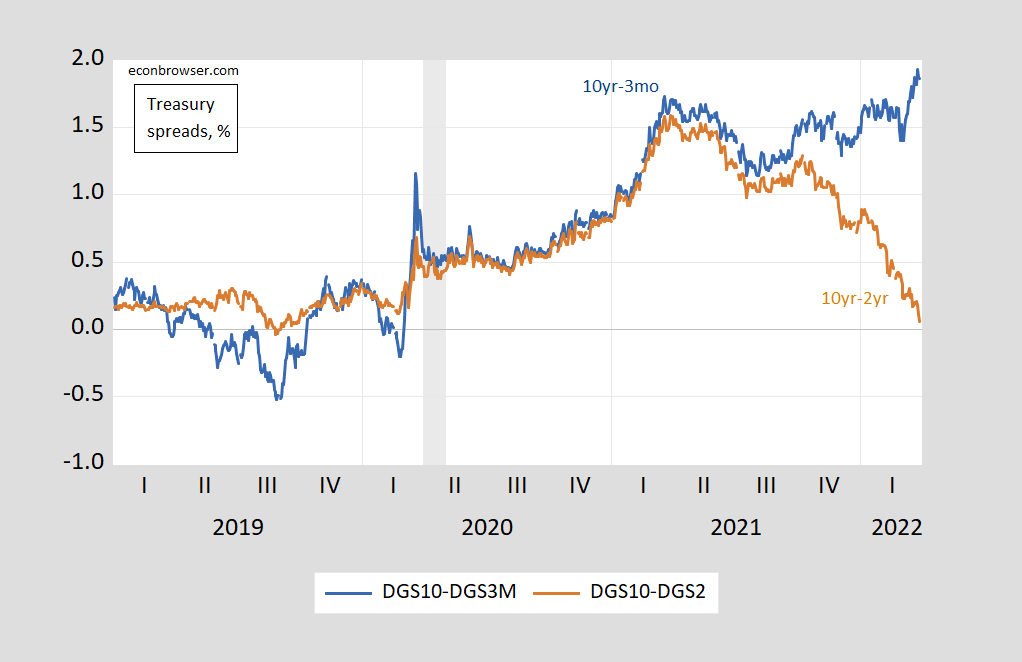

figure 1: 10-year-3-month Treasury spread (blue), 10-year-2-year spread (brown), both expressed as a percentage. Recession dates as defined by NBER are shaded in gray. Source: FRED, NBER and author’s calculations.

The 10-year to 2-year spread is close to zero, so this part of the yield curve will be close to inversion, which is sometimes a precursor to a recession.

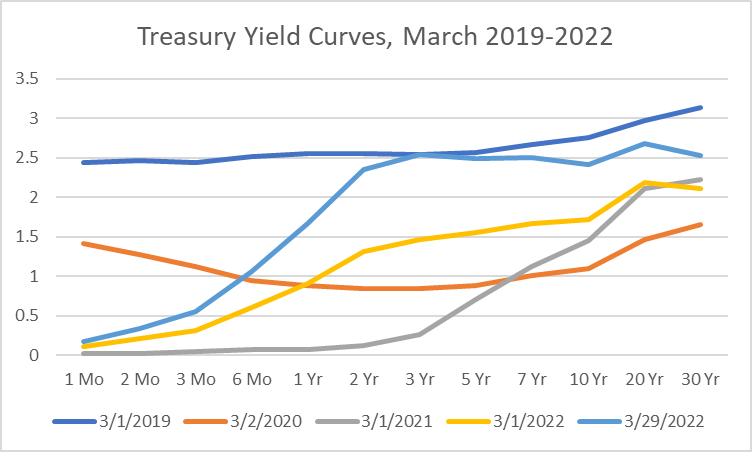

Examination of the yield curve today and at several points in time shows that today’s inversion does not apply to much of the curve.

figure 2: Yields on Treasury bills of different maturities, in %. Source: Ministry of Finance.

Note that as of today, the reversal has only occurred in the 10- to 3-year segment (as of yesterday’s 10- to 7-year segment).

