Today, we are pleased to introduce to you the Dimitrios Canellis (Westfälische Wilhelms-Universität Müun) and Pierre Ciclos(Wilfrid Laurier University and CAMA and Australian National University). The views expressed here are their own and do not reflect the official views of the institutions to which the authors are affiliated.

An obvious source of unscripted information is the human voice, since voice does not necessarily convey the same information as text. Gorodnichenko et al. (2020) provide evidence of how the verbal sentiment of Federal Reserve Board chairs can have a significant impact on stock prices in the days following an FOMC press conference. Curti and Kazinnik (2021) and complementary studies by Alexopoulos et al. (2022) Estimating the real-time impact of Federal Reserve chair facial expressions on stock prices.

in our Paper, we estimate the impact of verbal sentiment and language in the question-and-answer segment of the ECB press conference during Mario Draghi’s presidency on the yield curves and spreads to German yields in the four major euro area economies. influences. We conduct an event study and construct a new dataset consisting of timely simultaneous audio and text data of press conferences from May 2012 to October 2019.

One challenge was that Draghi answered several questions in succession on completely different topics. We therefore exploit an interesting feature of the ECB press conference transcript. ECB staff identify points of contact and structure them in writing. Following this structure, we adjust the audio data for each answer and establish synchronization between speech and text. We then implement the fully convolutional neural network (FCN) of García-Ordás et al. (2021), which has special properties for handling audio files of non-fixed length.

To measure the content of non-scripting languages used in press conferences, we implemented Fin-BERT. This large language neural network model can analyze texts related to economics and finance, surpassing word counting methods of dictionary methods. We use data from France, Germany, Italy and Spain.

To quantify sentiment and generate numerical variables for our event regression estimates, we used methods developed in SER, a subfield of machine learning (Pérez-Espinosa et al., 2022). More recently, economists have started using the SER to analyze the verbal sentiment of the Fed chair to estimate the impact on asset prices (Gorodnichenko et al. (2020); Alexopoulos et al. (2022)).

In contrast to Gorodnichenko et al. (2020), we utilize a fully convolutional neural network (FCN) based on García-Ordás et al. (2021), which yielded higher out-of-sample accuracy and a clear advantage when measuring sentiment in question answering sessions, which are characterized by highly variable answer lengths. These emotions are Neutral, Calm, Happy, Sad, Angry and Surprised, and they come in two different intensities (Normal Emotional Intensity and Strong Emotional Intensity).

Voice sentiment was found to be persistently negative during the European Sovereign Debt Crisis (ESDC). An exception was the press conference on 2 August 2012, the most positive moment during the crisis, observed just days after Draghi’s famous “whatever it takes” speech, which is considered to be the period of ESDC A turning point. After the end of ESDC, before turning more negative again for most of 2014, a temporary increase in verbal sentiment could be observed, with the ECB Governing Council facing challenges due to the low inflation and growth environment, financial fragilities and heightened risks Unanchored inflation expectations for one year. The launch of the Asset Purchase Program (APP) was accompanied by more positive rhetorical sentiment, possibly due to Draghi’s success in pursuing an unconventional monetary policy despite controversy surrounding the policy within the Governing Council (Brunnermeier et al., 2016). The decline in average verbal sentiment was seen again in 2018, a period of mounting policy challenges and reaching new lows when the ECB restarted its quantitative easing program, just months after the Governing Council began trying to exit.

To illustrate this, the slide below is an example of positive, neutral and negative sentiment delivered by Draghi based on our methodology (all of which could have occurred in the same press conference). Readers were asked to determine whether they agreed with the sentiments displayed by Draghi, as identified by the methodology used (answers are provided in the captions below the slides). Actual illustrations are also identified for comparison.

notes: The first audio clip is neutral, starting on April 27, 2017; the second is a positive value starting at 1Yingshi July 4, 2023 press conference on forward guidance; last clip, negative, from April 15, 2015, when an activist jumped on a table.

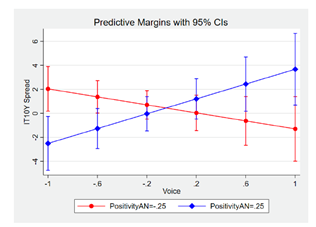

Among the hypotheses tested is whether positive sentiment increases yields, while negative sentiment lowers them. We estimate that changes in the framing of press conferences have a significantly positive effect on spreads, i.e., positive changes in statements lead to wider spreads, while negative rewrites lead to lower spreads. Marginal plots measure the impact of vocal emotion at a given level of positivity of the language used in a question-and-answer session. This allows us to identify more subtle effects on yield spreads than regressions alone provide. The chart below shows the marginal effect of voice sentiment on 10-year Italian bond spreads.

notes: These plots visualize the marginal effect of a change in Voice on Italian 10-year government bond spreads for a given level of PositivityAN at time t, also at time t. We report spread changes in basis points (ie in the range -25 to +25).

The interplay of vocal emotion and language in a question-and-answer session has a significant and asymmetric impact on the spread of Italian bonds. The combination of negative vocal sentiment and negative language resulted in increased transmission. Ten-year Italian bonds, for example, reacted differently, depending on the degree to which vocal and verbal signals collided. Positive-positive and negative-negative combinations of sound and language lead to increased transmission, while more conflicting signals decrease transmission. In the case of Germany (not shown), unscripted communication had a positive effect on earnings. However, this effect is limited to the short end of the yield curve and is asymmetric in terms of vocal sentiment. More positive communication pointed to a rise in German bond yields. The paper also discusses the impact of Draghi’s sentiment and the content of the ECB press conference on French and Spanish bond yields.

One bottom line of this paper is to remind people that communication is more than words. Future research should consider how financial markets perceive and process vocal cues during crises such as the COVID-19 pandemic or rising inflation from 2021 onwards, and how central bankers’ sentiment affects asset prices at times of heightened economic and geopolitical uncertainty.

The paper is available from https://cama.crawford.anu.edu.au/publication/cama-working-paper-series/20867/emotion-euro-area-monetary-policy-communication-and-bond.

refer to

Alexopoulos, M., Han, X., Kryvtsov, O., Zhang, X., 2022. More Than Words: Fed Chair Communications in Congressional Testimony. work documents.

Brunnermeier, MK, James, H., Landau, JP, 2016. The euro and the battle of ideas. Princeton University Press.

Curti, F., Kazinnik, S., 2021. Let’s face it: quantifying the impact of non-verbal communication in FOMC press conferences. Draft working paper: March 18, 2022.

García-Ord as, MT, Alaiz-Moretón, H., Benítez-Andrades, JA, García-Rodríguez, I., García-Olalla, O., Benavides, C., 2021. Sentiment analysis in non-fixed-length audio using Fully Convolutional Neural Network. Biomedical Signal Processing and Control 69.

Gorodnichenko, Y., Pham, T., Talavera, O., 2020. The voice of monetary policy. Draft Working Paper: June 14, 2022, forthcoming in American Economic Review.

Pérez-Espinosa, H., Zatarain-Cabada, R., Barrón-Estrada, ML, 2022. Emotion recognition: from speech and facial expressions. Chapter 15. Posted by: Torres-García, Alejandro A. and Reyes-García, Carlos 1 Villasenor-Pineda, Luis and Mendoza-Montoya, Omar (Ebs.): Using Computational Learning and Intelligence for Biosignal Processing and Classification. Elsevier.

This article was sponsored by Dimitrios Canellis and Pierre Ciclos.

{kind=link}

{kind=link}