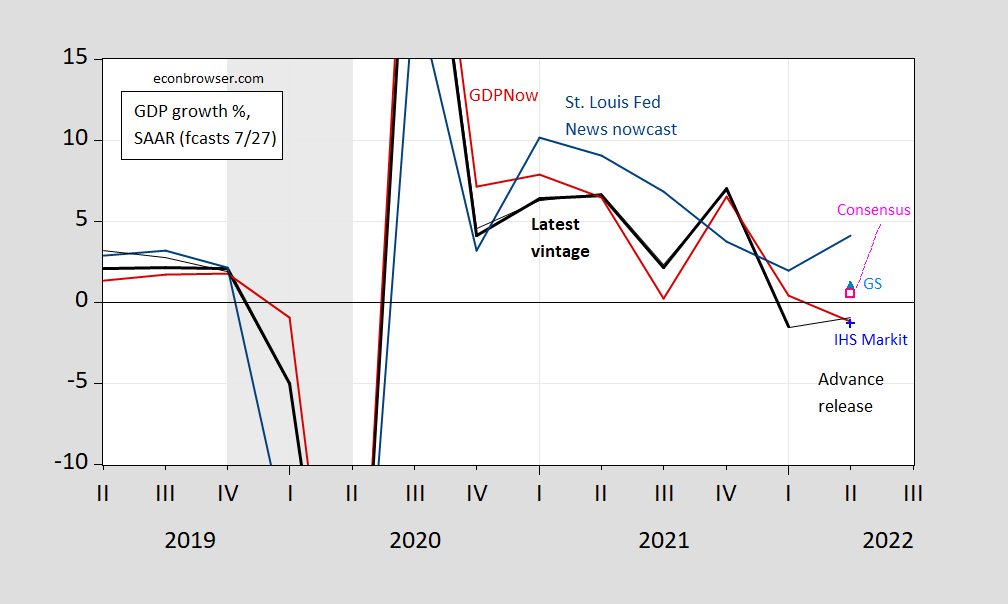

The quarter-on-quarter growth rate for the second quarter was 0.9%, 1.3 percentage points lower than market expectations (SAAR), but higher than GDPNow and IHS-Markit (0.4%, 0.5%, respectively).Although during the period 1996-2020, the average revisions advanced to the third edition were essentially zero (see Bank of East Asia), in the last 5 quarters (2021Q1-22Q1), they were 1.9 percentage points (MAR 12.9 percentage points, RMSR 6.8 percentage points). That said, the revision characteristics seem to have changed from Advance to 3rd (though I didn’t test for statistical significance), Advance revised upwards at launch.

figure 1: Real advance GDP growth rate (thick black), latest year (thin black), Atlanta Fed GDPNow 7/27 (red line), St. Louis Fed News Index 7/22 (turquoise line), IHS Markit 7/27 (sky blue line) color triangle), Goldman Sachs (blue+) on 7/27, Bloomberg consensus as of 7/27 (open square in pink), all expressed as a percentage, SAAR. The NBER uses shades of grey to define the peak and trough dates of the recession. sal. Source: BEA, BEA via ALFRED, Atlanta Fed, St. Louis Fed via FRED, IHS-Markit, Goldman Sachs, Bloomberg and NBER.

The fifth quarter is a small sample, so don’t take too much from the average revision (that is, with a small sample, there is a lot of uncertainty around point estimates). But keep some things in mind.

As for moving forward to the end, over the 1996-2020 period, the MAR was 1.2 ppts and the RMSR was 0.9 ppts, although the average correction was zero. For me at least, this suggests that there will be more progress on the final revision in 2021-22.

{kind=link}

{kind=link}