Today, we are honored to present the Arthur Stara Bourdillon, economist at the Bank of France. The views expressed in this article are those of the author and should not be attributed to the Banque de France, the Eurosystem or the NBER.

in a New NBER WP, Nicolas Chatelet (Bank of France), Menzie Chinn (University of Wisconsin), and I use sector-by-sector stock variables in factor models to predict future economic activity in the United States.

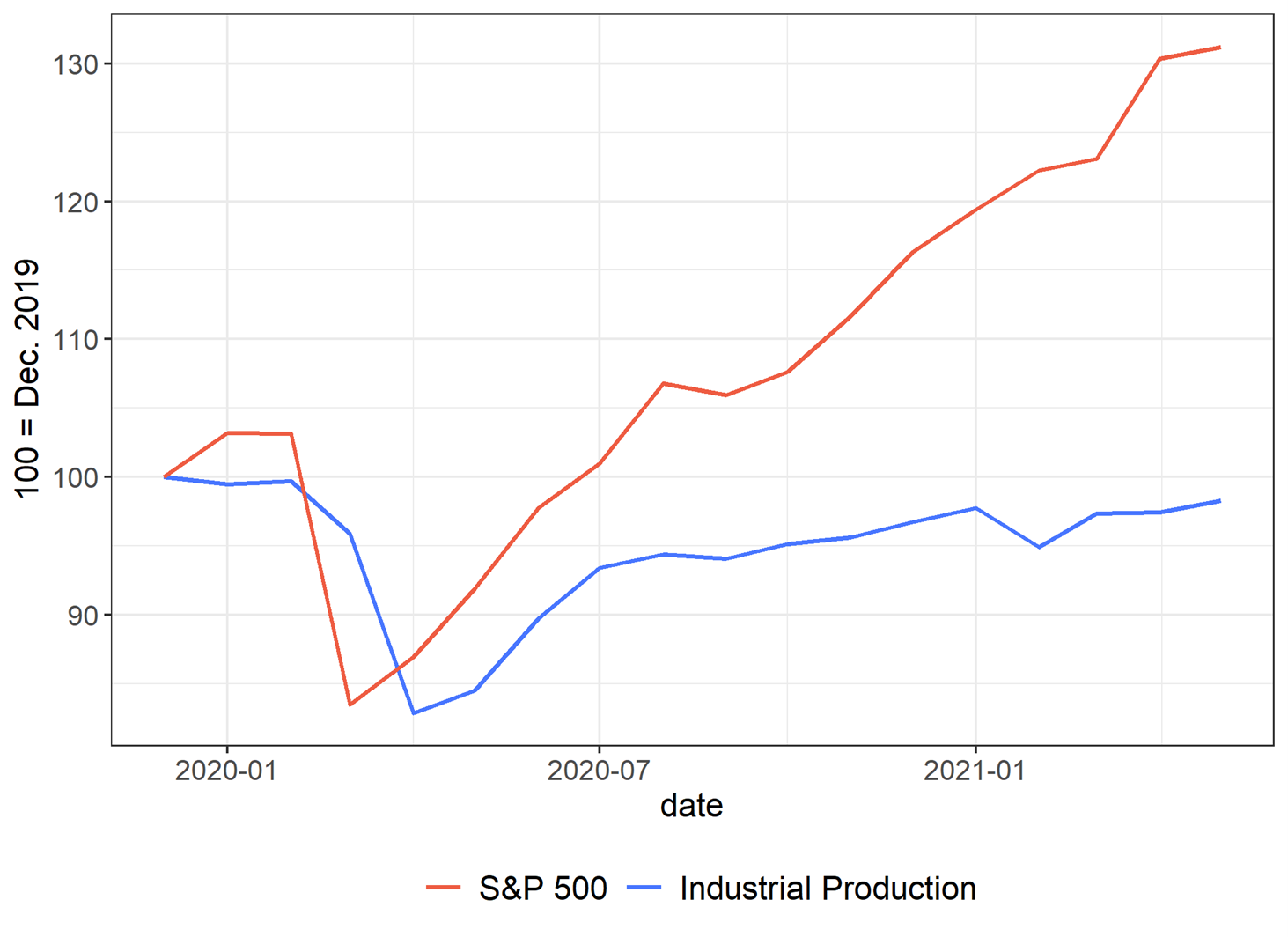

The idea for the project originated during the Covid crisis. At the time, the overall stock index was disconnected from actual macro variables. As a result, econometricians trying to predict economic activity (in this case, industrial production (IP) growth) and aggregate equity variables such as market dividend yields (DY) will get poor results (Figure 1).

Figure 1: S&P 500 and US Industrial Production Index (100 = December 2019)

notes: The graph represents the evolution of US industrial production and the S&P 500. Both indices were set to 100 in December 2019. Source: Federal Reserve Economic Data, Refinitiv Datastream.

