Last Thursday, I talked about Central Time in WPR Regarding the outlook for the national economy and Wisconsin in light of President Biden’s policies. I note that the macro outlook has improved substantially since December, as the economy has proven more resilient than expected and inflation has decelerated more than expected. This is true nationally as well as locally.

Wisconsin Economic Outlook

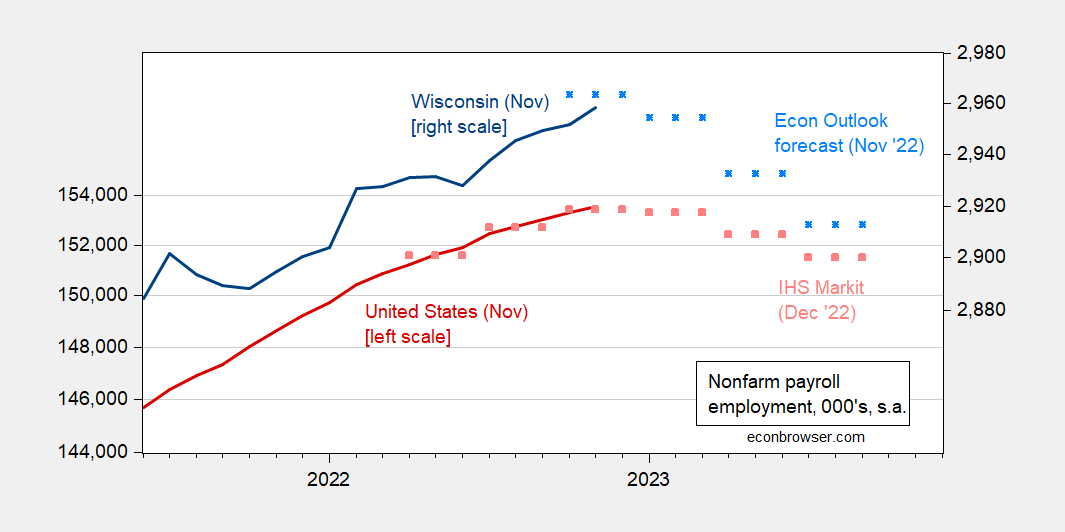

Figure 1 shows the November Wisconsin Economic Forecast Update And December IHS Markit forecasts for countries (economic forecasts are based on IHS Markit forecasts for country inputs). Therefore, the forecast decline in non-farm payrolls is driven by the downturn at the national level.

figure 1: U.S. Nonfarm Payrolls, November Release (red) and December IHS Markit Forecast (pink squares), Wisconsin Nonfarm Payrolls, November Release (blue) and Wisconsin November Economic Forecast Update (sky blue squares) , both 000’s , sa Source: BLS via FRED, IHS Markit (13 December 2022), WI Revenue Department (Novemberreleased in December)

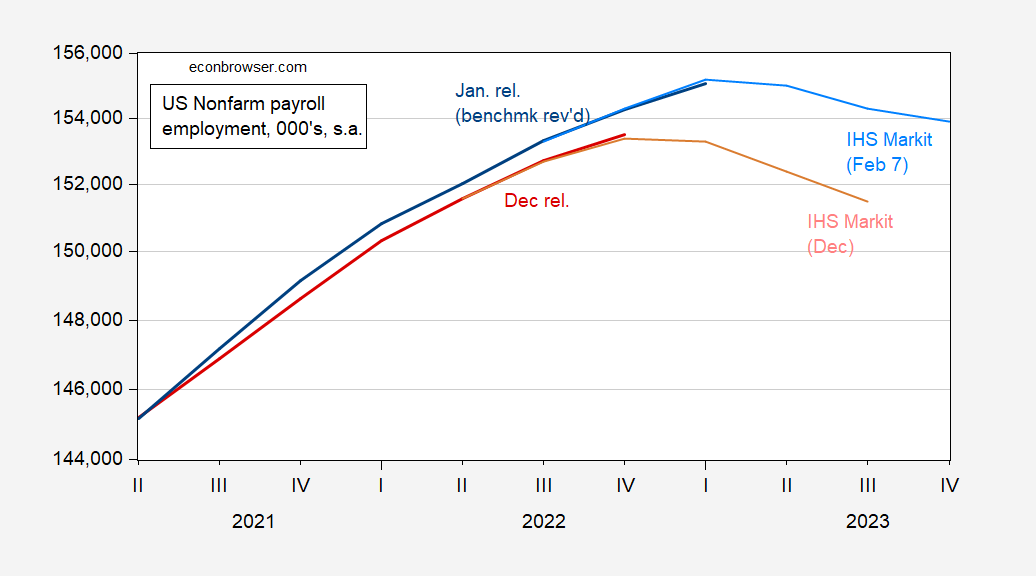

Since November, as discussed in this article, the economic outlook has improved yesterday’s post. Since the Revenue Department’s forecast relies on IHS Markit’s forecast, it is worth looking at how IHS Markit’s forecast has changed since last December, as shown in Figure 2.

figure 2: US non-farm payrolls released in December (red), data released in January (blue), IHS December forecast (pink) and February forecast (sky blue), all in 000, sa Source: BLS via FRED, IHS Dec. 13 and Feb. 7.

