Influenced by SVB, income and expenditure, and PCE releases.

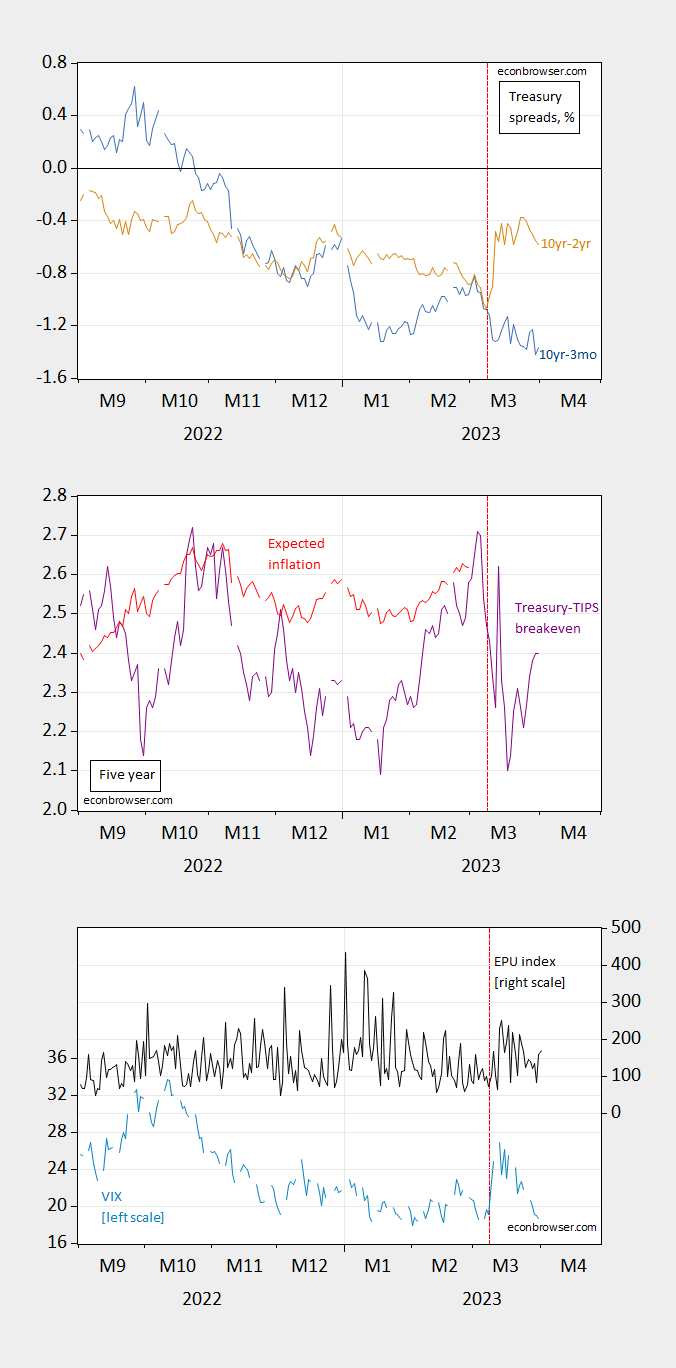

figure 1: Top: 10-3M Treasury spread (blue), 10-2Y spread (tan), both in %; Middle: 5-Year Treasury-TIPS spread (purple), 5-year Period spreads adjusted for liquidity and risk premiums (red); bottom panels: VIX (sky blue, left scale), EPU (black, right scale). Source: Treasury via FRED, kilowatt Follow D’amico, Kim and Wei (DKW), CBOE via FRED, policyuncertainty.com.

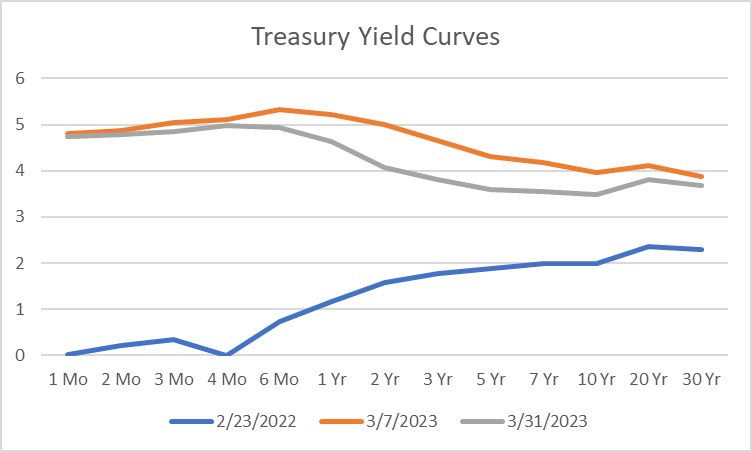

From 10 years to 2 years has risen, but from 10 years to 3 months is still deep in the negative area. Here’s the yield curve on Friday relative to SVB ahead and Ukraine ahead.

source: treasury.

Before Ukraine, the yield curve showed continued growth. Even before the SVB collapse, the yield curve was already inverted along most of the spectrum, and after the SVB collapse, it inverted even more in the 2 yr-6 mos portion.

The 5-Year TIPS spread has fallen, although the premium could change as well, it’s hard to say what that means. Risk, as measured by the VIX, has also declined, while uncertainty as measured by Baker, Bloom & Davis’ “news”-based measures remains high.

I do think it’s interesting that 5 years TIPS has dropped. In fact, essentially the entire decline in nominal interest rates has been caused by a decline in real interest rates, which indicates less economic activity.

Oil prices rise on OPEC+ pledge to cut output, which could change interest rates (next post).

{kind=link}

{kind=link}