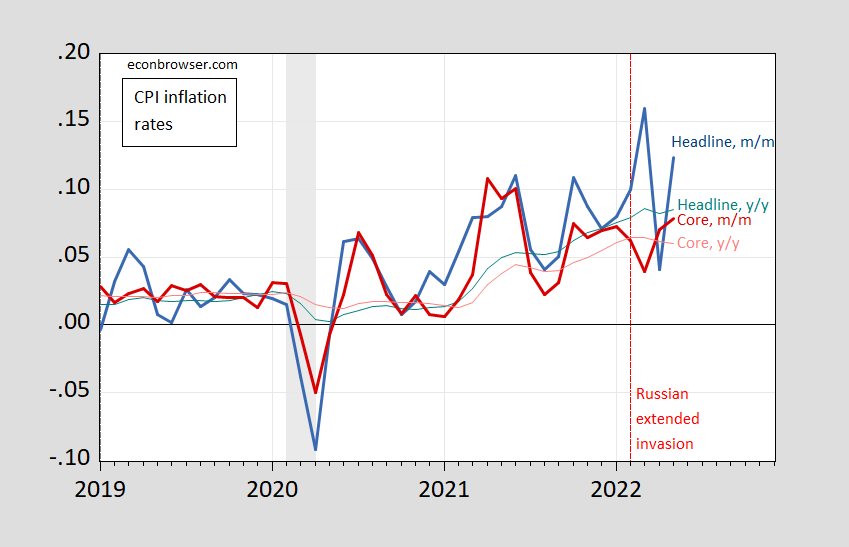

MoM and YoY, as well as headline, chain, sticky price, 16% cut and (April) PCE deflator.

First, keep in mind the difference between m/m (more informative about contemporaneous conditions) and y/y (more backward looking).

figure 1: Headline CPI MoM Inflation (blue), Headline CPI MoM Inflation (Teal), Core CPI MoM Inflation (Dark Red), Core CPI YoY Inflation (Pink) . NBER Defined Recession Dates (Peak-Valley) Shades of Grey. Dotted red line for Russia’s extended invasion of Ukraine. Source: BLS, NBER, and author’s calculations.

Note that while the y/y headings have peaked (since 1981), m/m has fallen (though not as much as one would like). On the other hand, month/month core inflation rose, signaling a poor inflation trend.

Second, the different estimates of monthly headline inflation shown in Figure 2 show some promising signs.

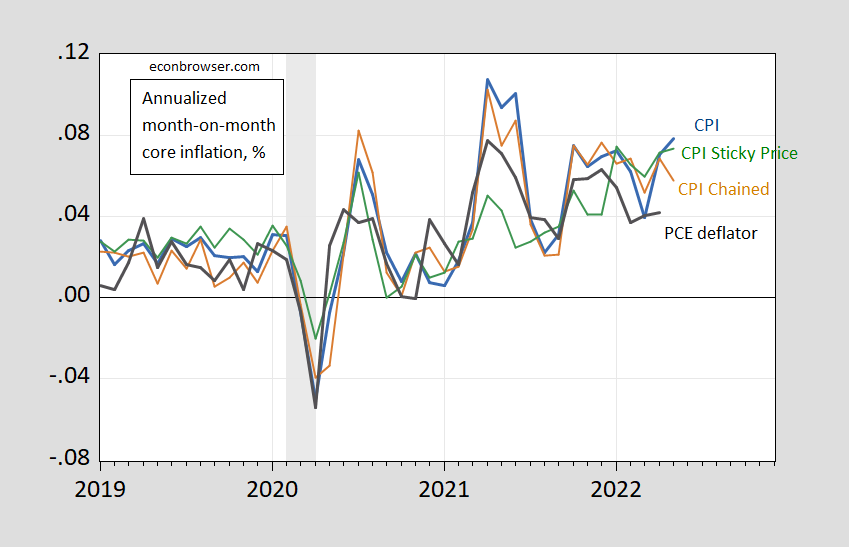

figure 2: CPI month-on-month inflation (blue), chained CPI (brown), 16% adjusted CPI inflation (red), sticky price CPI inflation (green), PCE deflator (black), all in decimal form (i.e. , 0.05 means 5%). Seasonally adjusted chained CPI using Geometric Census X13 (brown). NBER-defined recession dates (peaks and valleys) shades of gray. Source: BLS, BEA, NBER and author’s calculations.

The Cleveland Fed’s near-term forecast for PCE annualized PCE inflation for the month to June 11 is 8.9%, rebounding from an actual preliminary 3.0% in April.

Adjusted and sticky price CPI inflation has not been that important over the past month. The trim < title suggests that price increases are concentrated in certain fast-rising categories. Sticky < title indicates that flexible prices are doing most of the price changes.

Third, the May uptick was not good news for the core measure (even though the ratio was lower than last April):

image 3: Chain inflation of core CPI (blue), chained core CPI (brown), sticky price core CPI inflation (green), personal consumption expenditures core deflator inflation (black), all in decimal form (ie 0.05 means 5%) . Seasonally adjusted chained CPI using Geometric Census X13 (brown). NBER-defined recession dates (peaks and valleys) shades of gray. Source: BLS, BEA, NBER and author’s calculations.

The Cleveland Fed’s near-term forecast for core PCE inflation in May is 5.7%, up from a preliminary 4.2% in April.

This provides a good overview of the impact of CPI releases brookings slice (Including the views of Furman, Edberg, and Wolfers).Look CEA Twitter thread Too. The contribution of housing costs is significant because this factor is likely to persist:

Together, these housing cost measures contributed about 24 basis points to monthly core CPI inflation, compared with the pre-pandemic average of 11 basis points, reflecting the challenges in the housing market.

The 5-year inflation breakeven rose to 3.15% from 3.08%, still below the March 25 level of 3.59%. The 5-year 5-year forward breakeven remains largely unchanged (down 3 basis points).

{kind=link}

{kind=link}