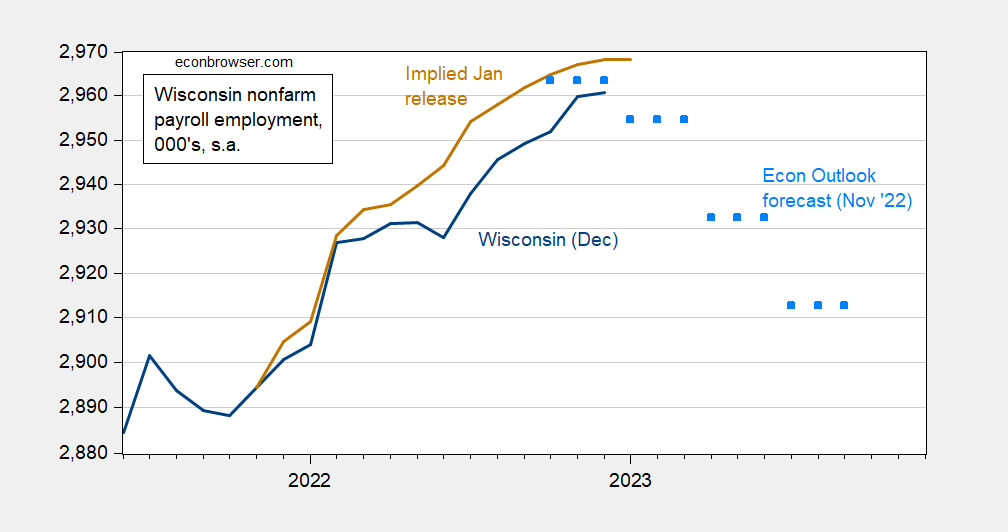

What does this mean for Wisconsin’s prospects? Figure 3 shows the employment data released for December (blue) and the Ministry of Revenue forecast for November (sky blue squares).

image 3: December Wisconsin nonfarm payrolls (blue), November Wisconsin economic forecast update (sky blue squares), and January estimated Wisconsin nonfarm payrolls (brown line). Source: U.S. Bureau of Labor Statistics, WI Revenue Department (Novemberpublished in December) and the authors’ calculations.

Given the upgraded outlook, I expect the next Wisconsin economic forecast to show a less pronounced decline in nonfarm payrolls and a later decline.Given National Benchmark Revision This added about 800,000 to national nonfarm payrolls in December, and we should expect a similar effect on Wisconsin employment. Unfortunately, we won’t see state-level baseline revisions and January data until early March. Therefore, I use the first-difference relationship between Wisconsin employment and national employment in the log, 2021M12-2022M12, to estimate a relationship:

MannpfWi-Fi = -0.002 + 1.44ManNon-farm employmentus

Regulate-R2 = 0.40, SER = 0.0017, DW = 1.90, Nobs = 13, bold Indicates significance at 5% msl using HAC robust standard error.

I then use the baseline revised growth rate of national employment to project the new level of Wisconsin employment (based on actual employment levels in Wisconsin in November 2021). This implied level is shown in Figure 3 as the brown line.

Federal Policy and Its Impact on Wisconsin

How legislation enacted since January 2021 affects Wisconsin’s economy. I noted that several policy measures are already in place, including the bipartisan Infrastructure Act ($1.2 trillion over five years), the Inflation Reduction Act ($40 billion to $800 billion in tax credits, etc.), and CHIPS ($280 billion).

The first measure is the easiest to assess. As of November 2022, $2.7 billion has been allocated, including $2.4 billion for transportation.this Administration expects to allocate about $5.4 billion to Wisconsin finally.use rules of thumb $100 billion in spending results in 1 million FTE-years This means that one person can add about 54,000 person-years of employment. The five-year distribution implies that nonfarm payrolls are about 1% higher than they would otherwise be.

Another way to look at this is to multiply $5.4 billion by 1.6 (Moody’s infrastructure number, CBO range is 0.4-2.2) which is about 0.6% of GDP per year over 5 years (Wisconsin’s 2021 GDP is $303 billion ).

Other terms are more difficult to assess. The Reduce Inflation Act provides substantial tax credits and incentives for green technology investments. If Wisconsin participates as a mid-industrial powerhouse, the increased investment will further stimulate GDP and employment growth.

Finally, the CHIPS Act provides funding to subsidize the construction of semiconductor chip facilities. Wisconsin came close to getting the Intel investment (using the Foxconn facility – that’s another story), but missed out. However, if the supply of semiconductor chips increases, it will lower production costs for Wisconsin manufacturing companies.

And then there are other inactions. In particular, the administration retained Section 232 aluminum and steel tariffs on China, as well as Section 301 tariffs. Since Wisconsin is a user of steel and aluminum, as well as other intermediate inputs imported from abroad, the net retention of these tariffs and restrictions is likely to reduce employment.

Russ (2020) An estimated 75,000 people lost their jobs in 2019 as a result of the steel and aluminum tariffs, and many more are likely to be lost thereafter. Since Wisconsin accounted for about 3.8% of national manufacturing jobs in 2019, that means Wisconsin probably lost about 3,000 manufacturing jobs. That’s about 0.6 of Wisconsin’s 2022 manufacturing employment. (Is this number big or small? Remember, The Scott Walker administration and the Republican legislature will pay up to $3 billion in state funding to lure Foxconn to bring 13,000 jobs to Wisconsin.)

{kind=link}

{kind=link}