in a VoxEU Posts Written today by Laurent Ferrara, Matteo Mogliani and Jean-Guillaume Sahuc, using the Growth at Risk (GaR) approach (Ferrara et al. 2022, Ungated 2020 WP Edition) They estimate downside risks to the euro area’s sequential growth relative to US GDP.

Using the Composite Indicator of Systemic Stress (CISS) developed by the ECB (Holló et al., 2012), they found:

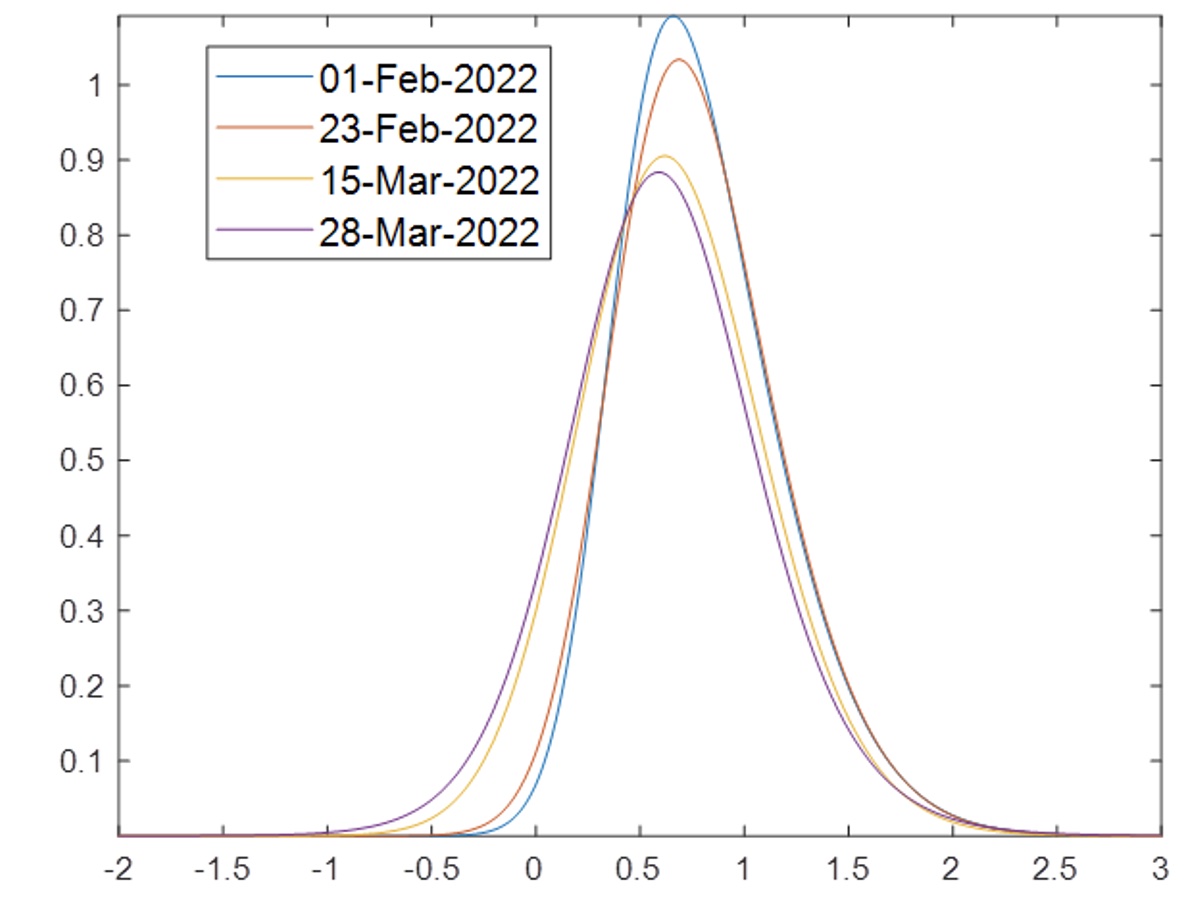

We observe that, within a few days, the probability density function for conditional GDP growth in the euro area in Q1 2022 shifts significantly to the left. The March 28 estimate shows a thicker left tail, underscoring an increase in macro downside risks following the start of the Ukraine war. As for the 10% GaR value, which can be considered as the 10% quantile of the estimated conditional distribution, it changed from -0.02% on February 1 to -0.90% on March 28.

as shown in picture 2 Ferrara et al.

resource: Figure 2 from Ferrara et al (VoxEU, 2022).

