Every decade, the debate over the dollar’s role as the world’s dominant currency resurfaces: Will America’s currency be replaced by other countries’ currencies? In the 1970s, it was the yen or the German mark. Then in the economic and monetary union, the euro is seen as a competitor. Over the past decade, the renminbi has played as aspirational a role as possible. Where will we stand in 2022?

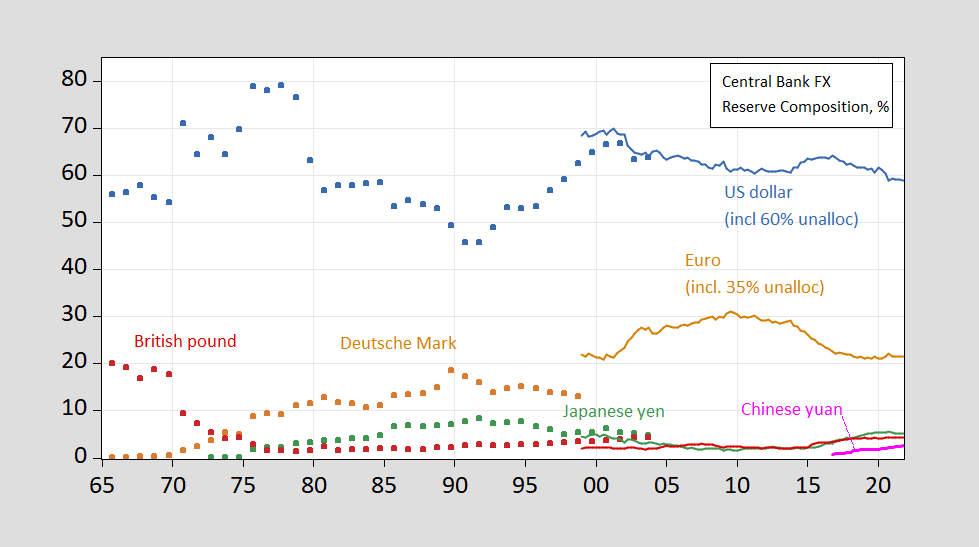

Before answering this question, it’s important to remember that one thing that has proven true over the past 40 years is the persistence of the dollar’s dominance, as shown in Figure 1 – during the global financial crisis and the coronavirus during the pandemic. The U.S. dollar remains the dominant currency held by central banks around the world. While there is some uncertainty about the exact share of each currency (as some central banks do not report the composition of their holdings), the dollar makes up around 60% of the total, well above the share of the euro in the low 20s. Despite the high-profile appreciation of the Chinese currency, the renminbi, its share only rose to 2.6% by the end of 2021.

figure 1: Shares of foreign exchange reserves for USD (blue), Deutsche Mark (orange square), EUR (orange line), GBP (red), JPY (green), and RMB (pink). Sources: Chinn and Frankel (2008), and IMF COFER.

If we look at other aspects of money’s role – as a unit of account, medium of exchange and store of value – it is not clear whether the dollar’s dominance is seriously threatened. About 40% of world trade is denominated in dollars, slightly more than the euro. In terms of foreign exchange transactions, the U.S. dollar remains the dominant currency, accounting for 88% of 200% of the total transaction value. The U.S. dollar remains the leader in the international messaging of financial transactions (i.e. via SWIFT), accounting for more than 40% of transaction activity. The euro is a close second, at around 35%. Then why wring your hands?

Sanctions counterattack

As the sanctions regime imposed on Russia appears to have taken a severe toll on the economy, doubts have been raised over the dollar’s dominance. Some argue that this manifestation of vulnerability will prompt other countries to wean themselves off the dollar.

Part of the farce comes from sanctions on the central bank of a large country because the monetary authority is believed to function as protected. In this case, the United States and Western allies have threatened to sanction financial institutions, including the Russian Central Bank, that conduct activities with Russian banks. But a large part of Russia’s foreign exchange reserves are held in Western central banks. Not only are financial transactions restricted, the Russian Central Bank is also unable to tap into its reserves of around $100 billion.

