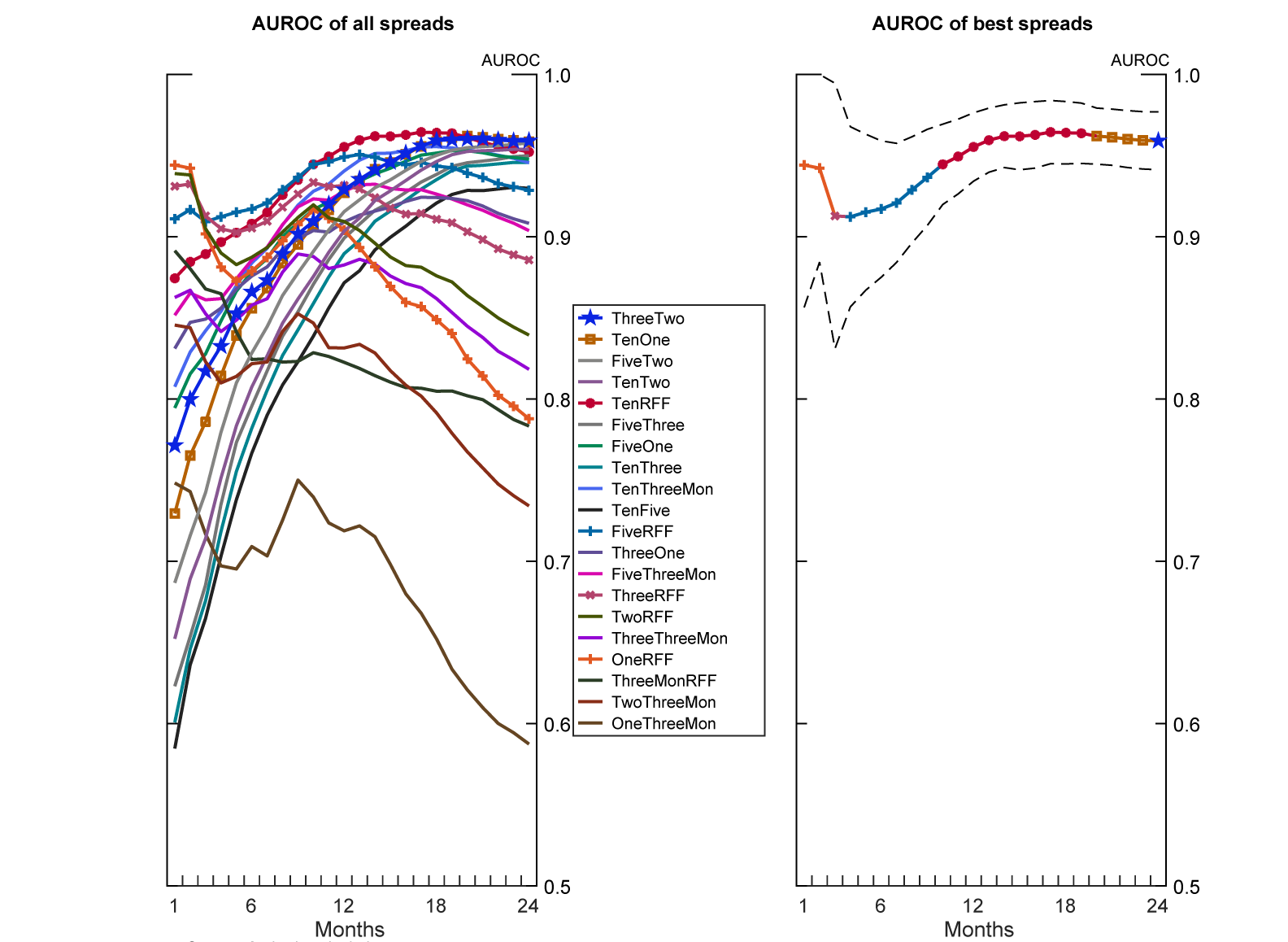

In 2019, Fed economists david miller A comprehensive assessment of the predictive power of term spreads for recessions (No single best predictor of recession). For the period 1984-2018, he found the following:

Figure 2: AUROC sample 1984 – 2018 from Miller (2019).

See this article for a discussion of AUROC (Area Under the Receiver Operating Characteristic Curve) Jim H.

How did those spreads look as of Friday?