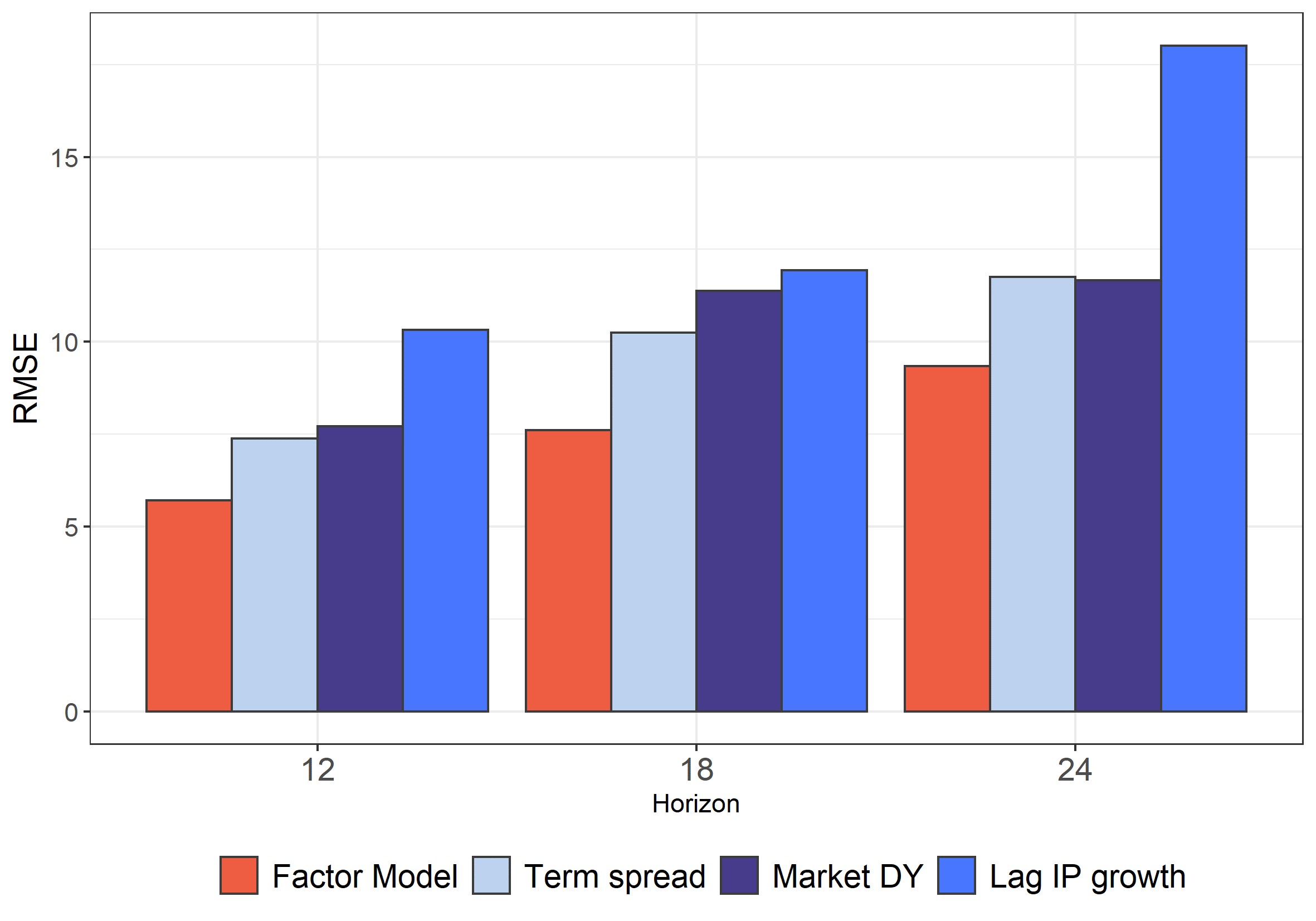

However, we show in the paper that in factor models, relying on departments When we compare the model’s performance to in-sample and out-of-sample classical benchmarks such as term spreads, IP growth lag, or market DY, instead of aggregating DY significantly improves our forecast accuracy (Figure 2).

Figure 2: Out-of-sample RMSE from different estimation models

notes: Out-of-sample RMSE for different models (factor models or univariate regression, depending on total DY, lagged IP growth, or term spread) are represented on the graph. The predictors were IP growth at 12, 18 and 24 months.

Why is this happening?

This is mainly because equity variables reflect not only expectations for future economic activity, but also changes in investor discount rates. Therefore, the regression of future IP growth on total DY is likely to be misspecified. In contrast, our sector-based DYs-based factor appears to have been removed from this “discount rate” component and more accurately reflects future economic activity than the original aggregate stock market variable.