This apparent success contrasts with conventional wisdom about the effectiveness of financial sanctions. Over the past few decades, the United States has imposed economic sanctions as a means of trying to change the behavior of other countries, from Cuba to Libya to Iran. The United States is trying to lure Iran into a deal to limit nuclear proliferation, including sanctions, some of which have been dubbed “smart sanctions” — targeting individuals and industries, not the economy as a whole. While the view of sanctions effectiveness is more valid after the brief success of the Joint Comprehensive Plan of Action (JCPOA) involving Iran, doubts remain that sanctions can deter or limit further Russian aggression in Ukraine.

The overall damage to the Russian economy has brought a new dawn to the effectiveness of sanctions. The Russian economy is expected to shrink by 30% by the end of 2022. What’s more, the long-term effects of cutting the economy from Western technology and imports could set the Russian economy back decades. The ruble has returned to pre-war levels, but this apparent resilience is only scratching the surface; the recovery has been achieved by imposing strict capital controls, restricting foreign currency purchases and forcing companies to hand over export earnings earned in foreign currency.

What makes the effect of sanctions even more surprising is that Russian policymakers have been shielding the economy from economic sanctions in the years following the 2014 invasion of Ukraine. In particular, a large amount of foreign exchange has been accumulated. All this seems to be a testament to the enormous power that the dollar’s special status as the world’s currency has given the United States.

Will this dramatic presentation inspire focused action away from the dollar in a way that has never happened in the past? I think the answer is no.

Say goodbye to dollars?

The first reason I think it’s unlikely is that in many ways it’s very difficult to get rid of the dollar. Consider foreign exchange reserves: Central banks tend to accumulate foreign exchange reserves in currencies that earn foreign exchange—whether it be exports or capital inflows. A large portion of export earnings in world trade is denominated in dollars. About 40% of cross-border debt is issued in U.S. dollars. In order to change the currency’s share in reserves away from the ratio earned, the central bank must make up its mind to sell dollars and buy other currencies, such as euros, pounds or yen. It would be an expensive proposition because assets denominated in these other assets are less liquid and therefore harder to get in and out of. In other words, diversifying reserve assets from the dollar would be an expensive proposition.Countries will have to bear the cost in the long run (holding less safe assets) in order to reduce their reliance on dollar transactions in the event of a conflict

The second reason I don’t think there’s a concerted move away from the dollar is that, in some ways, doing so would learn the wrong lessons from the events of 2022. It’s the multilateral nature of sanctions that makes them so effective, not the fact that the U.S. dollar is involved. Western central banks have frozen their holdings of Russian foreign exchange reserves (only a portion of which is held by the Russian Central Bank), so of the $160 billion at the end of February, only about $60 billion is available.

For example, Chinese policymakers have apparently concluded that, at least in the short term, there is little way to shield themselves from the kind of sanctions imposed on Russia (their The idea is this). At a high-level meeting of regulators and bankers in April, leaders concluded that such treatment would destroy China’s economy, given the myriad trade and financial ties between the West and China. Even now, Chinese companies are careful to avoid dealing with sanctioned Russian banks to prevent themselves from being sanctioned. But what drives Chinese restraint is not the dominance of the dollar, but the dominance of Western finance and financial infrastructure.

But what about the renminbi?

Throughout the 2010s, China’s rise was reflected in its overtaking the size of the US economy (at least in terms of purchasing power parity). Clearly, it is only a matter of time before an international dominant currency. The inclusion of the renminbi in the International Monetary Fund’s Special Drawing Rights (SDR) seems to herald the era of the renminbi. Between 2015 and 2020, the renminbi’s share of foreign exchange holdings rose from zero to 2%. RMB turnover increased from 0% in 2001 to 9% in 2019 (out of 200%).

But as long as there are strict restrictions on cross-border transactions, no single currency can become the dominant international currency. For some time now, China seems to have opted for a more open international financial system. However, since Xi Jinping came to power, greater financial opening – and the accompanying reduction in economic autonomy – seems to have ceased to be a priority. Well, by default, the yuan’s path to dominance is now canceled.The renminbi is already an important regional currency and will become more so, but its direction This Global currencies are now blocked.

so what happens

The U.S. dollar will maintain its dominance because the network externalities associated with being a major currency are very strong. The dollar’s dominance is so strong that it is hard to imagine a rapid erosion. This does not mean that other currencies may not grow in importance (eg, AUD, CAD, etc.) and that other systems for clearing and messaging transactions may evolve enough to compete with existing incumbents. In the next decade, the international monetary system may look much the same as it does now.

{kind=link}

{kind=link}