Today we are fortunate to present an article by Michael Rubasek (SGH Warsaw School of Economics), Joshua Beckman (Fern Universität Hagen and Kiel Institute for the World Economy) michelle kazoz (ECB), and maleic acid (SGH Warsaw School of Economics). The views expressed in this article are those of the authors and not necessarily those of the institution to which they are affiliated.

We have published a new ECB working paper (No. 2731) entitled “Improving spreads through equilibrium exchange rate estimates’. The title suggests that it is possible to improve the performance of forex trading strategies, rather than assuming random movements in exchange rates.

The generally held view in economics is that it is nearly impossible to predict the future movement of exchange rates (Rossi, 2013). Two pieces of evidence are often presented in support of this argument. The first comes from the (time-series) foreign exchange literature on currency forecasting, arguing that it is preferable to assume exchange rates follow a “random walk” and make constant forecasts than to forecast exchange rates using a macro model. The second prevails in the Forex literature on currency portfolios, pointing to the success of an investment strategy known as the “carry trade” that involves borrowing in a low-yielding currency and investing in a high-yielding currency (Lustig et al., year 2011; Koijen et al., 2018). The profitability of the carry trade contradicts unsecured interest rate parity and implicitly assumes that exchange rates behave as random walks. For decades, these two branches of the FX literature have been explored in parallel, the first aimed at forecast accuracy and the second at portfolio profitability to outperform their respective benchmarks, random walks and arbitrage trading strategies. In both cases, the approach is the same in spirit, that is, to build a model that attempts to restore, theoretically or empirically, the link between exchange rates and economic fundamentals (Menhof et al., 2017; Zhang et al., 2019; Colacito et al., 2020).

The assumption of stochastic exchange rates is difficult to accept because it is inconsistent with economic theory. On the Econbrowser blog “Currency Forecast on a Napkin” We argue that the process of gradual exchange rate convergence towards purchasing power parity (PPP) tends to outperform random walks in exchange rate forecasting. In the article “Reliability of Equilibrium Exchange Rate Models: A Forecasting PerspectiveWe generalize this result, showing that it also holds for equilibrium measures based on behavioral equilibrium exchange rate (BEER) models (rather than just purchasing power parity). This predictive power contradicts the first evidence supporting the random walk hypothesis. In this blog, we discuss a second piece of evidence in support of this hypothesis, namely the success of carry trade strategies and whether their past strong performance is evidence in support of the random walk hypothesis.

To understand whether the predictability of (time-series) exchange rates can be exploited to design competitive currency portfolios, we collect quarterly data on G10 currencies from 1975 to 2020. We then compute two sets of equilibrium exchange rate estimates using the PPP and BEER models and validate our claim that there is some time-series predictability in at least one quarter of the time horizon over this time horizon. We ultimately employ tools and methods from the foreign exchange trading literature to demonstrate that investors can use evidence of exchange rate misalignment to build foreign exchange portfolios with competitive risk-reward characteristics.

To this end, we evaluated:

- Three benchmark strategies: Momentum (M), Value (V) and Arbitrage (C);

- Strategies based on foreign exchange imbalances only (EqER);

- Strategies based on the assumption that the exchange rate gradually returns to equilibrium – assuming that half of the adjustments take place over a fixed period of time, eg 3 (HL3) or 10 (HL10).

