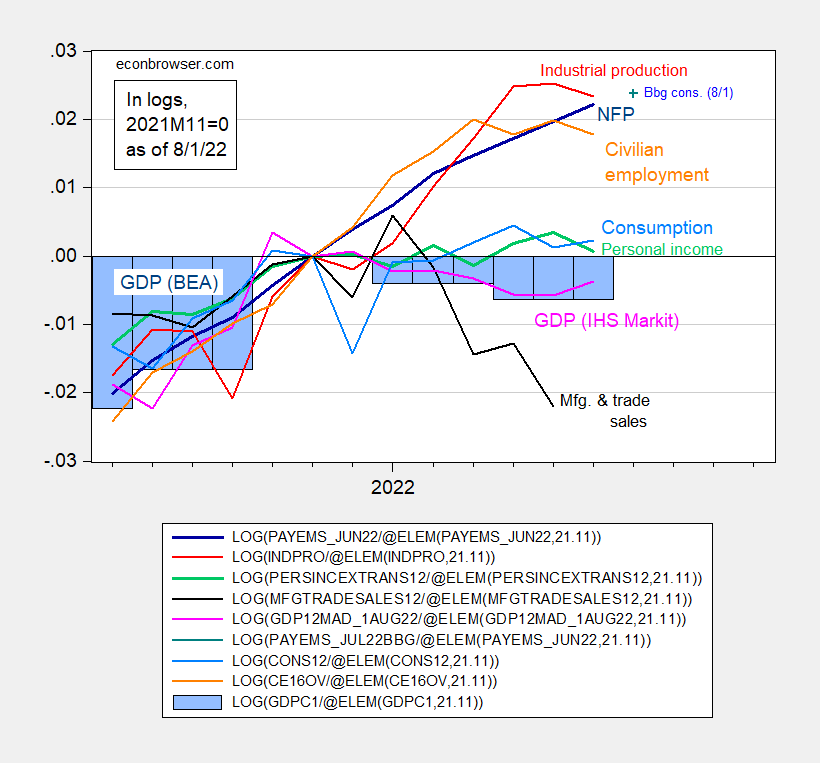

If GDP is the determining factor NBER determined business cyclethis is what the picture looks like (normalized in the middle of Q4):

figure 1: Nonfarm Payrolls (Dark Blue Bold), Bloomberg Consensus as of Aug. 1 (Blue+), Residential Employment (Orange), Industrial Production (Red), 2012 excluding Transferred Personal Income (Green Bold) ), manufacturing and trade sales in 2012 (black), consumption in 2012 (light blue) and monthly GDP in 2012 (pink), official GDP, advances in Q2 2022 (blue bars) , all log normalized to Nov-2021=0. Sources: BLS, Federal Reserve, BEA via FRED, IHS Markit (nee Macroeconomic Advisers) (published Aug. 1, 2022), NBER, and author’s calculations.

In addition to the official BEA GDP and IHS Markit’s monthly GDP (not currently on the list), these six plotted series are those of interest to the NBER Business Cycle Dating Committee. Of the six key items, nonfarm employment (blacks) and personal income are given greater weight after transfers.

{kind=link}

{kind=link}