(If you’re wondering how to estimate seasonality — you might be right wondering – Then that’s another option. ) QCEW data are not reported on a seasonally adjusted basis, making comparisons with other survey-based, regularly reported BLS series difficult. One way to solve this problem is to use 12-month changes while sacrificing a more current perspective. Here’s how the QCEW series compares to the other two nonfarm payroll growth indicators.

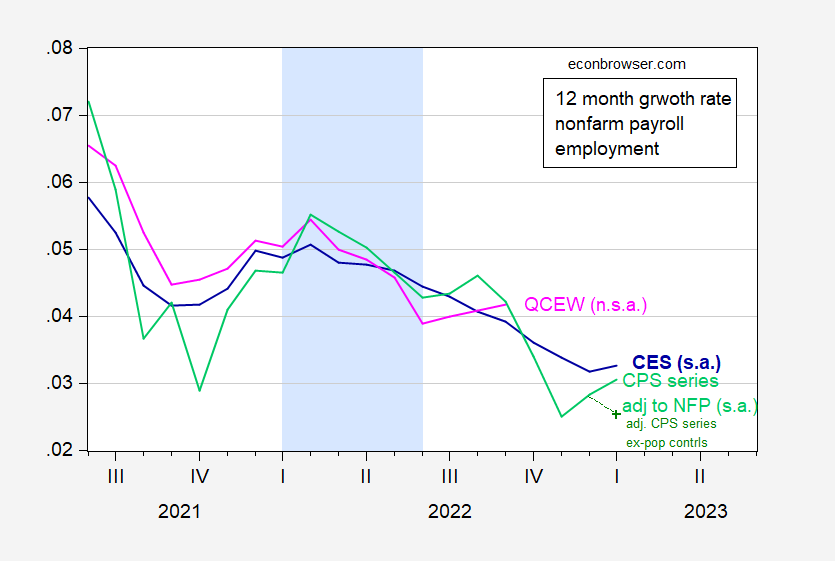

figure 1: 12-month log difference of nonfarm payrolls since January 2023 CES release contains baseline revision, sa (blue), household series adjusted to NFP concept (light green), household series adjusted, excluding January’s population control , sa (green+), total number of workers covered by QCEW, NSA (pink). Light blue shading represents a hypothetical 2022H1 recession. Sources: BLS (various) and ADP via FRED, BLS QCEW, Philadelphia Fed via FRED, and authors’ calculations.

The 12-month growth rate for CES NFP through September 2022 is 3.9% (using seasonally adjusted, or using seasonally unadjusted), compared to 4.2% for QCEW. In numbers, the comparison is 5.9 million versus 6.2 million (CES versus QCEW).

see also this postal.

Total:

- QCEW is currently seeing a large 12-month change in terms of percentage terms and numbers.

- During what some consider to be a hypothetical 2022H1 recession, none of the series have turned negative.

{kind=link}

{kind=link}