gentlemen. steven corbett Assert that the Philadelphia Fed’s early preliminary benchmarks support a recession in the first half of 2022, namely:

You, Menzie, are more likely to be correct with the Est Survey. You wrote: So: (1) I give more weight to the institutional series, (2) the gap between the two series is more likely to be due to increasing and biased measurement error in the family series, rather than, for example, being primarily There has been an increase in the number of people wearing multiple hats. https://econbrowser.com/archives/2022/12/the-household-establishment-job-creation-conundrum

Big mistake, because it turns around. As expected.

You’re wrong because you haven’t considered statistics more holistically. This is where your students learn. If your dial is telling you different things, cross check your indicators. If employment is growing faster and faster, then GDP should also be rising. If jobs are growing rapidly, so should mobility and gasoline consumption, because so many people in this country drive to work. Finally, if productivity is collapsing while jobs are being added, you really need to pause and put together some narrative about why this is happening. It indicates an anomaly in the data that needs to be examined more closely.

If you did, Menzie, you’d probably come to the same conclusion as the Philly Fed…

What is left of the assumption?So, on March 16, the Philadelphia Fed released this renew.

source: Federal Reserve Bank of Philadelphia.

from Report:

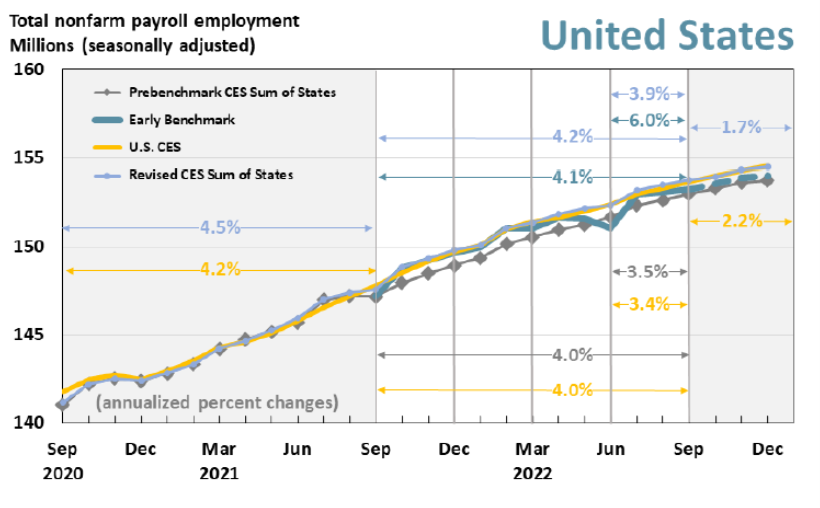

For the full year ending in the third quarter of 2022 — including additional QCEW data changes affecting the first three quarters — jobs grew by 4.1% in the 50 states and the District of Columbia.

• Employment rose 4.0%, based on the benchmark pre-CES aggregate of states and US CES.

• Revised aggregate CES growth of 4.2%.

This EB estimate corresponds to a net gain of 6,072,000 new jobs over the period, rather than the 5,825,500 estimated by states combined; US CES estimates a net gain of 5,904,000 jobs over the period.In the third quarter of 2022, after adjusting for QCEW data, employment in the 50 states and the District of Columbia increased by 6.0%.

• Job growth based on state-by-state benchmark pre-CES sum and US CES 3.4% and 3.5%respectively.

• Revised combined CES state growth of 3.9%.

• This EB estimate corresponds to a net gain of 2,203,200 new jobs over the period, rather than the 1,322,100 estimated by states combined. US CES estimates a net gain of 1,270,000 jobs over the period. [bold italics added – MDC]

i argued before Refutation of Kopits 2022H1 Labor Market Recession Hypothesis These estimates are subject to revision. So many of them, in fact, that (1) the previously estimated recession has largely been eliminated, and (2) job growth will continue through the third quarter of 2022.

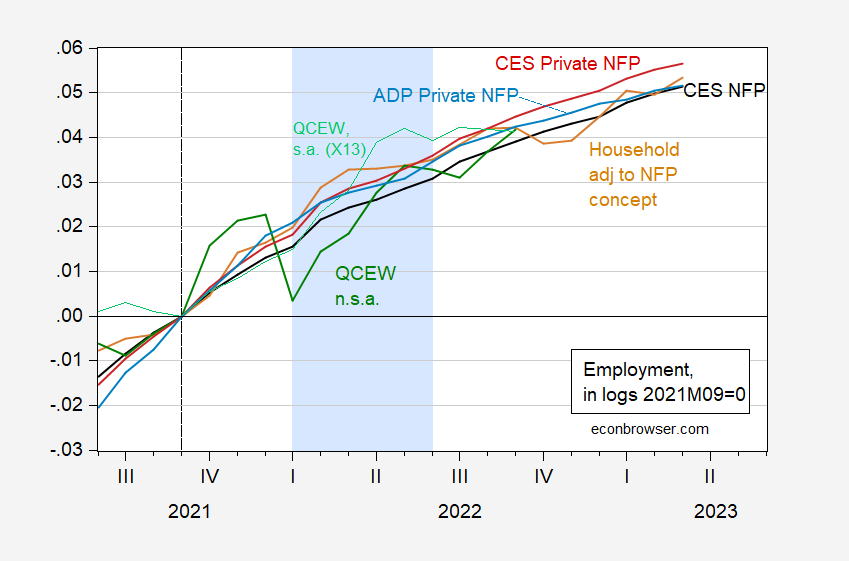

I don’t think it’s wise to rely on just one series, so in Figure 1 I show CES, CPS and ADP estimates for NFP or private NFP, or the QCEW table covering employment.

figure 1: Cumulative percent change for CES nonfarm payrolls (black bold), CPS civilian employment adjusted for the NFP concept (tan), CES private nonfarm payrolls (red), ADP private nonfarm payrolls (light blue), quarterly employment and Census of Wages (QCEW) total employment, seasonally adjusted using log X-13 (light green), and QCEW total employment, not seasonally adjusted (dark green), both since 2021M09. Light blue shading represents Steven Kopits’ hypothetical recession. Sources: BLS, ADP via FRED, and authors’ calculations.

Taken together, I do not see a recession in the first half of 2022 (although the data will be further revised).However, as noted earlier, momentum in 2022 does not guarantee a recession-free 2023 here.

{kind=link}

{kind=link}