Or why Jason Furman and I get different answers.

- Is core inflation in the U.S. faster than in the euro area during the pandemic? yes.

- Was core inflation in the U.S. higher than in the euro area before the pandemic? yes.

- Is core monthly/monthly inflation in the US higher than in the Eurozone during the pandemic, statistically significant? Do not.

- Is US core monthly/monthly inflation accelerating relative to the Eurozone, statistically significant? Do not.

follow up on this postal.

I examined monthly inflation rates in the United States and the euro area using the log-difference of price levels. The Eurozone HICP index is seasonally adjusted using geometric X-12. Then define the annualized monthly/monthly inflation differential for the US versus country i:

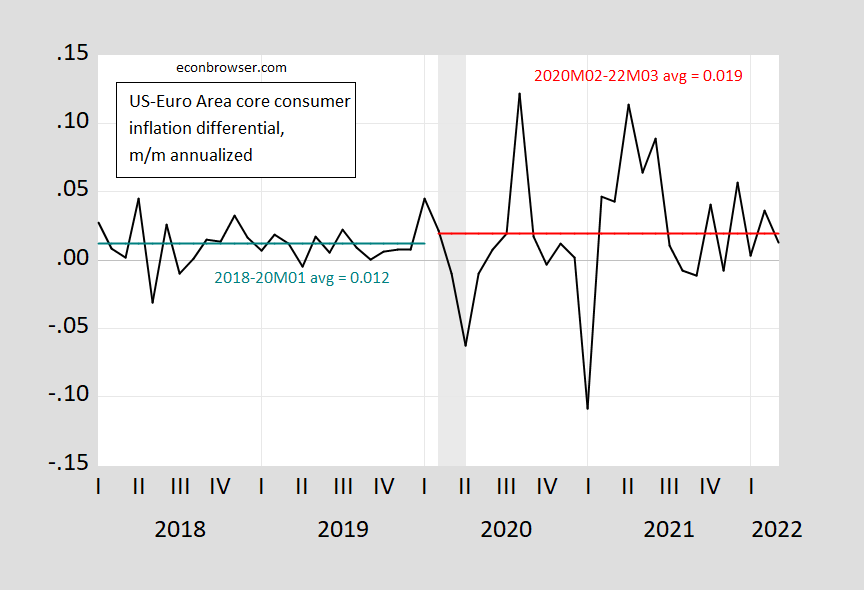

Taking this variable and regressing this object to a constant over the period 2018M01-2020M01, I get an estimate of 0.012 with an HAC standard error of 0.0025 (ie US core inflation on average exceeds Eurozone core inflation by 1.2%). Then do the same regression on 2020M02-2022M03 and get an estimate of 0.019 with a HAC standard error of 0.0109. As a result, the difference between US and Eurozone core inflation widened from 0.012 to 0.019, or 0.007 (0.7%).

How to calculate the difference in average inflation difference? A t-test can be done and the standard errors (essentially a weighted average of the first and second standard errors) are calculated manually. Alternatively, I can run the regression during 2018-2022M03:

![]()

Where coronavirus diseaseTon is a dummy variable that takes the value 1 from 2020M02.

this A sort of The coefficient is the pre-pandemic inflation difference between the US and country i; this b The coefficient is the change in inflation differential after covid. (This diffs-in-diffs approach is preferred because of the compositional aspects of the US series and the Eurozone HICP.)

Using the HAC robust standard error, I found that the estimated b The coefficient for the US-Euro area is 0.007 (HAC robust standard error 0.011).zero-zero t statistic b The coefficients are close to the conventional level of statistical significance. This is partly because (in a mechanical sense) the variability of differences during the pandemic is so great.

figure 1: Monthly core inflation differentials between the US and the Eurozone (black), calculated using log-differences. The cyan line is the mean difference 2018-2020M1; the red line is the mean difference 2020M02-2022M03. The authors seasonally adjusted core HICP for the euro area using geometric census X-12. The NBER uses shades of grey to define the peak and trough dates of the recession. Source: BLS, Eurostat via FRED, NBER and author’s calculations.

