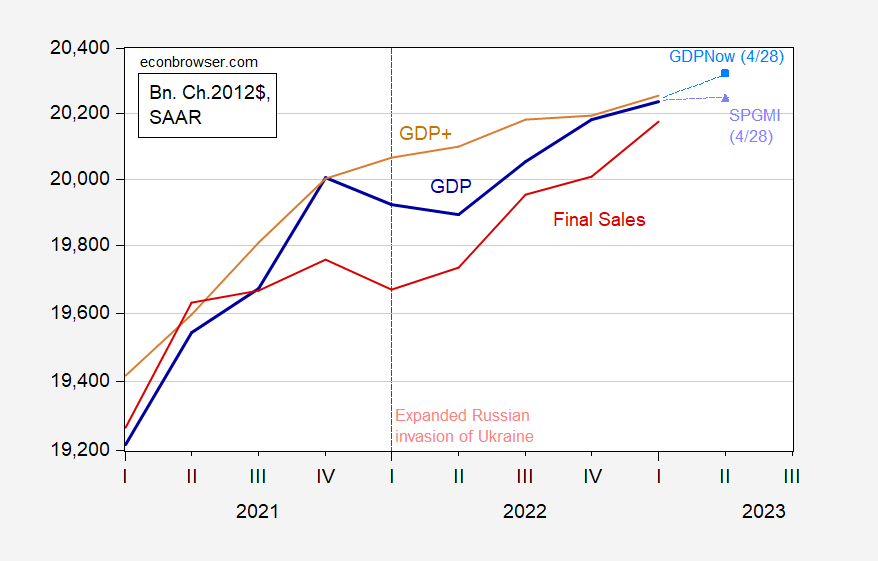

Jim pointed to repeated delays in long-forecast recession in his Thursday postal. Here are some additional thoughts on the past and future of economic activity in light of additional data. GDPNow (reaching first quarter growth target) indicates continued growth in the second quarter. S&P Global Market Insights (formerly Macroeconomic Advisors) said it had plateaued. Final sales (ie GDP excluding inventories) point to continued growth.

figure 1: GDP (bold dark blue), GDP+ (tan), final sales (red), GDPNow now forecast for 4/28 (sky blue squares), S&PGMI tracking as of 4/28 (lavender triangles), all in ten The unit is 100 million. 2012 $SAAR. Source: BEA 2023Q1 advance, Federal Reserve Bank of Philadelphia, Federal Reserve Bank of AtlantaS&PGMI, and author’s calculations.

My interpretation of these data, including the fact that GDO and GDP+ seem to better reflect the trajectory that GDP ultimately describes (given that GDP has been revised several times over time), is that economic activity decelerates in the first half of 2022 ( Aggregate demand actually fell), but there was no recession following Russia’s expanded invasion of Ukraine and the ensuing cost-push shock. Economic activity is likely to continue to rise into the second quarter of 2022, although growth will be subdued.as in a Previousmany forecasts set the decline in 2022Q3 or 2022Q4.

{kind=link}

{kind=link}