Along with the release of IHS-Markit’s monthly GDP, we have the following charts of key indicators noted by the NBER BCDC.

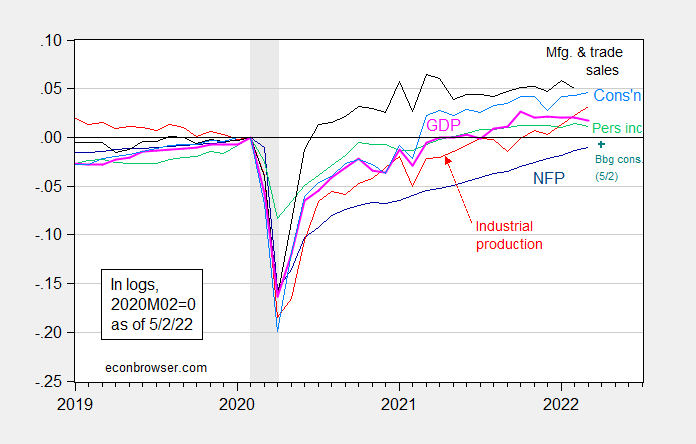

figure 1: Nonfarm Payrolls (dark blue), April NFP Bloomberg Consensus as of May 2 (blue+), industrial production (red), 2012 excluding transferred personal income $ (green), 2012 manufacturing Industry and trade sales $ (black), consumption in Ch.2012$ (light blue) and monthly GDP in Ch.2012$ (pink), all log normalized to 2020M02=0. NBER defines recession dates, peaks and valleys, shades of gray. Source: BLS, Federal Reserve, BEA, via FRED, IHS Markit (nee Macroeconomic Advisers) (published May 2, 2022), NBER, and author’s calculations.

The monthly GDP data is interesting because it provides some insight into the overall output trajectory (ie, decline).

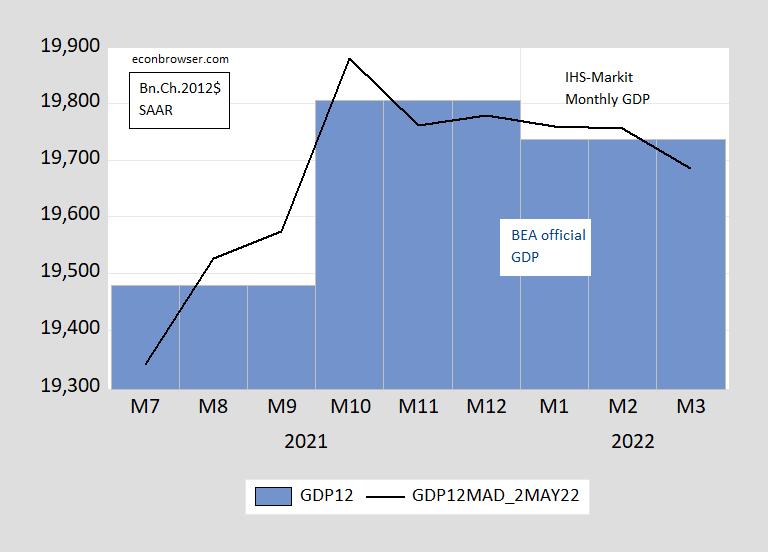

figure 2: BEA releases GDP (first quarter ahead) (blue bar) and monthly GDP (black line), both in billions. 2012 $ Sal. Source: BEA (Q1 advance) and IHS-Markit (May 2, 2022).

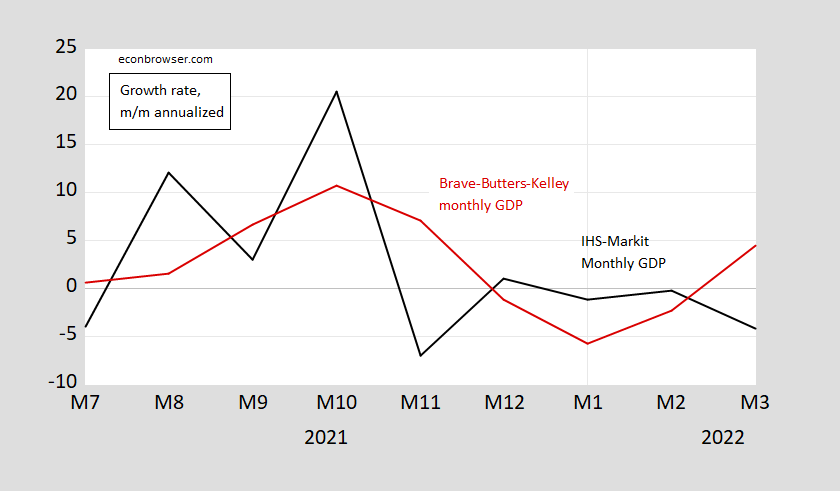

There are several tracking measures for GDP. IHS-Markit (formerly Macroeconomic Advisors) is probably one of the longest reporting companies. The Chicago Fed also reports monthly GDP growth (Brave Butters Kelly Index). Here are two series compared during the same period.

image 3: Monthly GDP from IHS-Markit (black line) and Chicago Fed (red line), m/m annualized, %. Source: IHS-Markit (May 2, 2022) and Chicago Fed via FRED.

Friday’s jobs data (up 400,000 according to the Bloomberg consensus) will provide an initial read on the economy’s trajectory.

{kind=link}

{kind=link}