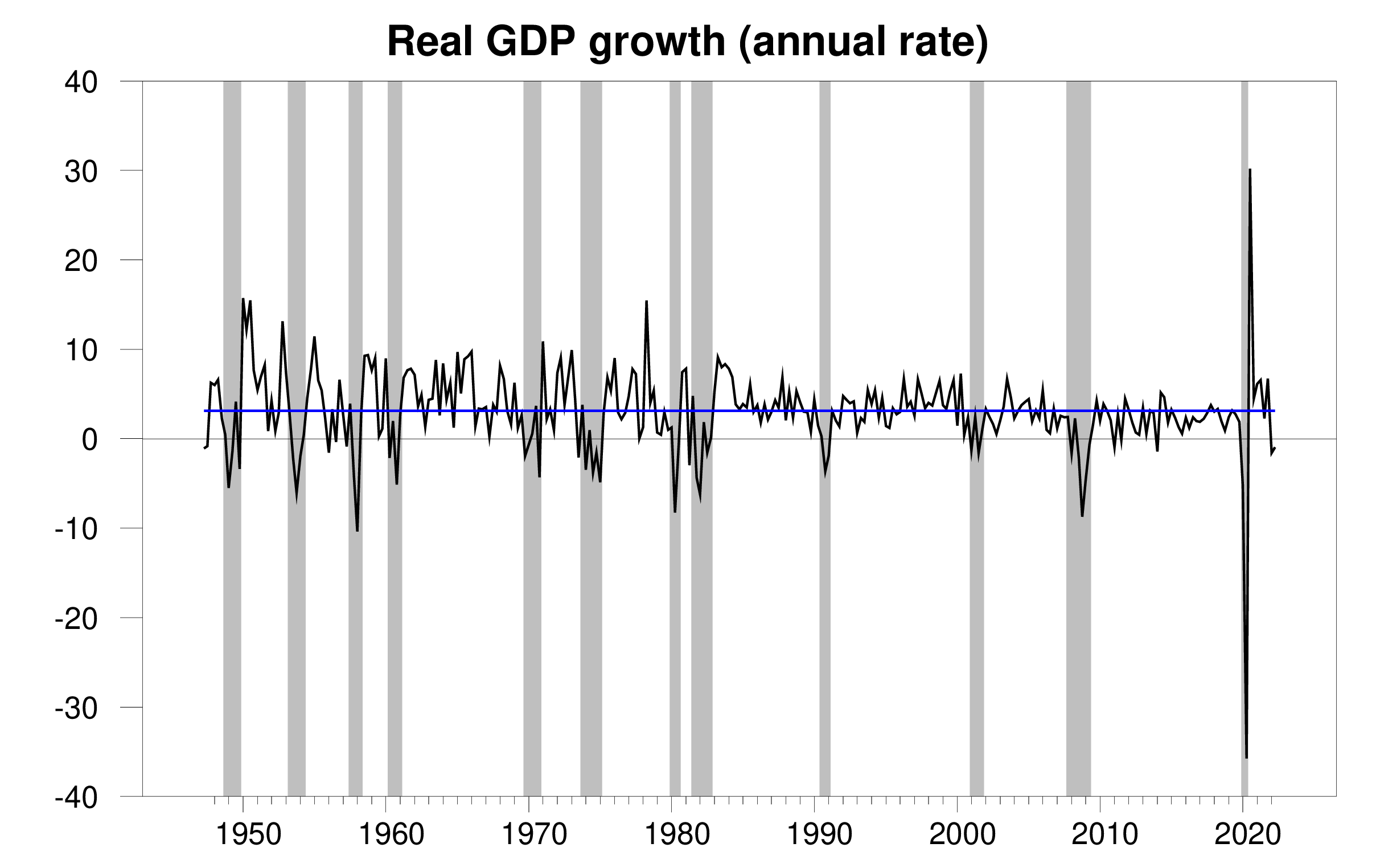

This Bureau of Economic Analysis Announced today, the seasonally adjusted U.S. first-quarter real GDP contracted an annualized 0.9%. That kept real GDP down for two consecutive quarters, a rule of thumb for declaring a recession. The current economic weakness is sure to develop into a recession. But the evidence is not convincing that a recession has begun.

Real GDP annual growth rate, 1947:Q2-2022:Q2, blue is the historical average (3.1%). Calculated as 400 times the natural log difference from last quarter’s GDP.

