The same is true for two-year Treasury bonds?

The standard breakdown of the ten-year rate is (for quarterly data):

The first item on the right hand side (call it and’) will represent the expected assumption of the term structure – the long-term interest rate is the average of the expected future short-term interest rates.

We did not observe the expected value, but we did observe the realization after the fact.Calculate the average realized after the fact to obtain and.

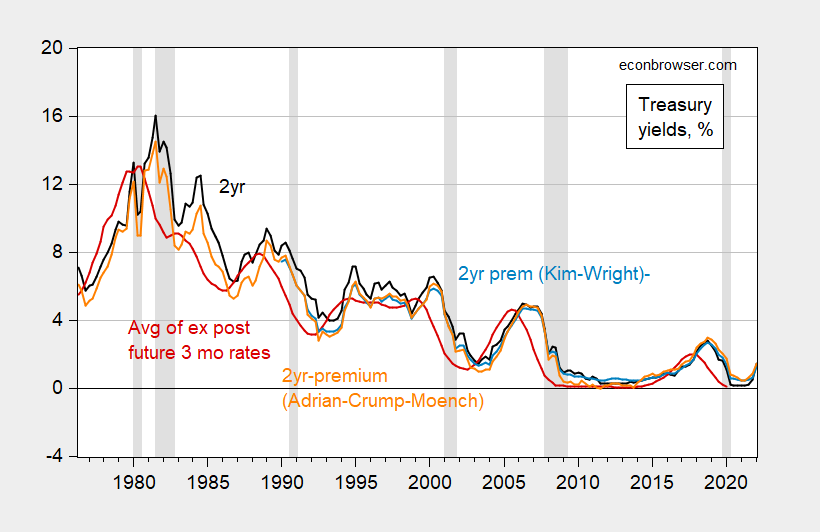

Figure 1 draws A generation10 years, t (black line), and (red line), and

![]()

where is estimated rp is the Kim-Wright estimate (blue line) or the Adrian-Crump-Moench estimate (orange).

figure 1: 10-year fixed-term Treasury yields (black), 10-year minus Kim-Wright term premium (blue), 10-year minus Adrian-Crump-Moench term premium (orange) and secondary market three months ahead Average of Treasury yields (red). Recession dates as defined by NBER are shaded from peak to trough in gray. Source: Treasury via FRED, Schillerpass Fred, New York FedNBER and author’s calculations.

If full-information rational expectations hold, and the estimate of the zero-coupon bond’s 10-year term premium is accurate, then the light blue or orange line should more or less match the red line. Although the Adrian-Crump-Moench estimate is better than the Kim-Wright estimate, this characterization does not hold.

A similar point applies to the biennium.

figure 2: 10-year fixed-term Treasury yields (black), 10-year minus term premium (blue), 10-year minus Adrian-Crump-Moench term premium (orange), and the next three-month Treasury bond yield in the secondary market Average of rates (red). Recession dates as defined by NBER are shaded from peak to trough in gray. Source: Treasury via FRED, Schillerpass Fred, New York FedNBER and author’s calculations.

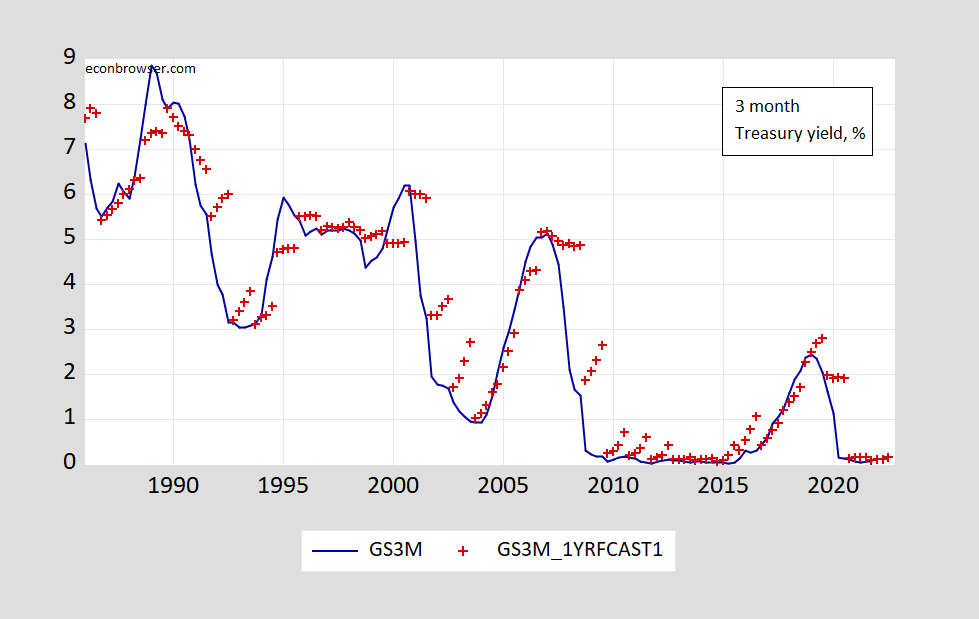

Long-term yields — even after adjusting for risk premia — remain too high, a finding consistent with market watchers overestimating how high rates will be. For some concrete evidence, see the survey of professional forecasters’ expectations and reality of Treasury bond yields over the next 3 months.

image 3: Three-month Treasury yields through the third quarter (blue line) and survey of professional forecasters’ mean forecasts (red +), expressed as a percentage. Green shading indicates early, late. Source: Federal Reserve Board, Philadelphia Fed.

None of the above invalidates the expected assumptions of the term structure (which depend on expected future interest rates). But it does cast doubt on whether future short-term rates will actually be as high as current long-term rates suggest (even after adjusting for the estimated term premium).

{kind=link}

{kind=link}