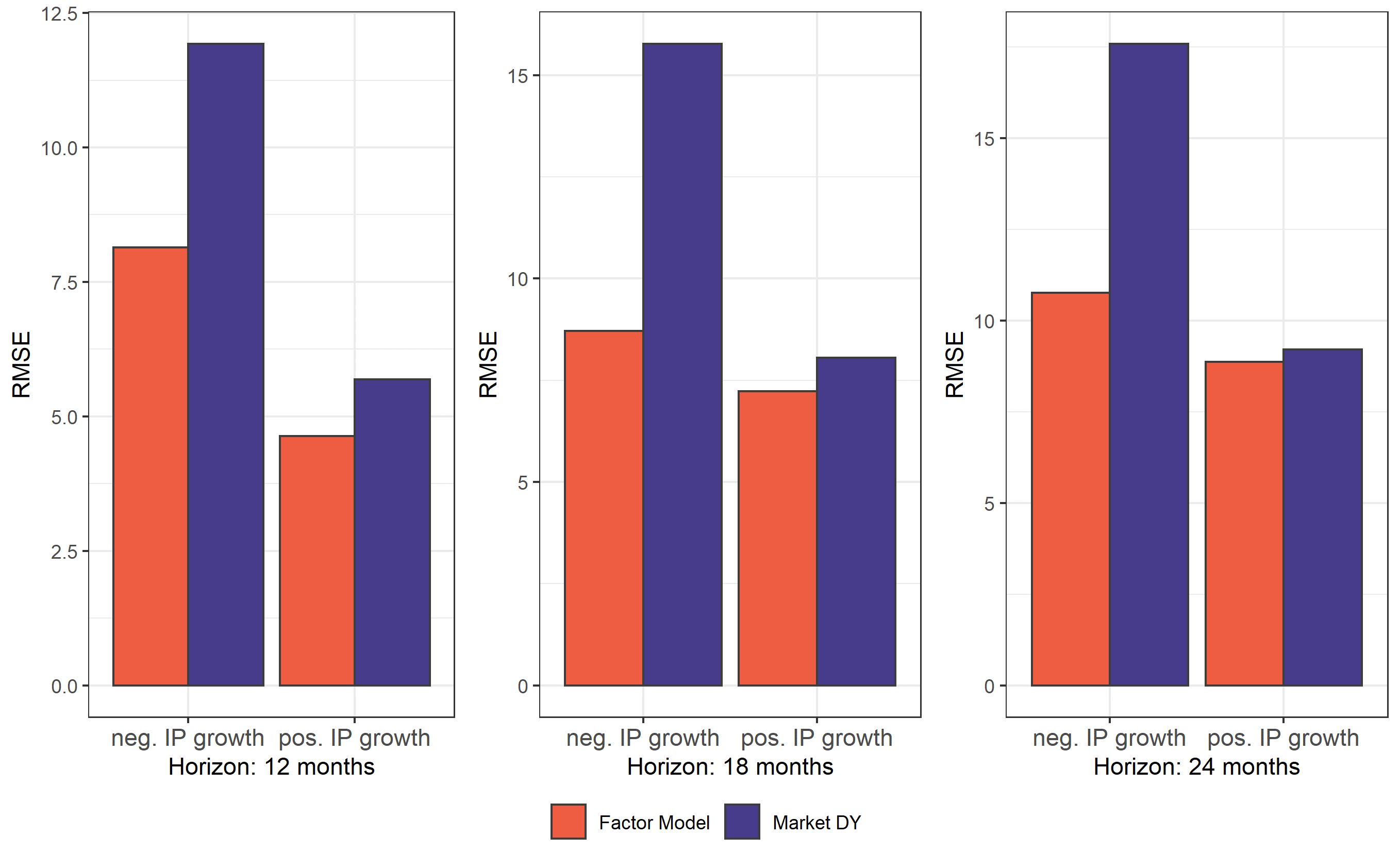

Intuitively, such forecast performance is especially strong when the discount rate is very volatile (recession, Covid-19 crisis), thereby masking the signal from the general stock index. Thus, the performance of our factor model appears to be mainly concentrated in periods when IP growth is already negative (Fig. 3).

Figure 3: Out-of-sample RMSE for different estimation models, by period

notes: The figure represents the out-of-sample RMSE of the factorial model and the univariate regression dependent on the aggregated DY. Note that here we break down our estimates based on the date the forecast was made. In other words, if we consider a 12-month forecast horizon here, the period of “negative IP growth” refers to forecasts made when annual IP growth is negative (rather than 12 months prior to the contraction in economic activity) predict). The predictors were IP growth at 12, 18 and 24 months.

Where are we now in terms of recession risk? As of July 2022, the signals from different financial variables appear to be quite mixed. Rolling-window regression estimates based on term spreads or market DYs project IP growth rates of +1.1% and +2.7% over the next 12 months (annual), respectively. In contrast, our factor model is more pessimistic and predicts negative IP growth next year: -2.2%.

This article is by Arthur Stara-Bourdiron.

{kind=link}

{kind=link}