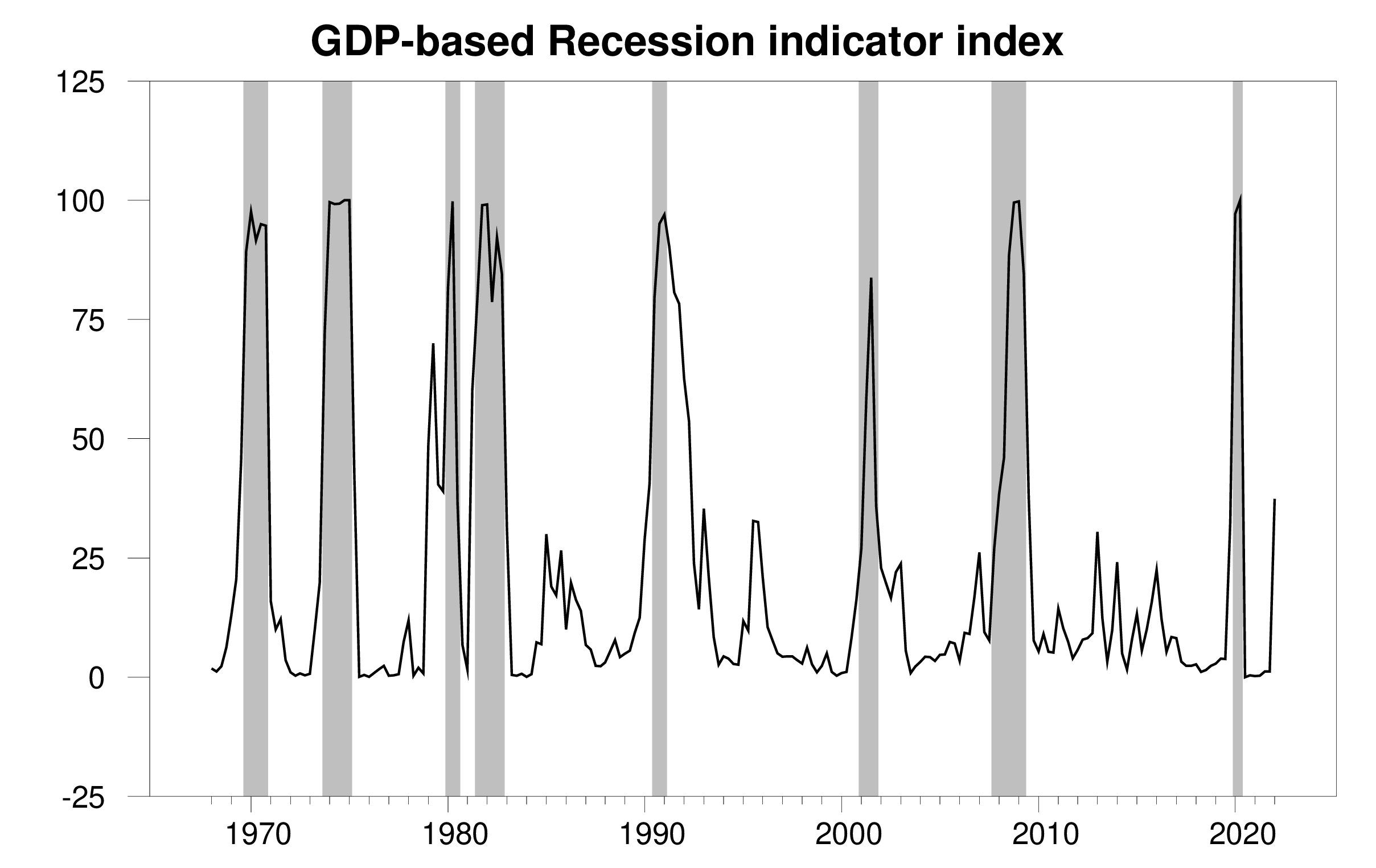

The new data improves Economic Browser Recession Indicator Index As high as 37.4%, flashing obvious warning signs. This is an assessment of the economic situation in the previous quarter, the first quarter of 2022. The index takes into account the fact that we have now seen two consecutive quarters of gross domestic product declines, but still finds inconclusive evidence that the U.S. economy started a recession in the first quarter.When Marcelle Chauvet and I The index was first developed 17 years ago, we announced that we would only declare a recession when the index rose to 65% (see pages 14-15) Our original paper). If the third-quarter GDP report causes the index to rise above 65%, we will declare a recession at that point and use the full range of revised historical data available at that time to determine the date when the recession is likely to begin. At Econbrowser, we have followed this procedure closely as data unfolded in real time for the past 17 years, successfully determining the start and end times of two recessions in real time since we started this blog.

