this Bureau of Economic Analysis Announced today, the seasonally adjusted U.S. first-quarter real GDP contracted an annualized 1.4%. What does this portend?

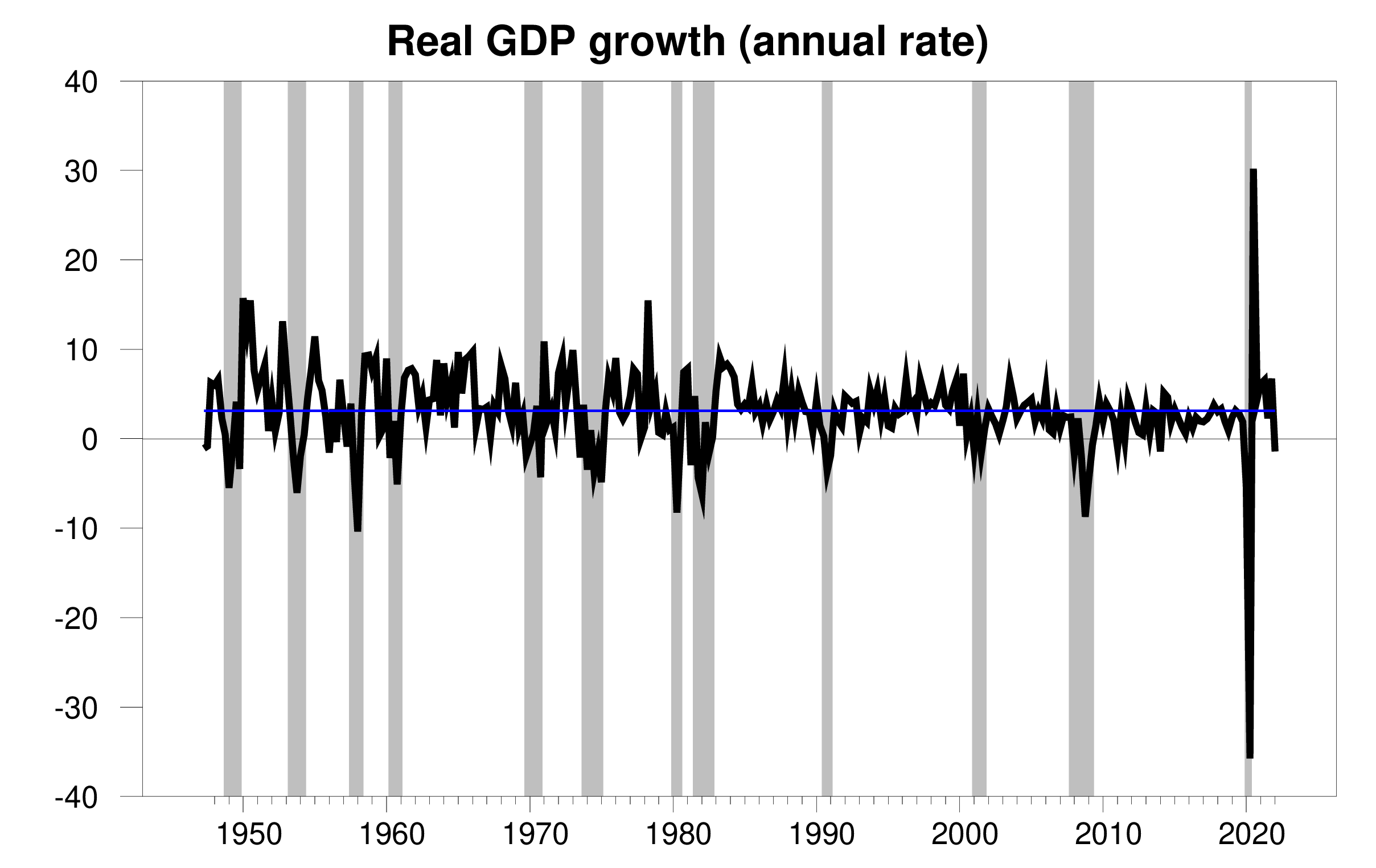

Real GDP annual growth rate, 1947:Q2-2022:Q1, blue is the historical average (3.1%). Calculated as 400 times the natural log difference from last quarter’s GDP.