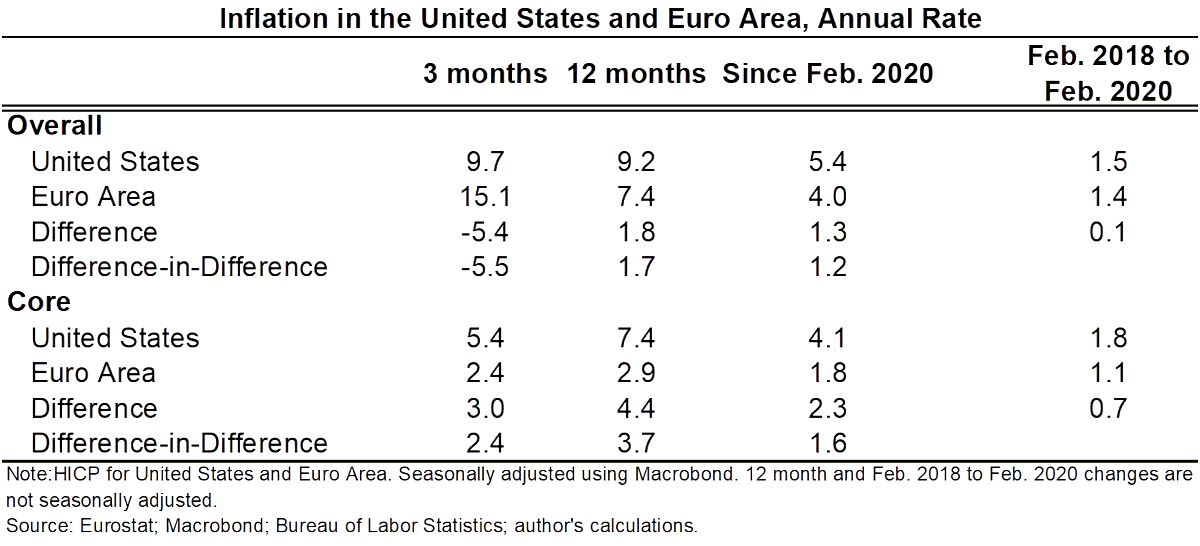

source: Furman (2022).

After some number crunching, I think Jason Furman calculated the before and after growth rates using the slope of the line in Figure 2 below.

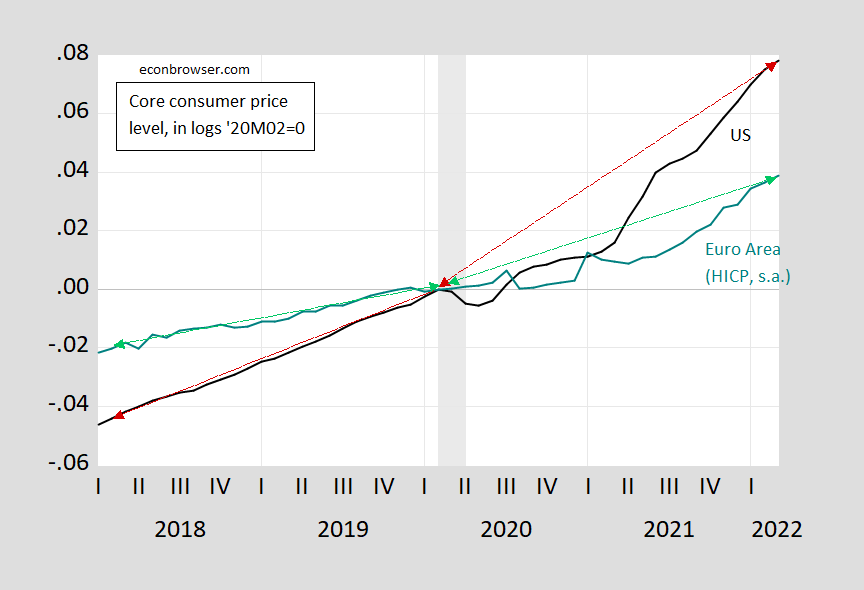

figure 2: US core CPI, sa (black) and euro area HICP core seasonally adjusted (turquoise). The red arrows connect 2018M02-2020M02, 2020M03-2022M03 in the United States, and the green arrows in the euro area. The authors seasonally adjusted core HICP for the euro area using geometric census X-12. The NBER uses shades of grey to define the peak and trough dates of the recession. Source: BLS, Eurostat via FRED, NBER and author’s calculations.

As the slopes of the arrows in both series steepen, inflation is rising in both — but the U.S. has a steeper slope than the euro area.

Both methods are “correct”. If you want to focus on the last 3 months or the last year, you should do what Jason does in the table. If you want to compare pre-pandemic and during the pandemic, you can follow what is in the table (implicit in Figure 2). But you can’t do statistical significance tests like I do. *Personally, I prefer to return the difference in context because that’s how I teach it in class.

* There may be some deep questions about whether the slope method treats CPI or HICP as an I(0) variable, while the inflation rate regression method treats inflation as I(0), but I don’t have the energy to think about it right now.

{kind=link}

{kind=link}