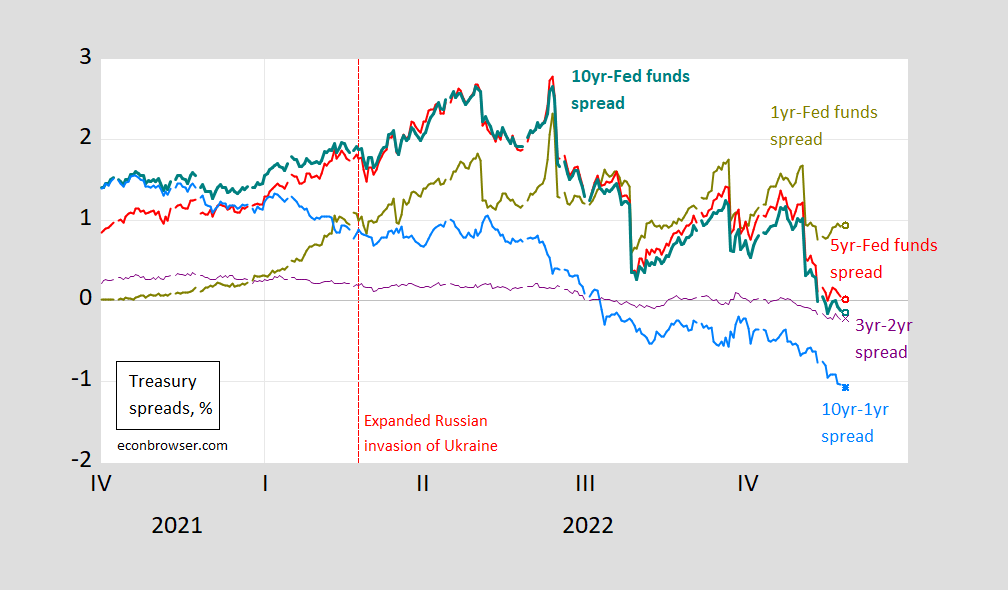

figure 1: 1Y Fed Funds Spread (Yellow Green), 5Y Fed Funds Spread (Red), 10Y Fed Funds Spread (Dark Teal), 10Y-1Y (Sky Blue), and 3Y-2 Years (purple), all are percentages. The dashed red line indicates Russia’s expanded invasion of Ukraine. Source: Treasury via FRED, and authors’ calculations.

The 1-year fed funds spread (1-2 months) has not turned negative, nor has the 5-year fed funds spread (4-9 months), although it has come close. The 10-year fed funds spread (10-19 months) did close in negative territory on November 10th, suggesting a recession will occur sometime between September 2023 and August 2024. Year 10 to Year 1 is also negative on July 12, so 20 to 23 months ahead (February 2024 to May 2024).

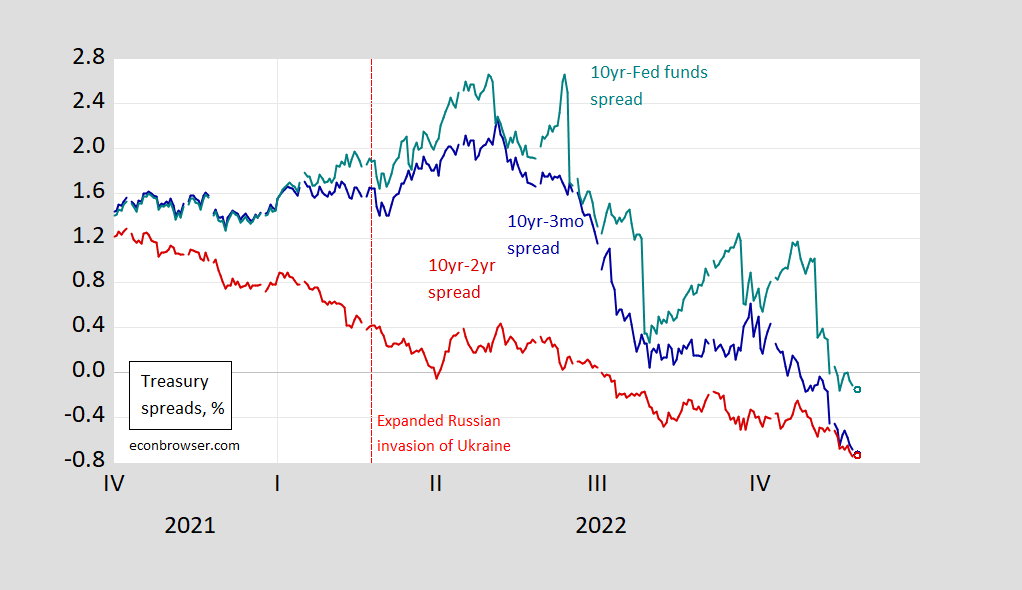

By the way, here are the common spreads I show:

figure 2: 10-Year-Federal Funds (turquoise), 10-Year-March (blue), and 10-Year-2 (dark red), all in percentages. The dashed red line indicates Russia’s expanded invasion of Ukraine. Source: Treasury via FRED, and authors’ calculations.

Note that AUROC is calculated for simple term spreads, not for models that include other variables such as foreign term spreads, financial conditions indices, or stock prices (as described in this paper) postal).

{kind=link}

{kind=link}