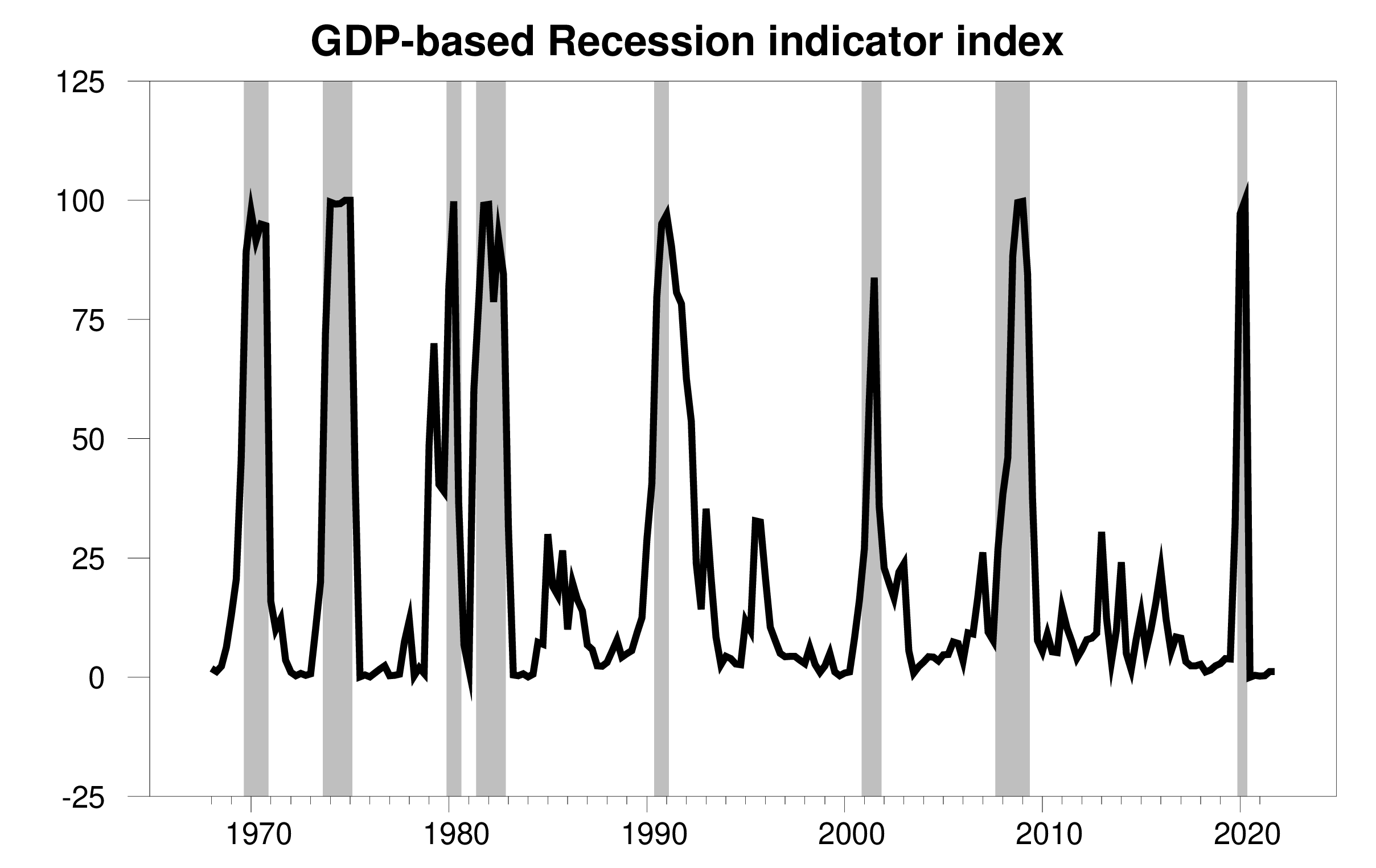

new data leave Economic Browser Recession Indicator Index 1.2%, very clearly indicating that the economic expansion continued at least until the end of last year. This is not a forecast indicator, but an assessment of the state of the economy in the previous quarter (i.e. Q4 2021). We use a quarter delay to allow for data modification (more on that below) and for better accuracy. The index provides the basis for our 15-year-old automated procedure for specifying the start and end dates of recessions. If the index rises above 67%, we will declare a recession.