GDP-based recession indicator index. The plotted values for each date are only based on publicly available GDP data as of the quarter following the date shown, the last date shown in the graph is Q1 2022. The shaded areas represent NBER’s decline dates, which were not used in any way to construct the index.

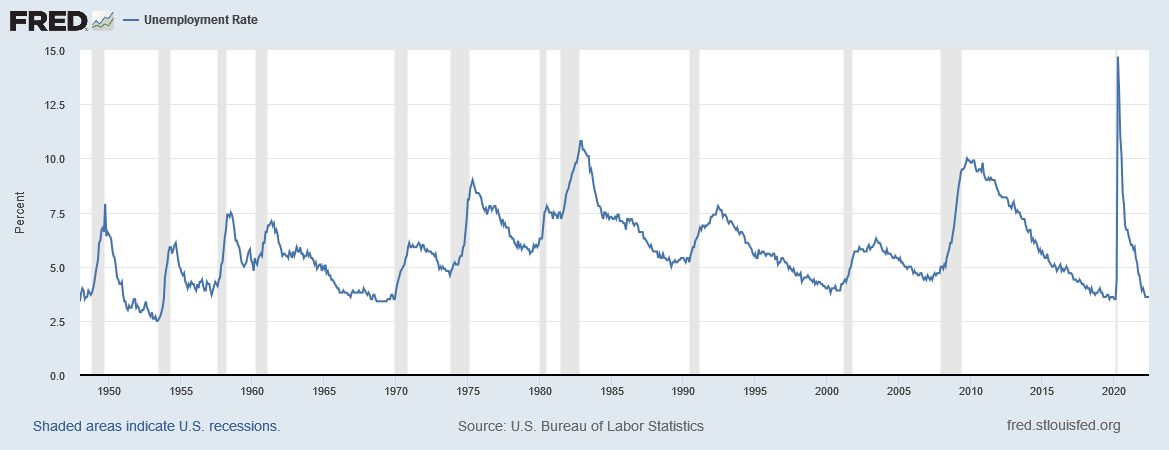

The index is based on GDP data only. But other indicators reinforce the conclusion that you cannot clearly say that a recession has begun. The sharp rise in unemployment is one of the defining features of every historic recession. How can we be in a recession for 6 months with the unemployment rate still at 3.6%?

Nonetheless, a loyal reader reminded me that I did not small economy watcher up to date. This is a more subjective assessment of aggregate information on various economic indicators.I am saddened to report that he is now completely transformed  .

.

