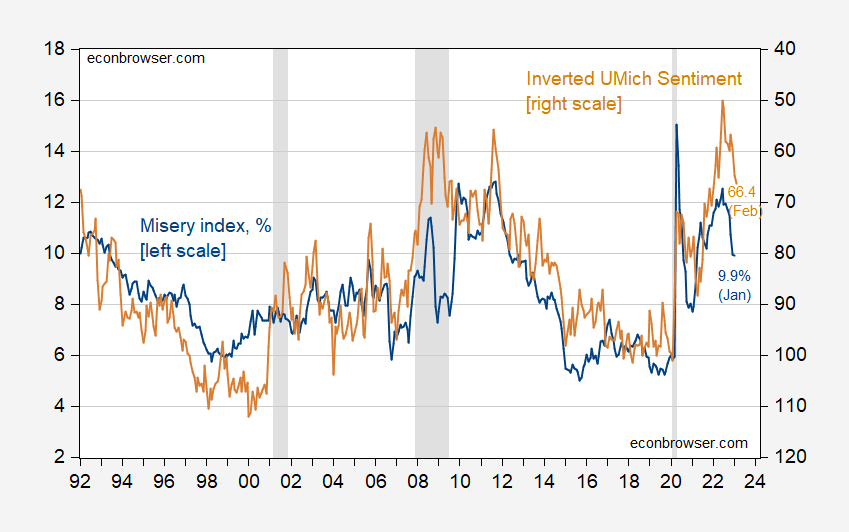

The University of Michigan’s February Consumer Sentiment Index (preliminary) was released today. Here’s the picture (the sequence is inverted, so down is improvement) and the “misery index”, which is the sum of unemployment and year-over-year CPI inflation.

figure 1: Sum of “misery index” unemployment and year-over-year CPI inflation, percent (blue, left scale) and University of Michigan consumer sentiment inversion (tan, right scale). Dates of peak-to-trough recessions as defined by NBER are shaded in gray. Sources: BLS, University of Michigan, all from FRED, NBER and author’s calculations.

This article discusses the link between the Distress Index and the Mood Index (FRED Series UMCSENT). What interests me are the breakouts that seem to have occurred in recent months. consider:

UMCSENT = 51.9 – 4.13suffering – 14.8pgasoline

Regulate-R2 = 0.64, SER = 7.87, DW = 0.23, Nobs = 303, samples 1992M01-2023.01. bold Indicates significance at 10% msl, using HAC robust standard errors.

MISERY has a beta (normalized) coefficient of 0.60 and a log real gasoline price of 0.344, so MISERY has the most significant effect on UMCSENT.