GDP-based recession indicator index. The plotted values for each date are only based on publicly available GDP data as of the quarter following the date shown, the last date shown on the chart is Q4 2021. The shaded areas represent NBER’s decline dates, which were not used in any way to construct the index.

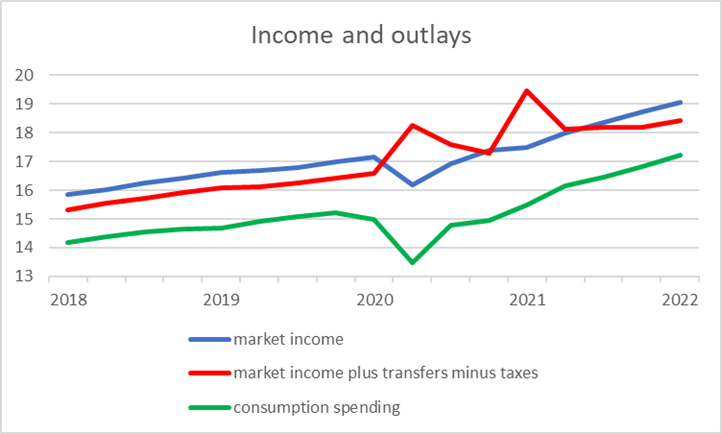

Some may wonder if the withdrawal of fiscal stimulus could be a factor in negative GDP growth. I am skeptical of this possibility. The blue line in the graph below shows personal income excluding taxes and transfers, while the red line adds transfers and subtracts taxes. The March 2020 Coronavirus Aid, Relief, and Economic Security Act and the March 2021 U.S. Relief Program Act resulted in a substantial increase in personal disposable income, with total transfers exceeding the amount of personal taxes collected. Taxes deducting transfers are now back around historical levels. It’s hard to look at this graph and conclude that stimulus related to the red line has been the main driver of green consumer spending. In fact, growth in U.S. consumer spending in the first quarter of 2022 was stronger than in the fourth quarter of 2021.

Blue: Personal income (PINCOME) plus government social insurance contributions (A061RC1Q027SBEA) minus government social benefits to individuals (A063RC1Q027SBEA). Red: Personal income minus personal tax (W055RC1Q027SBEA). Green: personal expenses (A068RC1Q027SBEA).All quarterly data, at quarterly adjusted annual rates, in billions of dollars, from Fred. See BEA Table 2.1 for details.

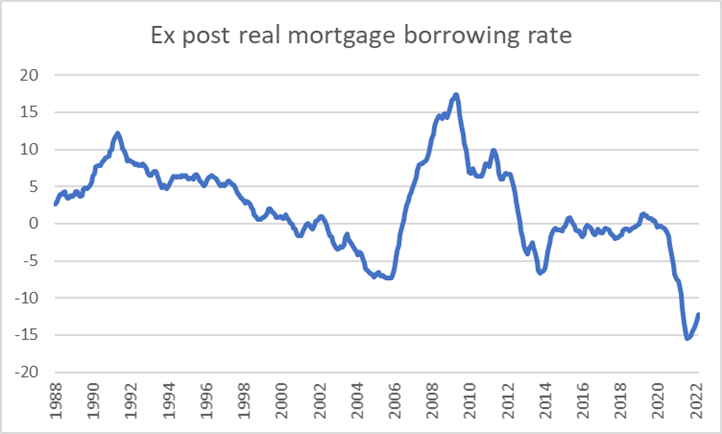

Others may be concerned about the Fed’s plans to raise interest rates. So far, we’ve only seen 25 basis points of that in the federal funds rate, but expectations for more to come have driven 30-year mortgage rates up 200 basis points since the start of the year. But if you borrow at the current 5% rate and see your house price rise by 17% like it did last year, buying a home is still very lucrative. Granted, it’s unclear how long these house price increases will last. But historically, the series plotted below changes very slowly. To be sure, the cycle tends to end in recession as the Fed continues its tightening cycle in an effort to rein in inflation. But we are still too early, and residential fixed investment was slightly stronger in the first quarter than in the fourth quarter.

