Linda Goldberg and krogstrup There is an article entitled “International Capital Flow Pressures and Global Factors”. They write:

We revisit these issues, recognizing that the observed magnitude of capital flows, exchange rates, and domestic monetary policy responses to global factors are interdependent and cannot be studied in isolation in many countries.In countries with fully flexible exchange

Under an interest rate regime, the exchange rate moves rapidly with initial changes in capital flows, thereby compensating or even avoiding observable adjustments in capital flows (Chari, Stedman, and Lundblad, 2021). In contrast, in fixed exchange rate regimes, managed floating exchange rate regimes, and even in some statutory floating exchange rate regimes, central banks reduce the exposure of realized exchange rates to global factors through policy interventions such as changes in domestic interest rates and official foreign exchange intervention. response (Ghosh, Ostry, & Qureshi, 2018). 1 In such cases, capital flow pressures may be reflected in foreign exchange intervention or policy rate changes rather than in the exchange rate. Therefore, looking at capital flow responses to global factors separately from exchange rate or policy responses will not provide a complete picture of actual capital flow pressures.Taking into account, on the one hand, the interdependence between capital flows and exchange rate changes, foreign exchange intervention, and policy rate changes, we first propose a new measure of international capital flow pressure, which is an improved version of the foreign exchange market pressure (EMP) index. The EMP index is a weighted and proportional sum of exchange rate depreciation, official foreign exchange intervention, and policy rate changes. Earlier versions of FX market stress indices have been used extensively in the literature, from studying balance of payments crises (Eichengreen, Rose, and Wyplosz 1994) to monetary policy spillovers (Aizenman, Chinn, and Ito 2016b) and classifying exchange rates (Frankel 2019 ). However, the weighting and scaling of the inputs has problematic features that cause these indices to mischaracterize pressure patterns across countries and over time, as discussed more extensively in the Appendix.

Instead, our construction derives the relevant weights and proportional terms in the index by exploiting key relationships such as balance of payments, international portfolio demand for foreign assets, and valuation changes in portfolio-related wealth. 2 ……”

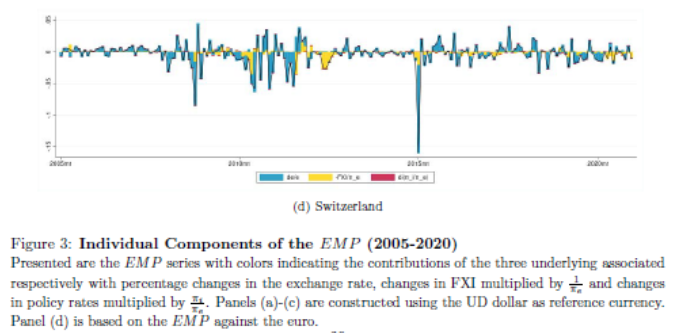

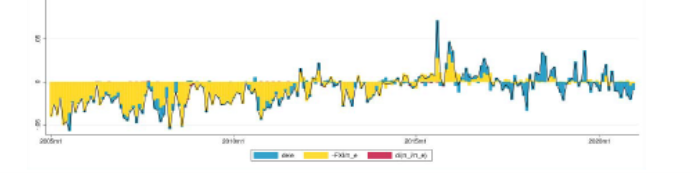

The paper describes in detail the (involved) calculation of their index. Figure 3 in the paper depicts the time series for the four countries. I reproduce panels b and d below (China and Switzerland, respectively).

source: Krogstrup Goldberg (2023).

One observation based on their index:

In times of greatest stress, countries allow on average more exchange rate movements to absorb capital flow pressures than in normal times, even when risk sentiment is high. Some countries may recognize that during periods of extreme stress with high currency pressures, foreign exchange market intervention may not be as effective and may result in a significant loss of official foreign exchange reserves, so they will suffer at least a temporary currency depreciation.

“FX intervention accounts for the majority of EMP not attributable to exchange rate movements. The interest rate component explains nearly all of the variation in very few countries. The contribution of the interest rate component is most pronounced in countries with high inflation and policy rates not constrained by the effective and zero lower bounds . Central banks in these countries have been able to use policy rates more aggressively to respond to capital flow pressures. …”

Some contrary findings on safe-haven currencies:

“…the determinants associated with safe assets have little support in the data, with the size of public debt and gross foreign positions occasionally weakly showing significant associations. Financial Market Development and Financial Openness Over Time, Norm There are country fixed effects and do not distinguish risky behaviors that have realized excess returns.”

Some Econbrowser posts about legacy EMP, and sanctioned russia, Trilemma, manage money inflow.

{kind=link}

{kind=link}