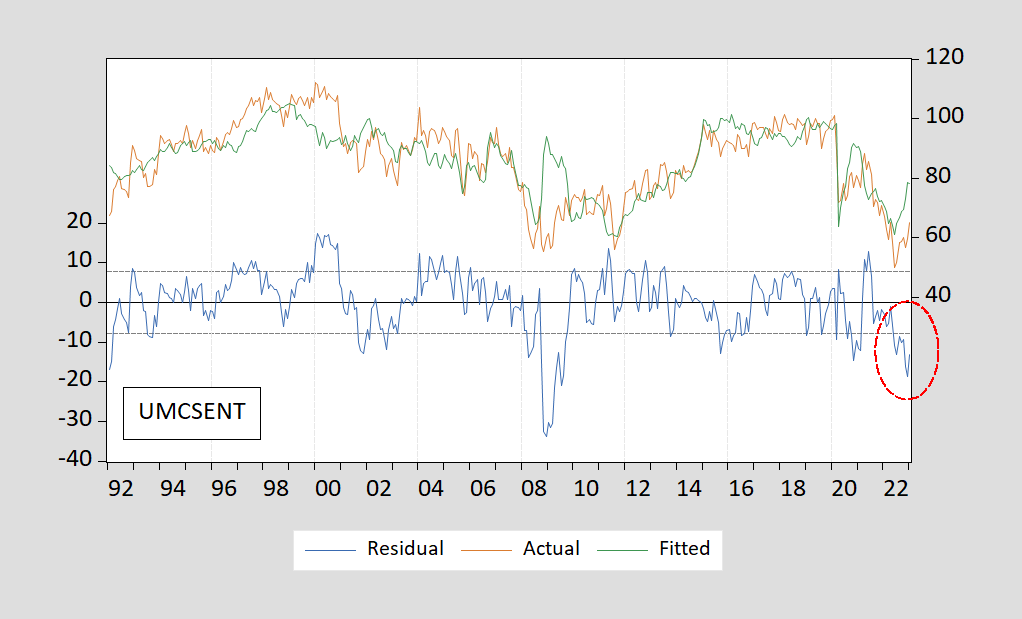

Actual values, fitted values, and residuals are shown below. In December 2022, the prosperity index was overestimated by nearly 20 points.

figure 2: Actual UMCSENT (red) fit (green) and residuals (blue).

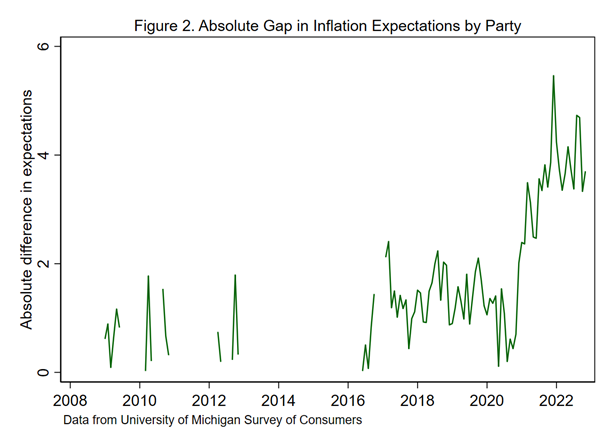

I don’t have a particular explanation for why overforecasting occurs, although it is interesting to note that partisan views on the state of the economy are increasingly divided, as has been documented by others Corolla Binder (2023).

source: Binder (2023).

If the GOP shift is particularly large in the Biden era, it could break the historic relationship between MISERY and UMCSENT.

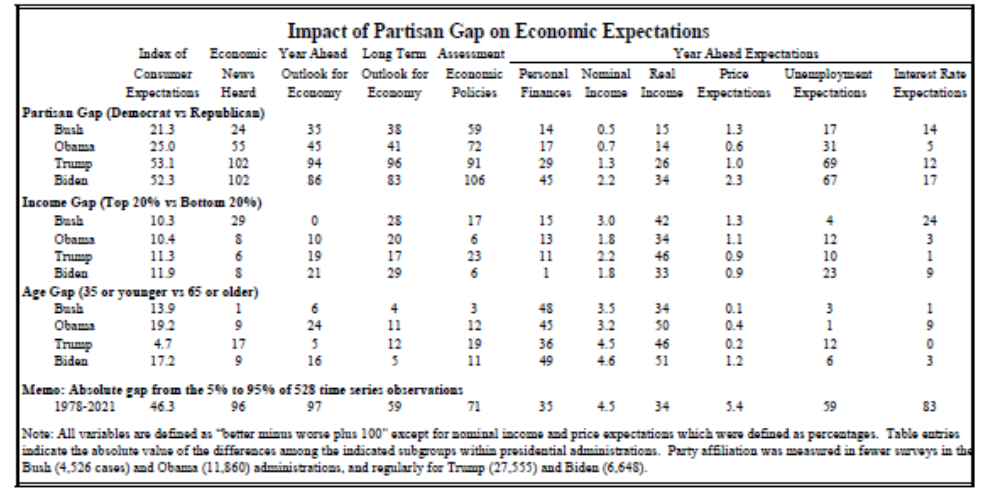

How big is the bias? Curtin (2022) Some slightly older estimates are provided, also based on the Michigan survey.

Curtin wrote:

…under Trump and Biden, the partisan gap was larger than the overall time-series change in the index from optimism to pessimism; the Bush and Obama gap was about half that size.

{kind=link}

{kind=link}