Nominal interest rate on 30-year fixed mortgages (month-end value of MORTGAGE30US) minus the year-over-year percentage change in the Case-Shiller National Home Price Index (CSUSPHINSA) for the 12-month period ending two months ago, from Fred.

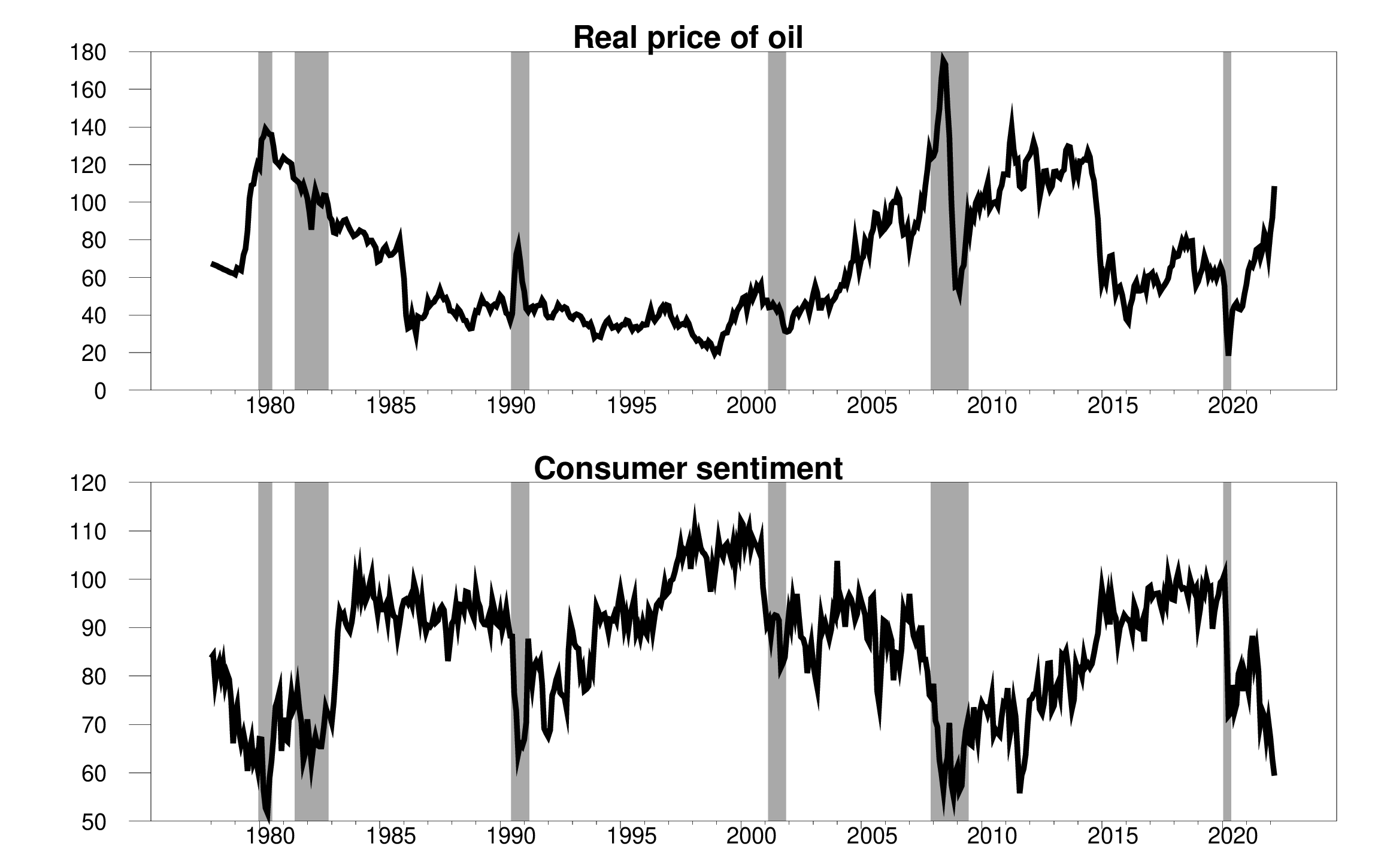

High oil prices are another headwind for the economy. These tend to lead to a drop in consumer sentiment, and current events are no exception. However, current indications are that oil prices in April will eventually be lower than in March, while consumer confidence will be higher than in March.

