Today, we are honored to present the Pavel Skrzypchinski, Economist at the National Bank of Poland. The views expressed in this article are those of the author and should not be attributed to the National Bank of Poland.

In February, Goldman Sachs introduced the employment-worker gap (Briggs & Hatzius, 2022). This measure is defined as the difference between the total number of jobs (i.e. employment plus vacancies) and the number of workers (i.e. labor force). We present an updated interpretation of this gap and show a simple rule for using it to track business cycles.

Formally, we calculate the employment-worker gap for the month as , where is the household employment level, is the job vacancy level, and is the labor force level. Note that the gap calculated this way is scaled by the number of workers. Alternatively, this disparity relative to labor levels can be expressed, as shown in Figure 1. Note that job vacancies data are available from December 2000, which means that some proxies are needed to calculate the employment-worker gap for previous months to December 2000.To achieve this, use the Help-Wanted Index developed by Barnichon, 2010 (data available at this site). That is, for the months before December 2000, the index of need for help was used, while for the months after December 2000 and beyond, the job vacancy time series was used.

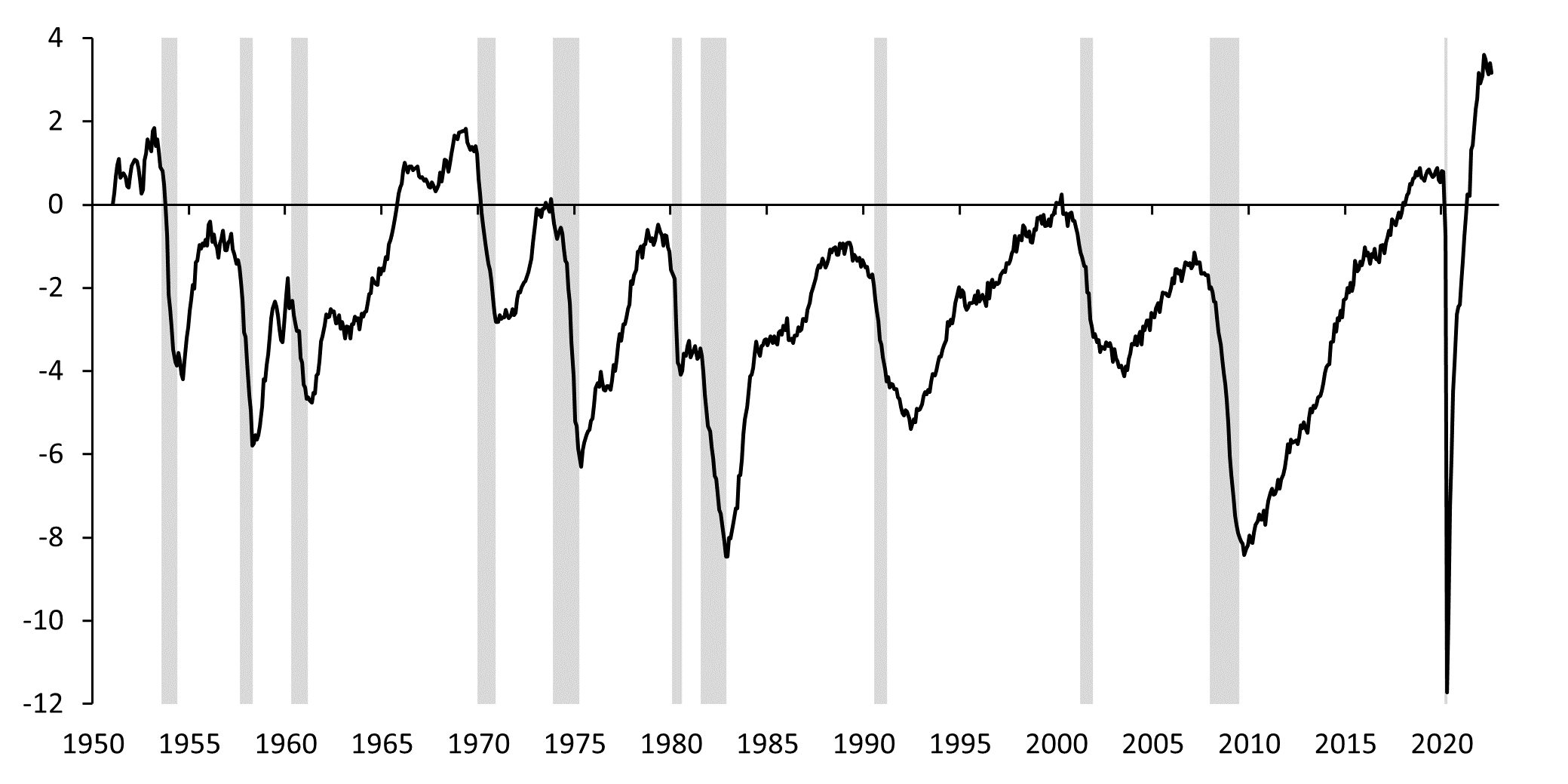

Figure 1. Job-worker gap (percentage)

