July Wow renew:

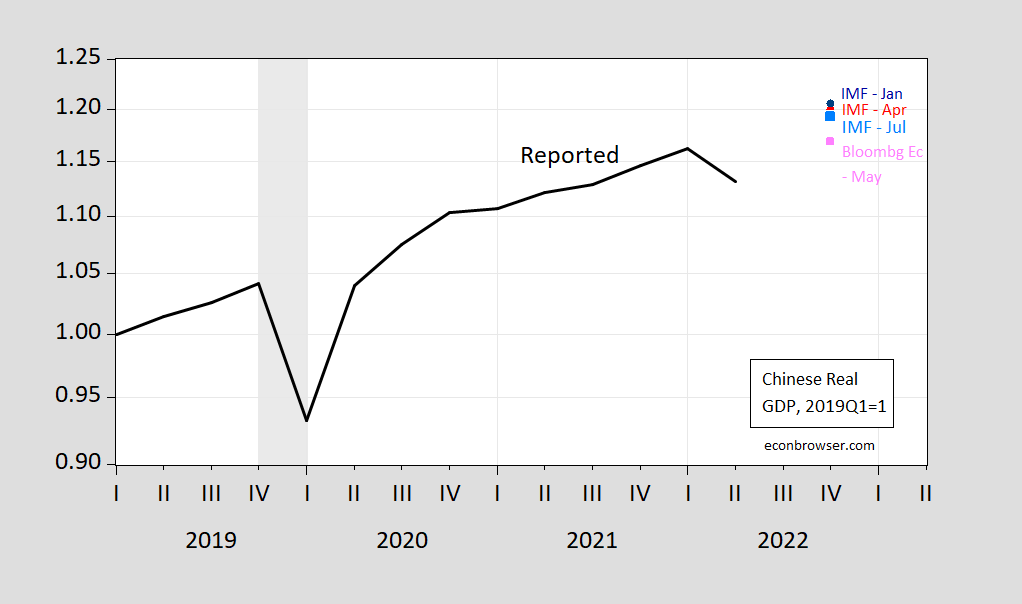

In China, further lockdowns and a deepening housing crisis resulted in a 1.1 percentage point downward revision to growth, with significant global spillovers.

This is shown in the graph below as the latest price cut for forecast growth rates and implied GDP levels:

figure 1: China’s 2019 real GDP=1 (black), and forecasts from the IMF World Economic Outlook, January (blue circles), April (red triangles), July (sky blue squares) and Bloomberg Economics (pink squares) ). GDP calculated by accumulating q/q reported growth rates. ECRI defines the recession date from peak to trough, shaded in grey. Sources: National Bureau of Statistics, IMF World Economic Outlook (various issues), Bloomberg Economics, ECRI, and author’s calculations.

Newest World Economic Outlook forecast This means that the end of 2022 will be at the same level as Deutsche Bank and Goldman Sachs forecast in May (see here postal).

More details:

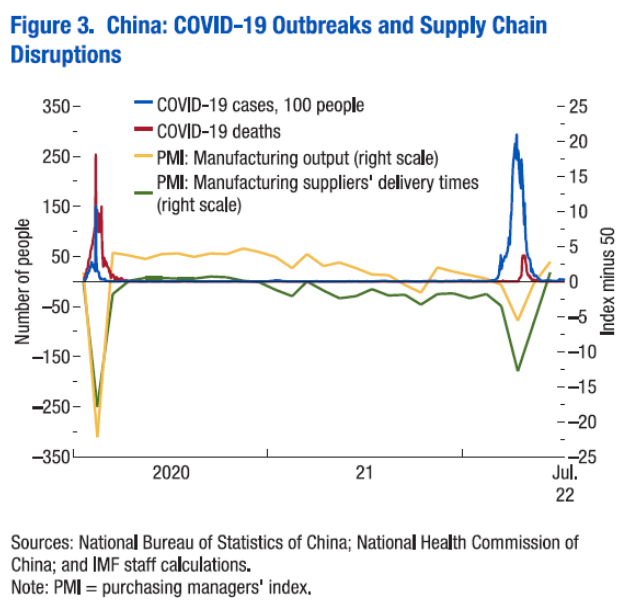

The COVID-19 outbreak and travel restrictions have widely and severely disrupted economic activity as part of the authorities’ zero-COVID strategy (Figure 3). Shanghai, a major global supply chain hub, entered a strict lockdown in April 2022, forcing a citywide shutdown of economic activity for about eight weeks. Driven by a drop in consumption, real GDP contracted sharply by 2.6% sequentially in the second quarter, the largest drop since the 10.3% drop in the first quarter of 2020 when the pandemic began. Since then, the more contagious variant has led to a worrying surge in COVID-19 cases. The worsening crisis in China’s real estate sector has also weighed on sales and real estate investment. China’s economic slowdown has global consequences: The lockdown has exacerbated disruptions to global supply chains and a drop in domestic spending, which is reducing demand for goods and services from China’s trading partners.

Figure 3 shows the impact of the pandemic on manufacturing activity and the government’s response.

{kind=link}

{kind=link}