Today, we introduce an article by David Papel and Luke Sandra ProdinProfessor of Economics and Associate Professor of Teaching at the University of Houston.

The Federal Open Market Committee (FOMC or Committee) raised its target range for the federal funds rate (FFR) by 3/4% (75 basis points) to 3.0% to 3.25% from 2.25% to 2.5% at its meeting last week, and A range is forecast between 4.25% and 4.5% by the end of 2022. Two years after the 0.0% to 0.25% effective lower bound (ELB) was raised by 25 basis points at the March 2022 meeting, the committee has now implemented one 50 and three 75 basis point rate hikes.

The Fed is widely believed to be “behind the curve” by not raising rates in 2021 when inflation rises, forcing it to “catch up” in 2022, causing dramatic rate hikes and market volatility. Why is this happening? The “we don’t know” explanation is that the Fed didn’t forecast inflation to rise that much by 2021, and they would raise rates sooner, if at all. The “they should know” explanation is that the Fed should know that inflation won’t be temporary and will raise rates sooner.

Most discussions of the Fed behind the curve hinge on a subjective analysis of when it should appreciate from the ELB. We propose different explanations. If the Fed follows its own policy rules, it will start raising rates in the third quarter of 2021 rather than the first quarter of 2022. Implementing the same total rate increase takes about twice as many meetings, and each individual rate increase only takes about half as much. Since the policy rule uses inflation and unemployment data rather than forecasts, it renders “we don’t know” explanations irrelevant, and “they should know” explanations unnecessary.

In an earlier paper, “Policy Rules and Forward Guidance After the Covid-19 Recession,” and the Econbrowser post, “Fed trails the curve by not following its own policy rules,” using data from the September 2020-June 2022 Summary of Economic Projections (SEP) to compare policy rule provisions with actual FFR and FOMC projections. This provides a precise definition of “behind the curve,” That is, the difference between the FFR specified by the policy rule and the actual FFR.

This Taylor (1993) The rules for the unemployment gap are as follows,

where is the rule-mandated level of the short-term federal funds rate, is the inflation rate, is the 2% inflation target level, is the 4% long-term unemployment rate, is the current unemployment rate, and is the current ½% neutral real rate of the SEP. We use real-time inflation and unemployment data available at the FOMC meeting.

Yellen (2012) The balancing method rule is analyzed in which the inflation gap coefficient is 0.5 but the unemployment gap coefficient is raised to 2.0.

![]()

After the Great Recession, the Balanced Approach rule received considerable attention and became the standard policy rule used by the Federal Reserve.

The Federal Open Market Committee passed a far-reaching Revised Statement Regarding the long-term goals and monetary policy strategy for August 2020. The framework contains two major changes from the original 2012 statement.First, policy decisions will try to mitigate insufficiencyinstead of deviation, from its highest level of employment. Second, the FOMC will implement a Flexible Average Inflation Targeting (FAIT) in which “after a period of persistently sub-2% inflation, appropriate monetary policy is likely to achieve inflation moderately above 2% for a period of time.”

We analyze Fed policy using the inertial version of the Balanced Approach (Shortage) rule introduced in February 2021 monetary policy report (MPR) in response to the revised statement. The rule alleviates employment shortages rather than biases by having FFRs respond to unemployment only when unemployment exceeds long-term unemployment,

![]()

If the unemployment rate exceeds the long-term unemployment rate, the FFR rules are the same as the balance method rules. If the unemployment rate is lower than the long-term unemployment rate, the FOMC will not raise the FFR simply because the unemployment rate is low.

While much of the attention following the revised statement has been on FAIT, the sharp rise in inflation in 2021 and 2022 makes that part irrelevant. However, with unemployment below 4.0%, insufficiency instead of deviation Employment remains an important aspect of policy.

These rules are non-inertial as the FFR is fully adjusted whenever the target FFR changes. This is inconsistent with the FOMC’s practice of smoothing rate hikes when inflation rises.We also specify an inertial version of the balance method (deficiency) rule, based on Clarida, Gary and Gertler (1999),

![]()

where is the degree of inertia and is the target level of the federal funds rate specified by equation (3).we set to Bernanke, Keeley and Roberts (2019). is equal to the ratio specified by the rule if positive, zero if the specified ratio is negative.

At its September 2020 meeting, the committee approved results-based Forward Guidance, saying it expects to maintain the ELB’s FFR target range “until labor market conditions reach levels consistent with the Committee’s assessment of full employment and inflation rises to 2% and is on track to moderately exceed 2% at some point in time.” ” The key word is “and”. While the Fed’s inflation target was achieved in December 2021, the ELB did not see a boost until March 2022 when its maximum employment target was achieved.

Had the Fed followed policy rules using inflation and unemployment data from the FOMC’s quarterly SEP rather than the FOMC’s forward guidance, they could have avoided the pattern of lagging behind the curve, turning and getting back on track, characteristic of Fed policy in 2021 and 2022 year. The rules mandate a rate hike from the ELB in Q2 2021 or Q3 2021, with a much smoother hike path through the end of 2022 than the one adopted/predicted by the FOMC.

