Some people think we’re in a recession right now, Some Consider this in the past (we are currently in the second half of 2022).With the new weekly, monthly and quarterly data, do we still think these views are sound? [follow up on this post]?

First, let’s take a look at what the quarterly (GDP Q2 release) and new monthly consumption, income and GDP figures show:

figure 1: Nonfarm payrolls (dark blue), Bloomberg consensus as of September 1 (blue+), civilian employment (orange), industrial production (red), 2012 excluding transferred personal income (green), manufacturing and Trade sales Ch.2012$ (black), consumption of Ch.2012$ (light blue), monthly GDP of Ch.2012$ (pink), official GDP (blue bars), all log normalized to 2021M11 =0. The lilac shading indicates dates associated with the H1 hypothetical recession. Source: BLS, Federal Reserve, BEA, via FRED, IHS Markit (nee Macroeconomic Advisers) (published September 1, 2022), and author’s calculations.

Most of these series are now in St. Louis Fed NBER Turning Point Dashboard.

From these data, it is recalled that the NBER Business Cycle Measurement Committee (BCDC) is not highly reliant on quarterly GDP (as many revisions over time can eliminate or cause recessions – see This post about 2001), it does not appear that H1 is declining. (The NBER BCDC now places the most emphasis on employment and income.) The only indicators that are clearly trending downward are sales in the manufacturing and trade sectors, which partly reflect a shift in consumption from goods to services. Interestingly, monthly GDP (from IHS Markit, formerly a macroeconomic advisor) peaked in December 2021 and then declined in January, March and April (month/month). However, July was higher than April.

With one more revision to GDP in the second quarter, before the annual benchmark revision at the end of September, it is worth recognizing again that GDP (GDI) is better measured in real time using a combination of spending-side data (GDP) and income-side data. What would a 50-50 weight yield BEA reported as Gross Domestic Product (GDO), only available in the second GDP version.GDI-dependent series show a different output profile than GDP alone – as in Recent posts by Jacobs, Sarfarez, Sturm and van Norden.

We also know that while the agency survey data is a more precise measure than the household survey data, it is subject to revision, and preliminary benchmark data for March 2022 implies that employment growth is stronger than previously thought.this is in yesterday’s post. Putting together our knowledge of GDO and employment, this is the corresponding graph of Figure 1. .

figure 2: Nonfarm employment (dark blue), civilian employment (orange), industrial production (red), personal income excluding transfers in mid-2012 (green), manufacturing and trade sales in mid-2012 (black), consumption $2012 ( Light blue) and 2012 monthly GDP (pink), official GDP (blue bars), all log normalized to 2021M11=0. The lilac shading indicates dates associated with the H1 hypothetical recession. Source: BLS, Federal Reserve, BEA, via FRED, IHS Markit (nee Macroeconomic Advisers) (published September 1, 2022), and author’s calculations.

Second, let’s look at the weekly index. The Lewis-Mertens-Stock weekly economic index for the week ended 8/27 was just released today. Through this release, we have obtained the following high-frequency economic picture.

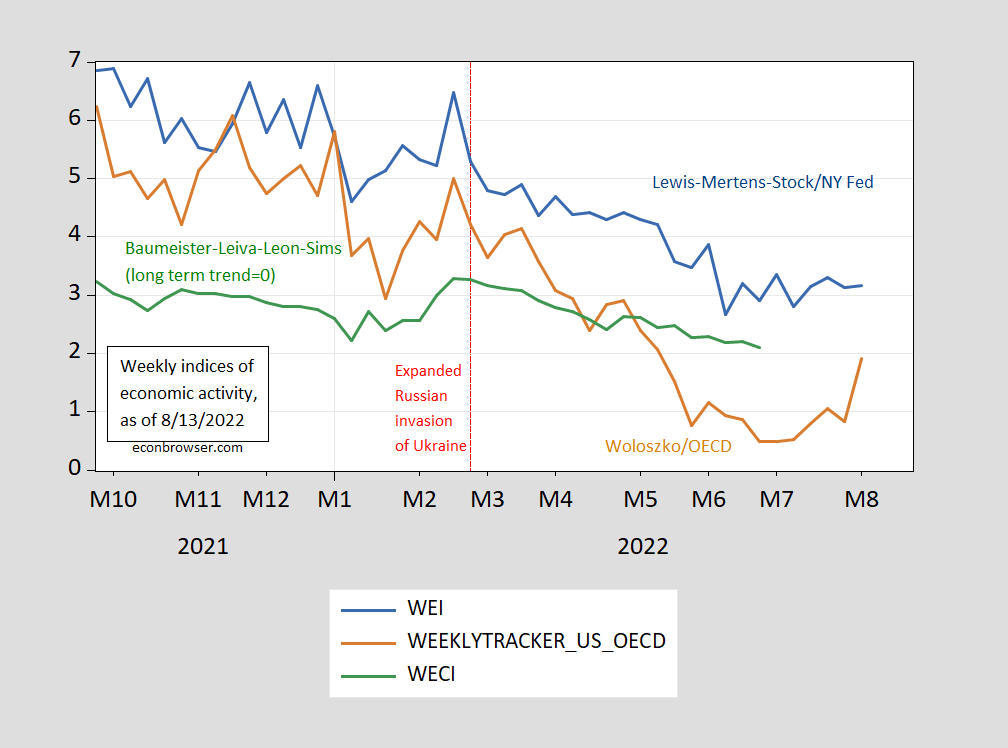

image 3: Lewis-Mertens-Stock Weekly Economic Index (blue), OECD Weekly Tracker (tan), Baumeister-Leiva-Leon-Sims US Weekly Economic Conditions Index plus 2% trend (green) Source: via NY Fed Fred, OECD, Wisioand the authors’ calculations.

If a reading of 2.5 persists throughout the quarter, a WEI reading of 2.5 for the week ended Aug. 27 could be interpreted as a quarterly growth rate of 2.5%. The OECD Weekly Tracker reading of 2.6 translates into an average annual growth rate of 2.6% through 8/20. Baumeister et al. The 2.1% reading for the week ended June 25 was interpreted as beating the long-term trend growth rate of 2.1%. The average growth rate of US GDP from 2000-19 was about 2%.

So I still don’t see a recession in the first half of 2022. As for the third quarter, today’s newly updated GDPNow was 2.6% (q/q SAAR), up from 1.4% previously; IHS Markit was up 1.4% and Goldman Sachs was up 1.1%.

{kind=link}

{kind=link}

{kind=link}