Today, we are pleased to present the contribution of our guest Laurent Ferrara (Professor of Economics, Skema Business School, Paris, international association of forecasters).

in the current context high inflation, problems arose with the way central banks controlled inflation and their strategies to achieve their goals. Since 1990, the world’s major central banks have gradually adopted an inflation targeting framework. This means that their price stability target is achieved by around a target value (e.g. 2% the fed and European Central Bank).

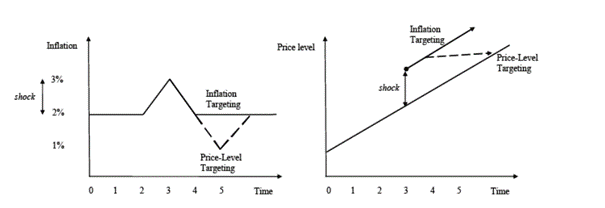

A well-known problem with this approach to inflation targeting is that by focusing on the growth rate of prices, it does not take into account the value of past inflation rates. We say “in the past”. Averaging 2% over time, as the Fed has done, is one way to alleviate this problem. Another approach is to target price levels directly. This approach provides greater flexibility by accounting for deviations from the target after unexpected shocks. For example, assuming an inflation target of 2%, if inflation rises to 3% after a given shock, rational economic agents would expect inflation to be 2% after this shock and only 1% below the price level % target system.This is well explained in Figure 1 taken from this VoxEU Post.

figure 1: Comparison of Inflation and Price Level Targets

Source: Minford and Hatcher, 2014, VoxEU

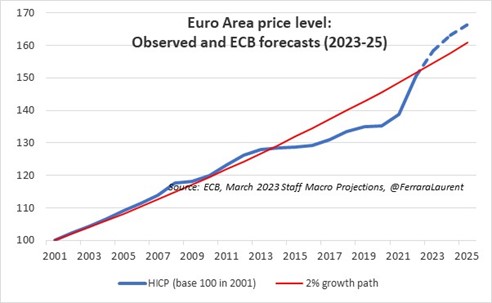

It is useful to look at the Eurozone from a price level analysis perspective. Since 2001, the level of inflation has been below the price level implied by a 2% inflation rate, and the observed price level is now almost at the “theoretical” price level in 2022 (see Figure 2). Thus, the sharp rise in price levels in 2021-22 erases the evolution of the nine-year trend below 2%.

figure 2: The price level in the euro area and the price level implied by the 2% path

Source: Eurostat and ECB macro forecasts March 2023

Interesting to consider the ECB in its inflation forecast for 2023-25 March 2023 Staff Macro Forecasting Exercise (+5.3% in 2023, +2.9% in 2024, +2.1% in 2025): Price levels may continue to exceed the “theoretical” price levels implied by the 2% growth path. For the first time in the history of the euro area, we will observe a significant and persistent gap between the two lines of Figure 2 (about 3.5% in 2025), suggesting that citizens of the euro area will always face high prices for goods and services. Moreover, if we assume that inflation will return to the 2% target after 2025, then the two lines will evolve in parallel after that date (as shown in the right panel of Figure 1).

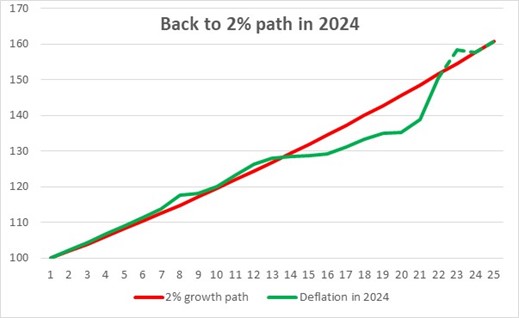

So how can policymakers close this gap? The first option is to tighten the stance of monetary policy to bring the price level back to the 2% path line. That’s what the ECB is currently doing by raising its main refinancing rate. But this tightening of monetary policy can be achieved in two ways: hard or soft. By generating around -0.5% deflation in 2024 (Chart 3), hard deflation would mean a quick return to the 2% line. This scenario is likely to also mean a recession in the Eurozone in 2024.

image 3: Deflationary price level scenarios in 2024

Source: Eurostat and authors’ calculations

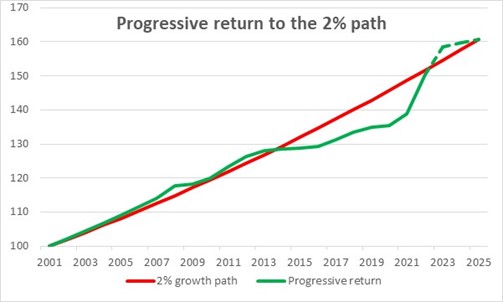

Moderate monetary tightening implies inflation well below the 2024 and 2025 targets. For example, an inflation rate of 0.8% in 2024 and 0.7% in 2025 would return the price level to a 2% path in 2025 (see Figure 4). The second scenario is of course preferred, as the eurozone would certainly avoid a recession and all its associated costs in terms of jobs and incomes.

Figure 4: Asymptotic Regression 2% Path Price Level Scenario

Source: Eurostat and authors’ calculations

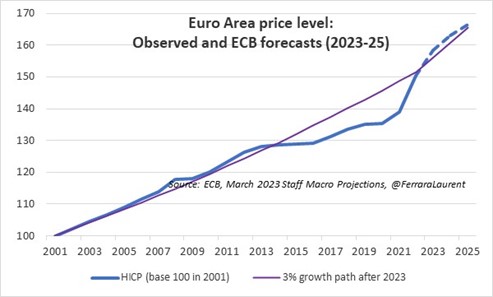

There is a second option, more complex to implement, but often advocated by leading economists, e.g. Olivier Blanchard, that is, raising the inflation target. After all, there is no strong theoretical argument for a value of 2%. This value is largely based on past periods in which policymakers believed prices were stable. So why not use a 3% or 4% target? Figure 5 shows the theoretical impact of moving to a 3% inflation target from 2023 onwards. We see that the expected price level will be in line with that implied by the 3% inflation target.

Figure 5: Price level scenario with a target of 3% from 2023

Source: Eurostat and authors’ calculations

Price level analysis suggests that the ECB is likely to continue tightening its monetary policy stance in the coming months to avoid a persistent gap between the observed headline price level and that implied by the euro area’s 2% inflation target. The alternative is to raise the inflation target, but that’s another story that will spark debate in academic and policy circles for months to come…

This article was sponsored by Laurent Ferrara.

{kind=link}

{kind=link}