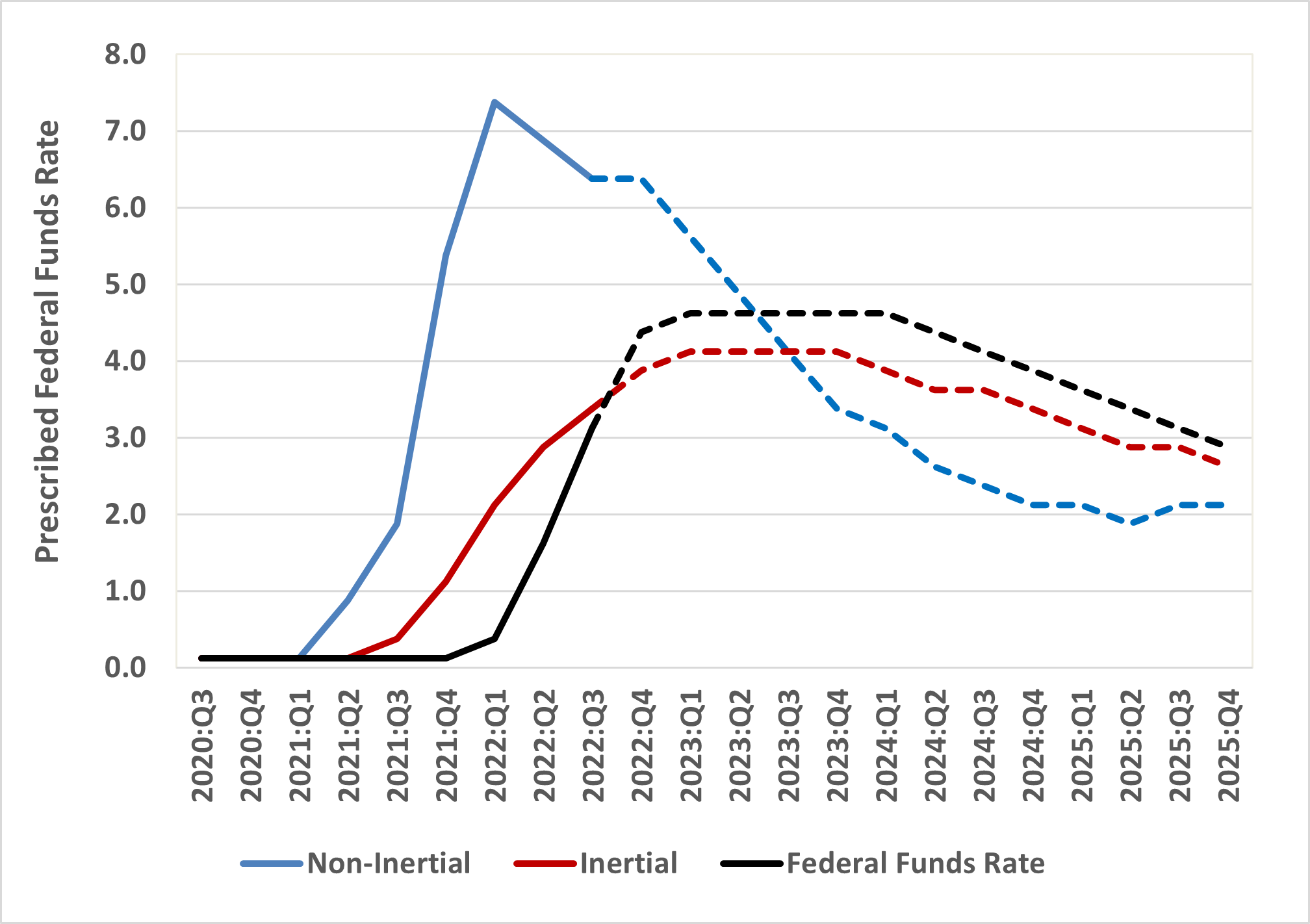

Figure 1 depicts the actual FFR from September 2020 to September 2022 and the projected FFR from December 2022 to December 2024 starting with the September 2022 SEP. After exiting from ELB to 0.375 in March 2022, FFR rose to 1.625 in June 2022 and 3.125 in September 2022, and is expected to rise further to 4.375 in December 2022 and 4.625 in March 2023, Then it begins to decline in June 2024.

figure 1: Balanced Approach (Deficiency) Rules: Non-Inertial and Inertial

The figure also illustrates the prescribed FFR with non-inertial balance method (deficiency) rules. ELB’s stated exit time is the second quarter of 2021, three-quarters earlier than the actual exit time. After rising from ELB to 0.875 in Q2 2021, the prescribed FFR increases sharply to 7.375 in Q1 2022 before starting to decline in Q2 2022. With six meetings between June 2021 and March 2022, each of which mandated FFR hikes of more than 100 basis points, these mandated rate hikes are completely unrealistic policy guidance.

Figure 1 also shows the prescribed FFR with the inertia balance method (deficiency) rule. The ELB’s stated exit time is the third quarter of 2021, which is one quarter of the non-inertial rule stated exit time and the first two quarters of the actual exit time. After rising from the ELB to 0.375 in Q3 2021, the stated FFR slowly increases to 3.375 in Q3 2022, just 25 basis points above the actual FFR.

The Fed’s turn can be seen by comparing the prescription of the Balanced Approach (Shortage) rule to FFR as of September 2022 and projected FFR thereafter. The FFR is 175 basis points higher than the stated FFR when it takes off from the ELB in March 2022. With the subsequent series of rate hikes, the FFR is now just 25 basis points above the stated FFR. However, from December 2022, the FFR is expected to rise to 50 basis points above the mandated FFR and, in a few cases, remain 50 basis points above the mandated FFR by June 2025.

Policy rules provide a framework for monetary policy evaluation. Using the rule that best matches the Fed’s goals, the Inertial Balance Approach (Shortage) rule, the Fed was just behind the curve in September 2021 and just got back on track. Instead of staying on track, the Fed now forecasts that the FFR will be above the policy rules for the next three years. Has the Fed gone too far in shifting its focus entirely from unemployment to inflation? While it’s clearly too early to answer that question, following its own policy rules starting in 2021 will allow the Fed to balance the two parts of its dual mandate and provide predictability for its future actions.

This article is by David Papel and Luke Sandra Prodin.

{kind=link}

{kind=link}