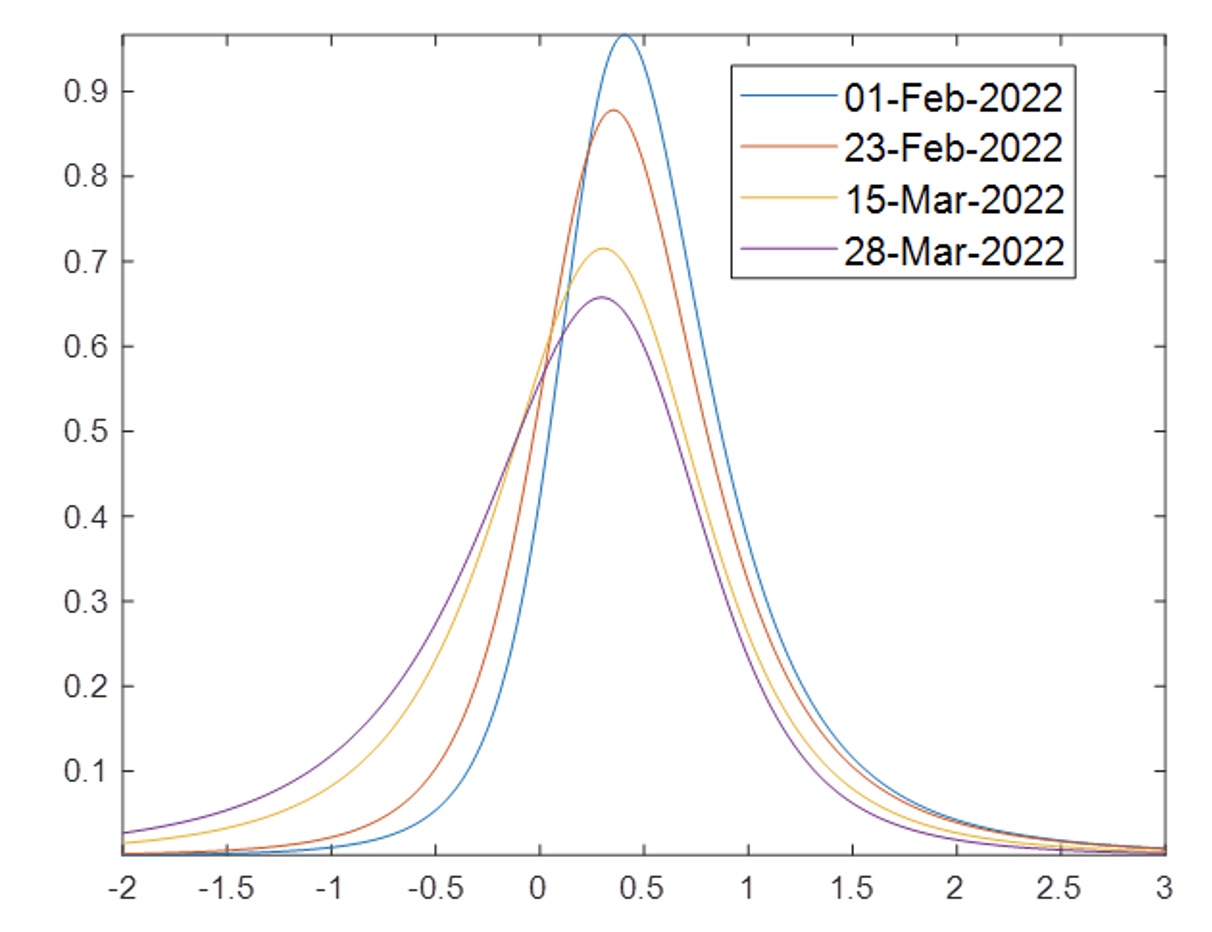

For the US, the shift was less pronounced than for the Eurozone: GaR (10%) fell to 0.03% from 0.30% on 1 February – so GaR (10%) fell by only about 0.30 percentage points.

resource: Figure 3 from Ferrara et al (VoxEU 2022).

{kind=link}

{kind=link}