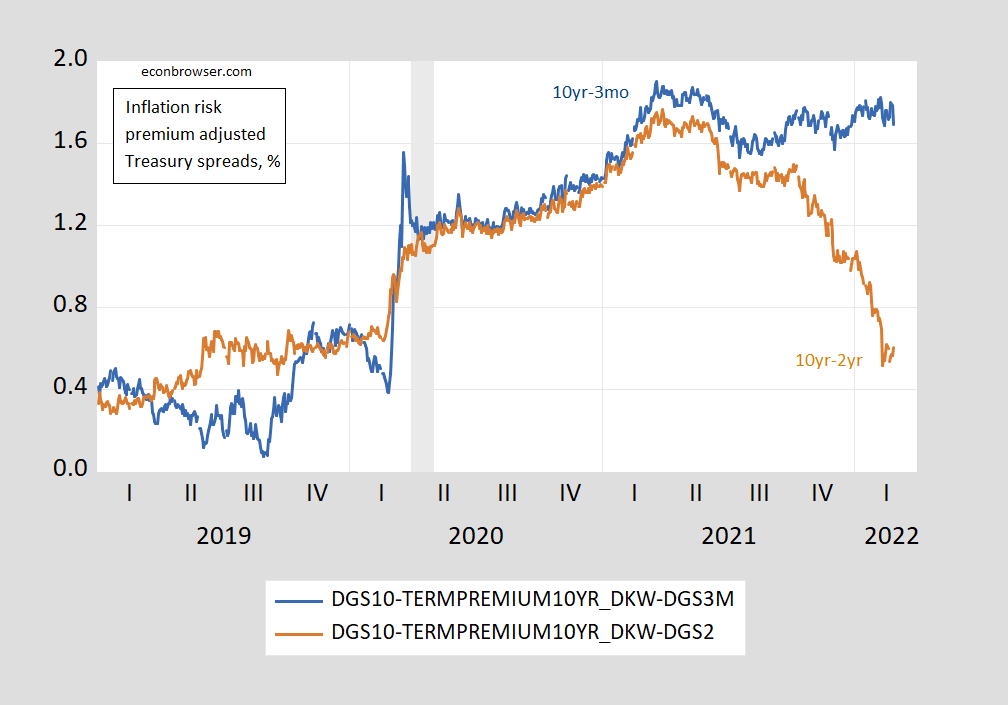

The justification for an inversion as a recession precursor is that lower expected future short-term rates during a recession drive lower long-term maturities. In principle, by removing term premiums for long-term maturities (possibly driven by inflation risk), a clearer picture of expected future short-term rates relative to current short-term rates can be obtained. In Figure 3, I show the spread adjusted by the inflation risk premium estimated by DKW.

image 3: 10-year-3-month Treasury spread minus estimated inflation risk premium (blue), 10-year-2-year spread minus estimated inflation risk premium (brown), all expressed as a percentage. Recession dates as defined by NBER are shaded in gray. Source: Treasury via FRED, NBER, KWW Follow DKW and author’s calculations.

This variable measures, in principle, the expected short-term interest rate over the next 10 years relative to the current 3-month yield when the 10-year-3-month spread is removed from the 10-year term premium. This is what the unadjusted and adjusted 10-year to 3-month spreads look like for the past 3 years.

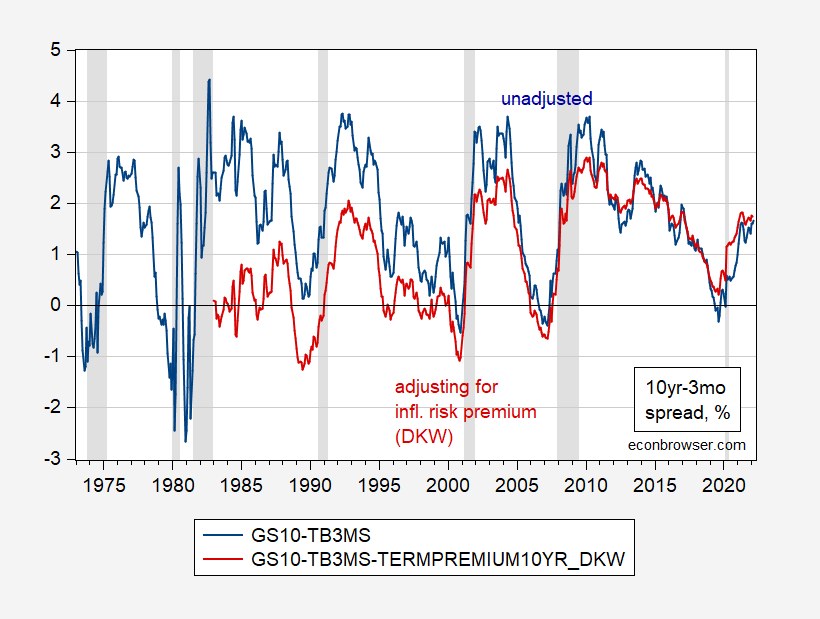

Figure 4: 10-year to 3-month Treasury spread (blue), 10-year to 3-month spread minus 10-year inflation risk premium (red). March observed March 29. Recession dates as defined by NBER are shaded from peak to trough in gray. Source: Source: Treasury through FRED, NBER, KWW Follow DKW and author’s calculations.

notes deep Reversals in adjusted series usually precede recessions.

We do not have a 2-year inflation risk premium estimate to be able to adjust for the 10-year to 2-year spread (the above calculations assume a 3-month Treasury risk premium of zero). What is true, however, is that the 10- to 2-year spread, which is removed from the 10-year inflation risk premium, has not reversed (0.6pp adjusted, 0.39pp unadjusted) as of end-February.

For more information on term spreads, credit spreads and recessions see here postal.

{kind=link}

{kind=link}