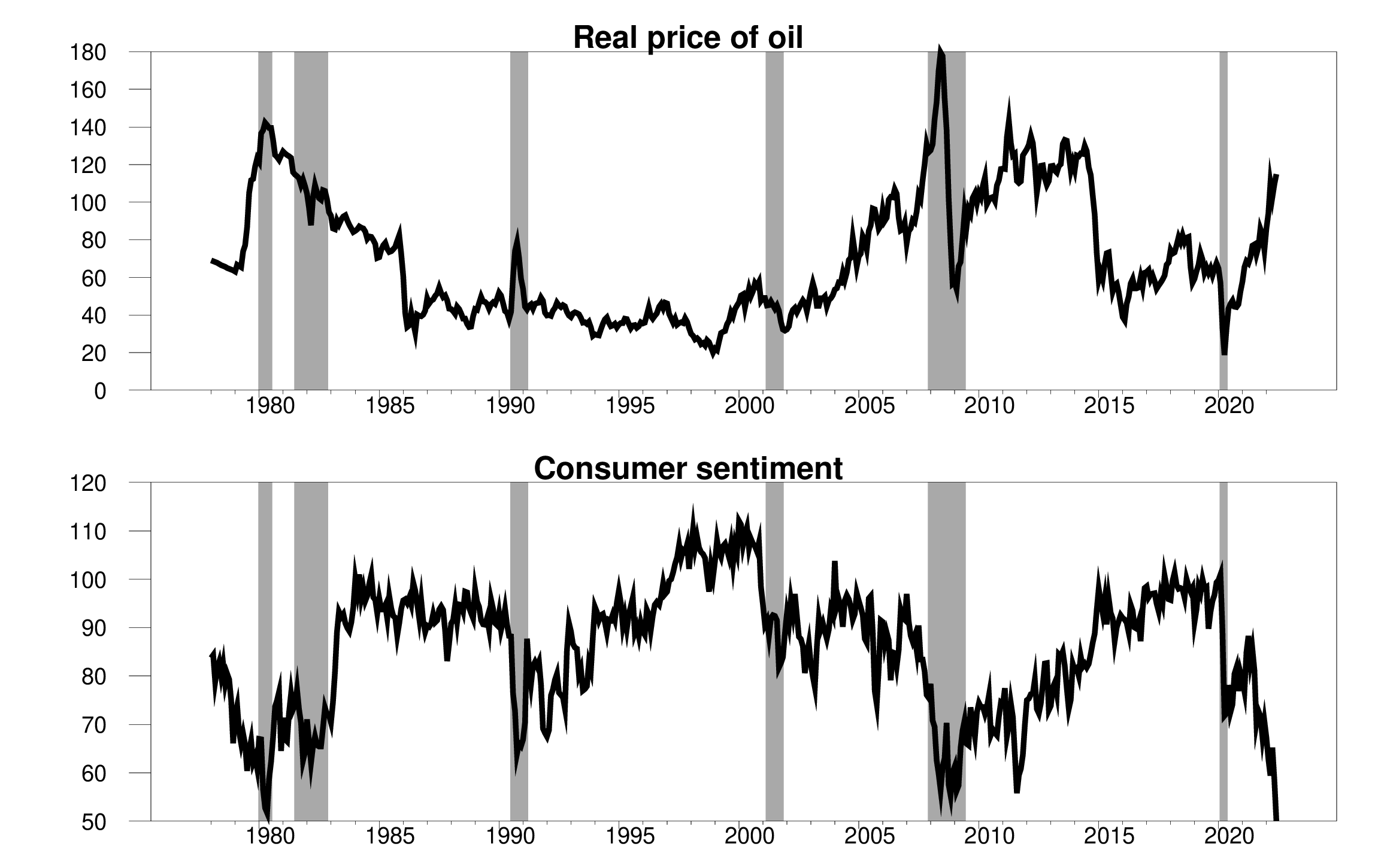

ten out of twelve Crude oil prices have risen sharply since before the U.S. recession since World War II. If 2022 does develop into a full-blown recession, that number will be 11 out of 13. One of the mechanisms by which soaring oil prices contributed to the historic downturn was a marked deterioration in consumer sentiment. Of course that’s part of the story.

Top panel: 2022 USD real oil price (WTI divided by CPI). Bottom: University of Michigan Consumer Confidence Survey. Monthly, 1978:M1 to 2022:M6.

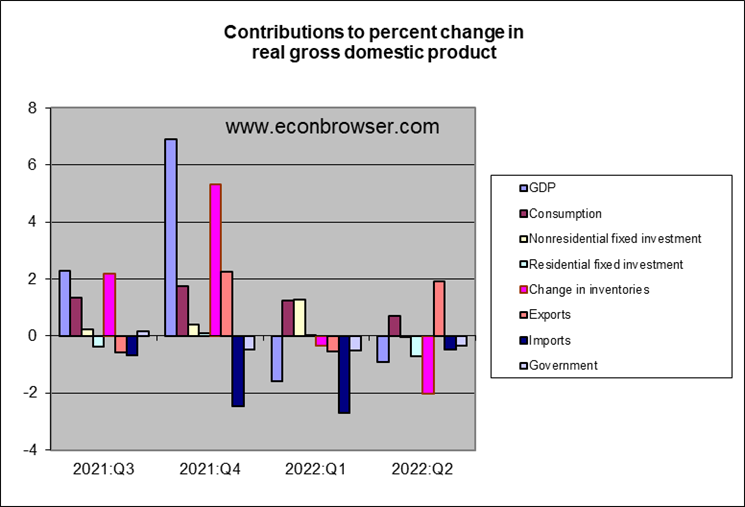

Worried consumers have undoubtedly contributed to the weak growth in real consumer spending so far this year. But the single biggest contributor to negative GDP growth in the second quarter was a drop in inventories. More goods are sold than are produced. Inventory build-up was one factor that made Q4 2021 growth look strong, and the decline now is one factor that made Q2 2022 growth weak. Last year’s real final sales were more stable than real GDP.