Top panel: 2022 USD real oil price (WTI divided by CPI). Bottom: University of Michigan Consumer Confidence Survey. Monthly, 1978:M1 to 2022:M3.

Historically, a key point in declining sentiment has been the purchase of consumer durables, especially automobiles. The sequential growth in these areas was actually stronger than the growth in GDP. Auto inventories have been low due to supply chain issues, which seems unlikely to be the main source of the quarter-over-quarter decline. Even if consumers are sluggish in purchasing, replenishment has a lot of room for production gains.

source: Fred.

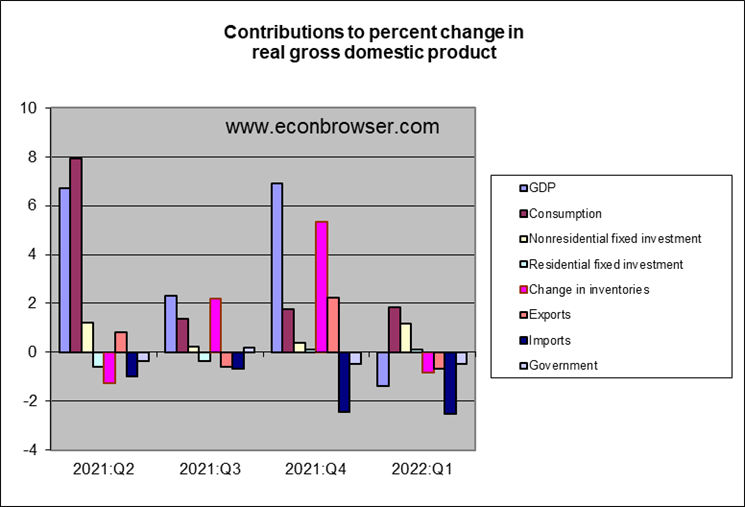

Non-residential fixed investment is another spending component that could see sentiment. But it’s also been there.

The most striking category in the chart above is U.S. exports. Of course, there is no shortage of deeply disturbing events around the world that could lead to a drop in exports. But it’s worth noting that the comparison between Q1 and Q4 (how the numbers are entered in the chart above) looks bad, in part because Q4 exports were very strong. The first quarter still looks pretty solid in terms of export levels rather than quarter-on-quarter changes.

Looking at BEA Table 4.2.2, I was surprised to find that almost half of the decline in US exports in the first quarter compared to the fourth quarter came from the decline in US exports of oil and petroleum products. The Energy Information Administration reports two estimates of this number collected from different sources. A monthly series based on data from refiners and oil transporters showed exports remained strong. A weekly series produced by U.S. Customs and Border Protection alone shows weakness.

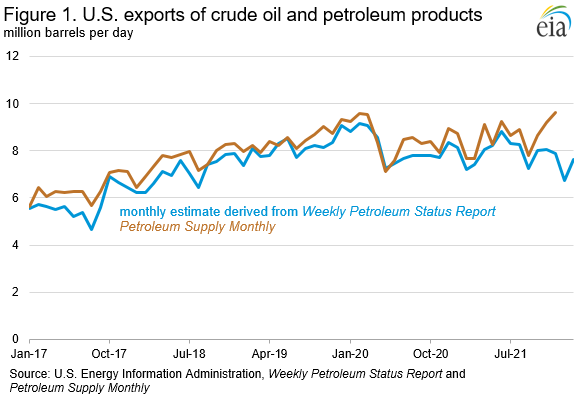

This is EIA assessment difference:

We may have underestimated exports of most products including crude oil, refined motor gasoline, distillate fuel oils, propane/propylene and other oils [our Weekly Petroleum Status Report] Week ending November 2021 to February 18, 2022. We use information from US Customs and Border Protection (CBP) in our WPSR estimates and are consulting with them to determine why.

That’s not to deny that there are plenty of dark clouds to watch, including another round of COVID-related shutdowns in Asia and the ongoing horrific tragedy in Europe. But it would be a big mistake to conclude that these and other concerns have already led to a recession in the United States.

{kind=link}

{kind=link}