Note: Calculations are based on employment published by BLS – August 2022, September 2, 2022, Job Openings and Labour Turnover – July 2022, August 30, 2022 and historical data from Barnichon’s Help-Wanted Index , 2010.

As of July 2022, the employment-worker gap was 5.6 million workers, meaning that employment and vacancies (total labor demand) outstripped labor (total labor supply) by 3.4%. Historically, this reading is close to the all-time high of 3.6% (5.9 million workers) reached in March 2022. While August job vacancies data were not yet available when the August Household Employment and Labor Force data was released, we made a job assumption that job openings were unchanged in August compared to July. Alternatively, weekly job posting data from Indeed can be used to bridge regression and forecast job openings for August. Assuming that job vacancies remain unchanged in August, combined with the August employment release (household employment rose by 442,000 square meters and labor force increased by 786,000 square meters), we find that the employment-worker gap declined by 3.2% (Figure 1) compared with The July level fell by 0.2 percentage points.

How big of a change from the current level of the employment-worker gap is enough to signal a recession? To answer this question, we propose the following measures. That is, we calculated the m/m change in the three-month moving average of the employment-worker gap, ie, relative to the previous twelve-month maximum. Smoothing allows us to obtain less volatile time series, which is more useful for tracking cycles. The resulting measure, called the Job-Worker Gap Business Cycle Indicator (JWGBCI), is measured in percentages and plotted in Figure 2. Note that the derivation of this indicator is similar to the derivation of the three-month moving average unemployment rate when calculating the so-called “Sam’s rule”. Together with the JWGBCI time series, we plot the decay thresholds derived from the Berge & Jordà, 2011 framework. That is, we compute a threshold of JWGBCI that maximizes utility for periods classified into recessions and expansions, so that the benefit of a hit is quantitatively equal to the cost of a miss. In other words, the recession threshold found using this method is -0.93 percentage points, the best level of JWGBCI to distinguish recession from expansion.

Figure 2. Employment-worker gap business cycle indicator (percentage points)

Note: Calculations are based on employment published by BLS – August 2022, September 2, 2022, Job Openings and Labour Turnover – July 2022, August 30, 2022 and historical data from Barnichon’s Help-Wanted Index , 2010.

We need to see the JWGBCI drop to -0.93 or below if we are to declare a recession. As of July 2022, the JWGBCI was -0.19 percentage points compared to -0.15 percentage points in June. Our conditional “guess” based on unchanged job vacancy levels in August is -0.22 percentage points. Thus, we conclude that while labor market conditions eased early in the third quarter, they remain tight and significantly away from recession-related levels. Note, for example, if we observe that the JWGBCI hit -0.93 in September, we would need to see the underlying employment-worker gap drop by 2.2 percentage points month-on-month to a level of 1% (ie, a gap of 1.6 million workers in August labor levels) . Except in the early days of the COVID-19 pandemic, there hasn’t been such a big change in a month, and that seems unlikely given current economic developments.

Overall, we suggest that current labor market conditions remain tight and would need to deteriorate significantly for the JWGBCI to signal a recession. A weaker JWGBCI index does not mean a recession is imminent unless the recession threshold is reached. Therefore, we interpret the future value of this indicator as being above the recession threshold consistent with a soft landing scenario.

refer to

Barnichon R., 2010, Building a comprehensive help-seeking index, Economics Letters109 (2010): 175-178.

Berge TJ, Jordà Ò, 2011, Evaluating recession and expansion classifications of economic activity, American Economic Journal: Macroeconomics3(2): 246-77.

Briggs J, Hatzius J. 2022, More Jobs Than Workers: A New Measure of Labor Market Tightness, US Economists, Goldman Sachs Economic Research.

This article is by Pavel Skrzypchinski.

{kind=link}

{kind=link}