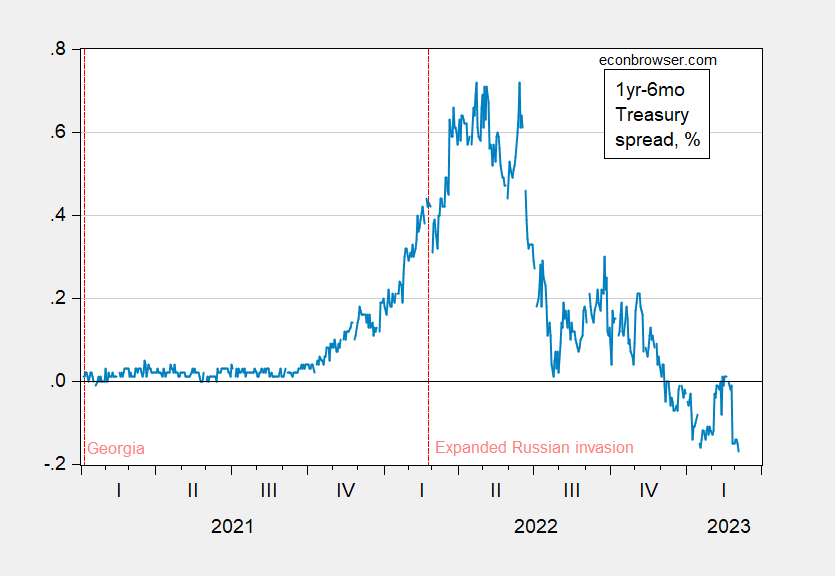

A follow-up recession always seems to be a proposition six months away (as in The Wall Street Journal’s “Gordo’s Recession”), I thought it would be interesting to see if the market has been saying something similar. In other words, this is the Treasury bond spread for six months a year.

figure 1: 1-year minus 6-month Treasury spread, % (light blue). Source: Treasury via FRED, and authors’ calculations.

This inversion of the spread means that the 1-year yield is lower than the 6-month yield. Assuming the pure expectations assumption for term spreads holds (1-year yield is the average of current and expected 6-month yields):

Then the expected 6-month interest rate after 6 months is:

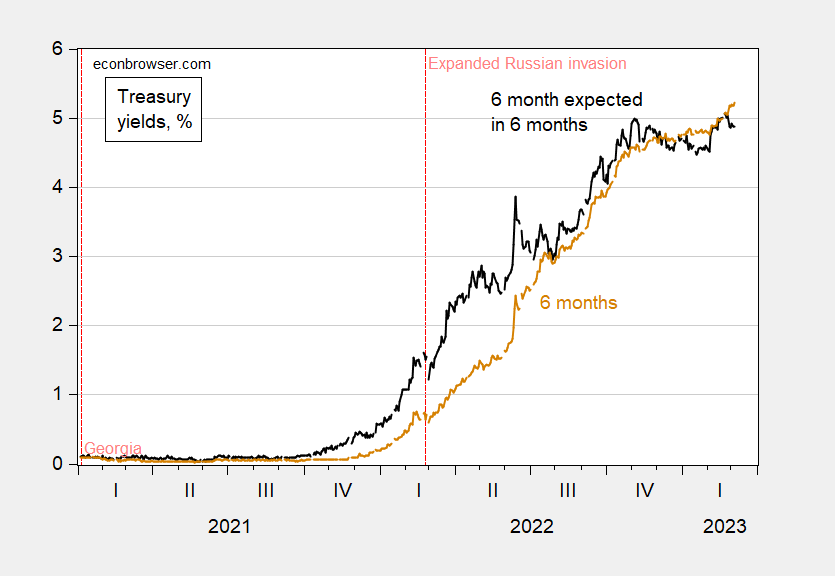

Expected rates 6 months from now are plotted in black in Figure 2 below, while rates for the current 6 months are plotted in tan.

figure 2: 6-month 6-month forward (black) and current 6-month rate (tan), both in %. Source: Treasury via FRED, and authors’ calculations.

The 6-month to 1-year segment of the yield curve is very flat at the end of July and in December 2022. If people think that the recession hits with lower interest rates, the recession has been early for the past six months, on and off for the past seven months.

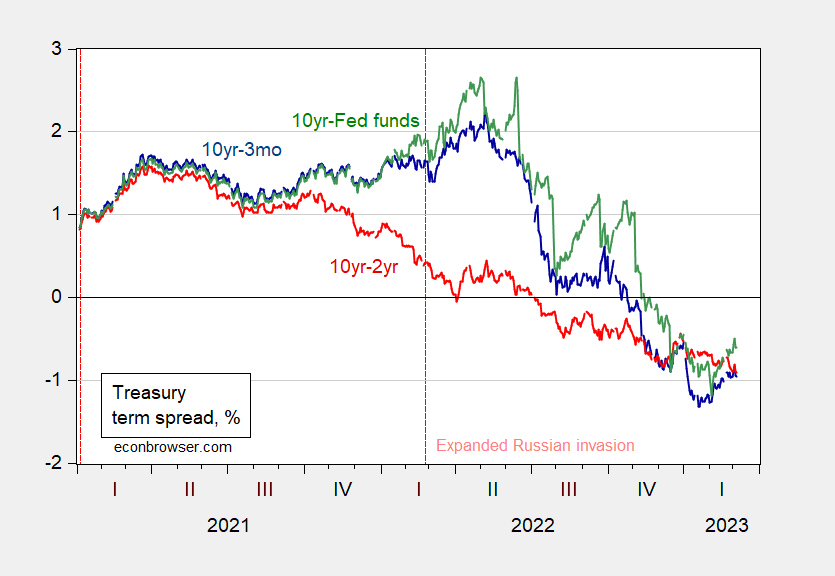

I would note that the 10yr-3mo and 10yr-2yr spreads suggest a recession is imminent.

image 3: 10Y-3M Treasury Spread (blue), 10Y-2Y Spread (red), and 10Y-Fed Funds Spread (green), all expressed as percentages. Source: Treasury via FRED.

Based on historical correlations, expect a recession around Q2/Q3.

{kind=link}

{kind=link}