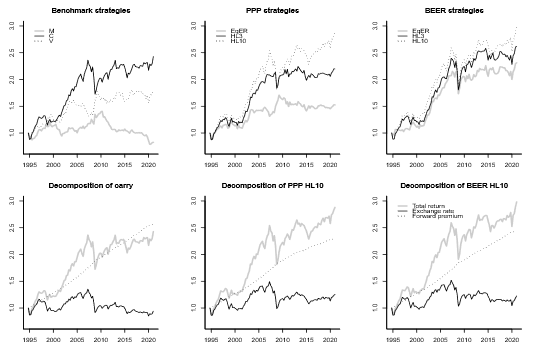

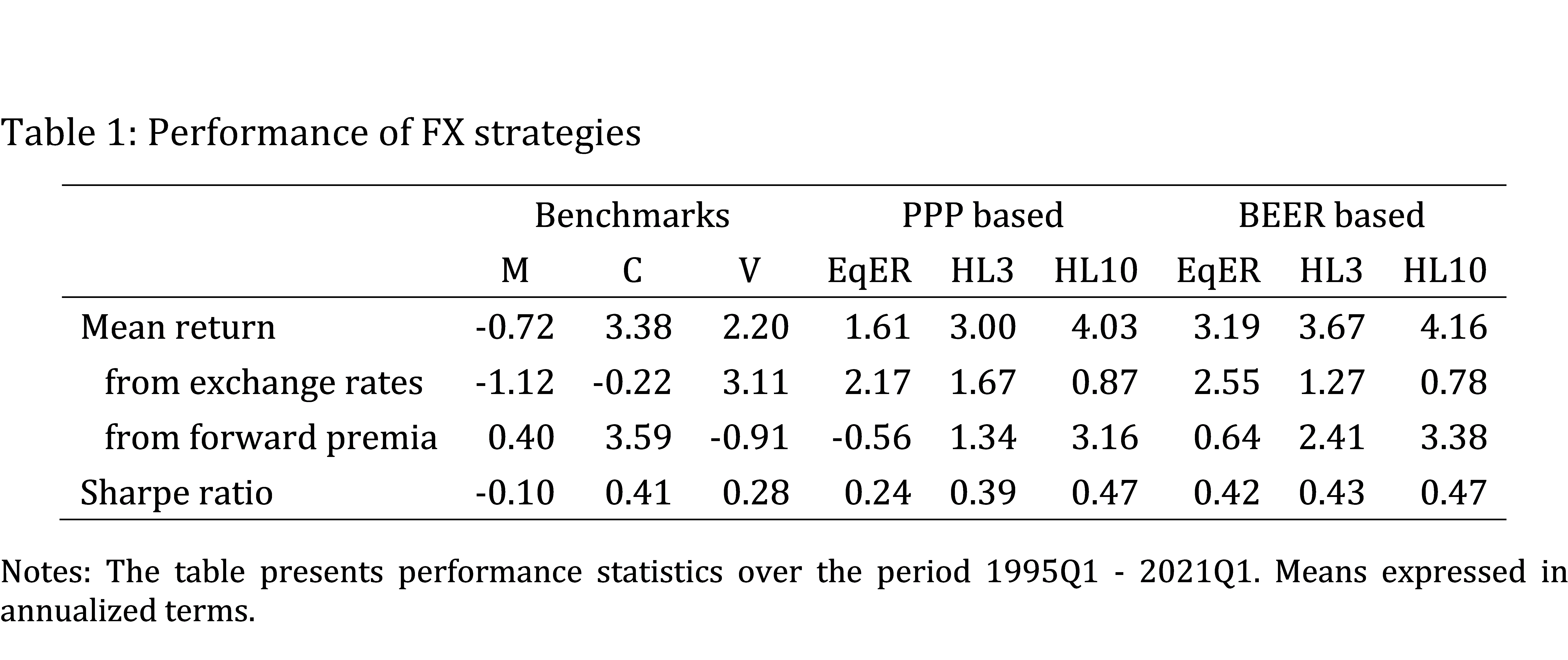

Table 1 and Figure 1 show the key performance statistics of the above strategies and their cumulative returns, respectively. The results show that on the horizon from 1975 to 2020, strategies based on foreign exchange dislocation (EqER) could have been profitable, as indicated by mean returns and Sharpe ratios (see rows 1 and 4 in Table 1). This is consistent with the idea that evidence of undervaluation or overvaluation can be exploited if the pool of money is large enough. However, they do not perform as well as pure arbitrage trading strategies. We interpret this result as consistent with evidence that exchange rates initially adjust very slowly to their equilibrium—therefore the predictable component is not large enough to outweigh the gains from knowing with certainty the general allocation of interest rate differentials across countries.

The lesson one can learn is that it is better to rely on an alternative assumption that exchange rates adjust only gradually towards equilibrium. We show that by exploiting both the time-series predictability of the exchange rate and extracting the forward premium (see rows 2 and 3 in Table 1), the two HL strategies are indeed highly competitive against other benchmarks . Of these, the HL10 strategy produces higher expected returns and Sharpe ratios than the naive arbitrage strategy in the case of the PPP and BEER models. This result is robust to a wide range of half-lives, showing how departures from the random walk assumption can help facilitate spread-based forex trading strategies. The key requirement is to assume a sufficiently slow adjustment process. Beyond performance issues, HL strategies profoundly change the nature of expected returns, since a significant component now comes from the modeler’s ability to extract spot rate predictability (Table 1 and bottom panel of Figure 1).

figure 1: Forex Portfolio Returns

notes: The graph above shows the cumulative return based on EqER and the benchmark strategy. The bottom panel decomposes excess returns into spot rate predictability and forward premiums.

The main message of this blog is not to question the evidence that carry trades have performed well in recent decades. In contrast, the HL strategy is no different in practice from the carry trade strategy. What we are arguing is that the success of an arbitrage trading strategy automatically means that the exchange rate is random. From the perspective of economic theory and portfolio investors, a gradual exchange rate adjustment to remove existing misalignments seems to be a preferable assumption.

refer to

Cheung, Y.-W., Chinn, MD, Pascual, AG, and Zhang, Y. (2019). Exchange rate prediction redux: new models, new data, new currencies. International Journal of Money and Finance, 95:332–336.

Colacito, R., Riddiough, SJ, and Sarno, L. (2020). Business cycles and monetary returns. Journal of Financial Economics, 137(3):659–678.

Koijen, RS, Moskowitz, TJ, Pedersen, LH and Vrugt, EB (2018). carry. Journal of Financial Economics, 127(2):197–225.

Lustig, H., Roussanov, N., and Verdelhan, A. (2011). Common risk factors in currency markets. Review of Financial Studies, 24(11):3731–3777.

Menkhoff, L., Sarno, L., Schmeling, M., and Schrimpf, A. (2017). monetary value. Review of Financial Studies, 30(2):416–441.

Rossi, B. (2013). Predictability of exchange rates. Journal of Economic Literature, 51(4):1063–1119.

this post was written Michael Rubasek, Joshua Beckman, michelle kazoz with maleic acid.

{kind=link}

{kind=link}