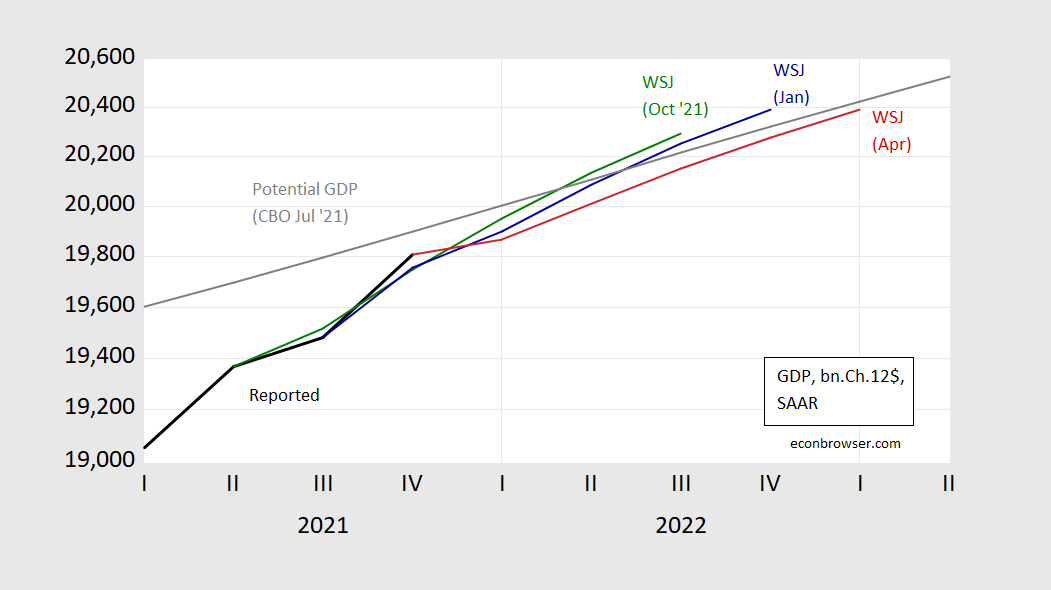

The Russian incursion likely explained most of the downward revision to the WSJ consensus.

figure 1: billion GDP. Ch. 2012 $ SAAR (black), WSJ October 2021 survey (green), WSJ January 2022 survey (blue), WSJ April 2022 survey (red) average forecast, and potential CBO GDP (grey). Sources: BEA, WSJ (various issues), CBO (July 2021) and author’s calculations.

Growth in Q4/Q4 2022 was revised from 3.3% in the January survey to 2.57% in April.

If one believes the CBO’s estimate of potential GDP, then the output gap of the economy is still negative, and there is still a long way to go before full employment. The observed inflation is then interpreted as a cost push, not a demand pull (to use accepted old-fashioned language).

Another piece of evidence consistent with this view is that while inflation expectations rose in late January and early February, they were not volatile (as is typical investigation). This means that disruptions related to the Russian invasion (uncertainty in oil prices, commodity prices, the economy and economic policy) could lead to downward revisions in expectations.

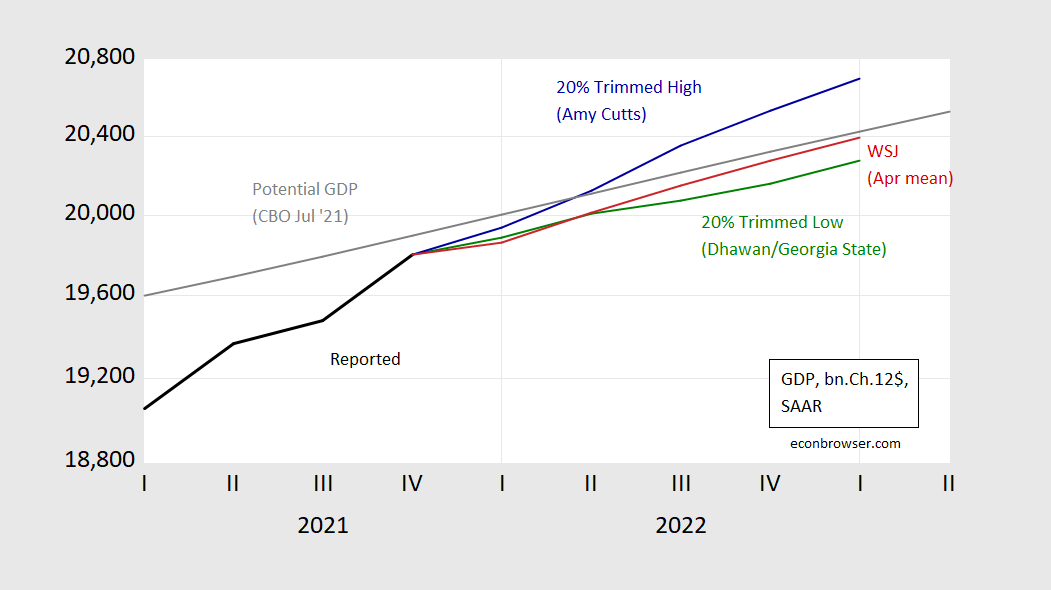

Below are the top and bottom forecasts (Q4/Q4 2022 down 20%).

figure 1: billion GDP. Ch. 2012 $ SAAR (black), WSJ April 2022 survey average forecast (red), 20% Q4/Q4 2022 (blue) and lows (green), and potential CBO GDP (grey). Sources: BEA, WSJ (April survey), CBO (July 2021) and author’s calculations.

Output won’t even reach potential GDP until this quarter (Q2), according to AC Cutts’ bullish forecast.

Note that the recession forecasts we hear are for 2023. Q4/Q4 2023 forecast average growth rate of 2.18% – much higher than Deutsche Bank forecast 0.7% That includes a recession in late 2023.

{kind=link}

{kind=link}