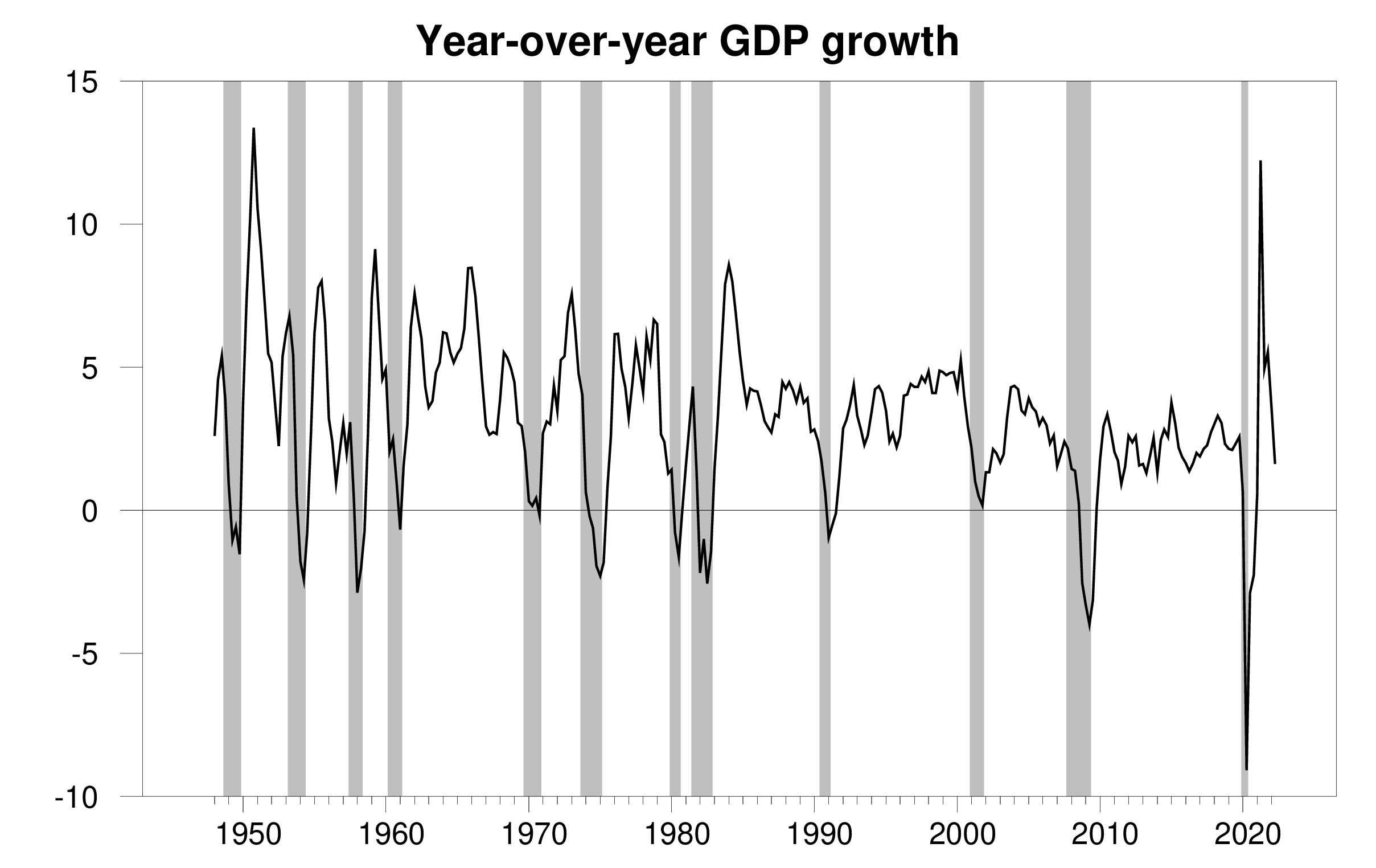

Compared to the same period last year, GDP growth was less worrisome.

An odd feature of the second-quarter GDP data was the seemingly robust exports. Real exports increased by $100 in the second quarter, with one-fifth attributable to oil and petroleum products.but this just corrects a abnormal drop Oil exports in the first quarter report. Oil exports are now back at levels last year in the fourth quarter. My view is that the quarterly export growth was stronger than the first quarter report and weaker than the second quarter report.

The biggest worry for the future is housing. It’s too early for the Fed’s tightening cycle to show up in homebuilding spending. But if the Fed keeps raising interest rates, it will definitely do so eventually. If the current economic slowdown is indeed the beginning of the 13th post-war recession, it may well be the deciding factor.

Bottom line: No recession so far, but plenty to worry about !

{kind=link}

{kind=link}