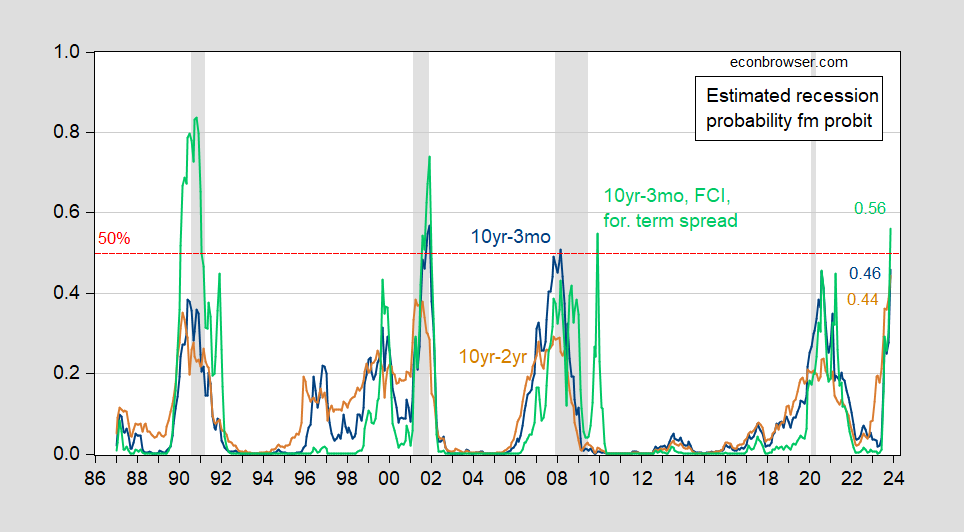

Yesterday’s Bloomberg article “Fed staff sees 50-50 chance of recession” Prompted me to examine the impact of the latest reading on term spreads. Figure 1 depicts recession probabilities estimated as of November 23 using a simple probability model based on 10-year to 3-month and 10-year to 2-year spreads.

figure 1: 10-3M Term Spread (blue), 10-Year-2Y Term Spread (tan), FCI Widened 10-Year-3M Term Spread, Foreign Term Spread (green) Recession Forecast probability. All models estimated to be over 1986M01-2022M11. Dates of peak-to-trough recessions as defined by NBER are shaded in gray. A dashed red line with a probability of 50%. Source: Author’s calculations, National Bureau of Economic Research.

While neither the 10yr-3mo nor the 10yr-2yr model crossed the 50% threshold, they were close enough to the 50-50 reading.

working Ahmed and Chinn (2022), indicating that foreign term spreads and financial conditions indices have additional predictive power for US recessions (see Table A.1). I add the 10-year-3-month spread to the average of the Germany-euro area/UK/Japan 10-year-3-month spread and the country financial conditions index to obtain the estimated recession probabilities shown in the green line in Figure 1. In November 2023 it will be 56%.

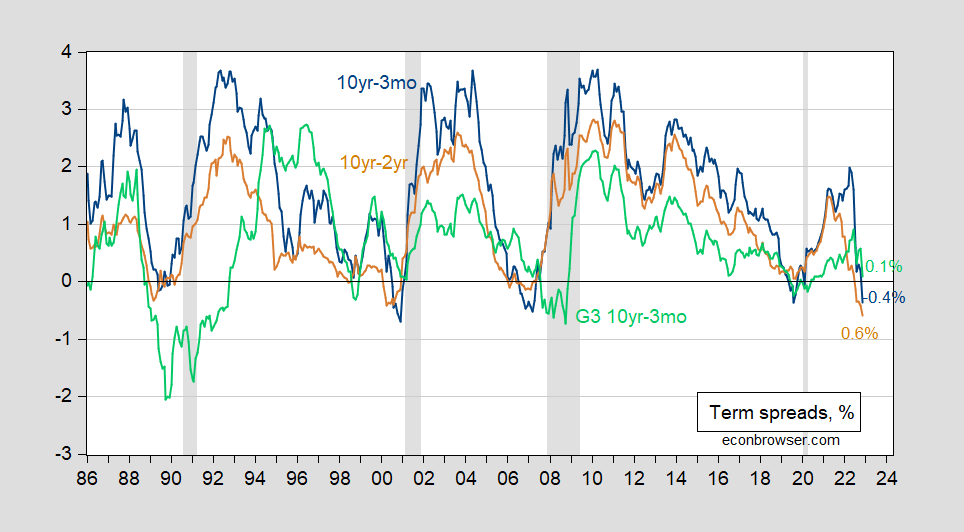

All of these estimates are based on the following term spreads:

figure 2: US Treasury 10y-3m term spread (blue), 10y-2yr (tan) and G3 Germany/UK/Japan 10y-3m (green), all expressed as a percentage. Dates of peak-to-trough recessions as defined by NBER are shaded in gray. Source: Ministry of Finance via FRED, OECD key economic indicators, NBER and author’s calculations.

{kind=link}

{kind=link}