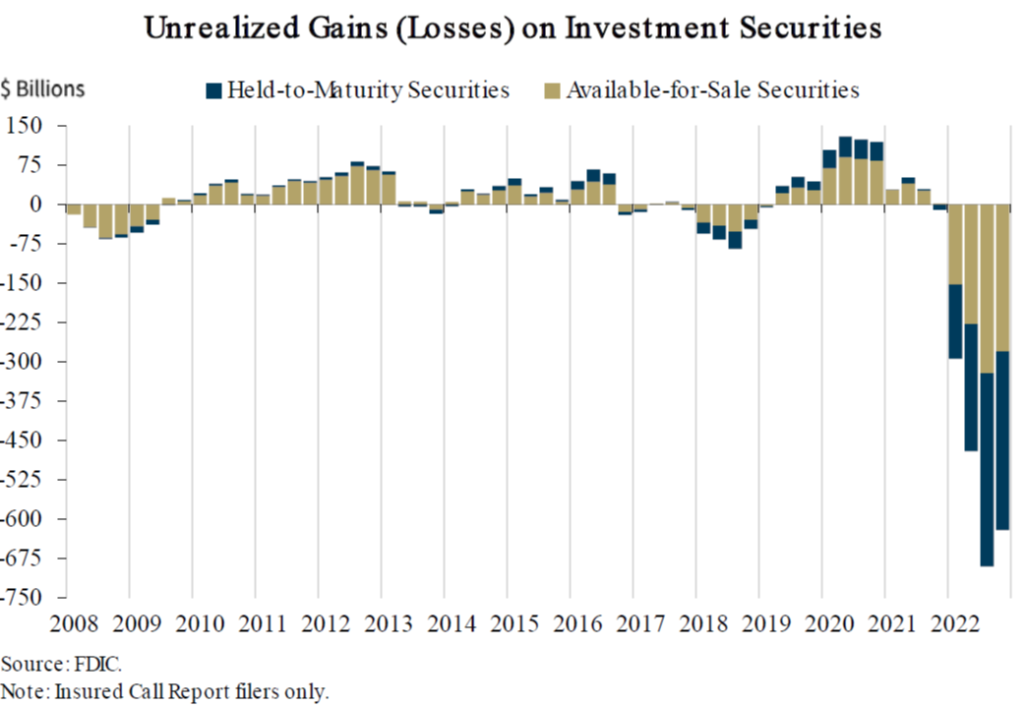

Consider the following chart reporting unrealized losses on securities held by banks (from Rupkey/This Week in Financial Markets):

source: Rupkey, “This Week in Financial Markets,” March 20, 2023.

This makes me wonder what makes these unrealized losses go to zero? Interest rates have dropped significantly. I don’t have the data at hand to do the calculations, but I do have marketable federal debt at par and market. I can look at the ratio of the two, and how that ratio varies with a given interest rate.

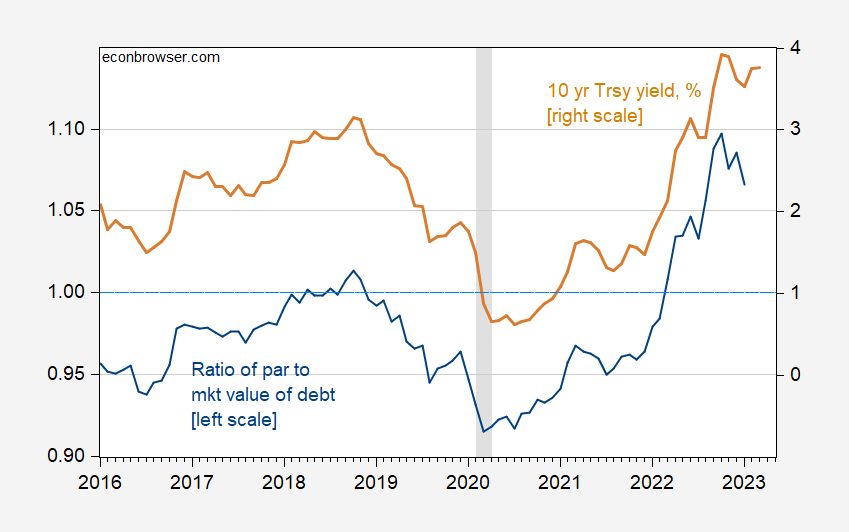

figure 1: Ratio of marketable debt par to market value (blue, left scale) and 10-year Treasury yield, % (tan, right scale). Dates of peak-to-trough recessions as defined by NBER are shaded in gray. Sources: Dallas Fed, Treasury Department, NBER, and authors’ calculations.

There is an obvious correlation. Return from:

ratio = 0.8817 + 0.0455(GS10)

adjust-R2 = 0.83, NObs = 85, DW = 0.20

Using this correlation, it turns out that a 10-year yield of 2.6% would do the trick (3.8% as of March, about the same as in February). Obviously, this is rough (the face value to market price ratio is not the same as the purchase price to market price ratio), but you’d think some of the unrealized losses would disappear if yields fell.

How plausible is this result? Not immediately, but I’ll note that the 10-year rate has dropped half a percentage point since early March…

{kind=link}

{kind=link}