from ford and duncan, Journal of Structured Finance (2020):

source: Ford and Duncan (2020).

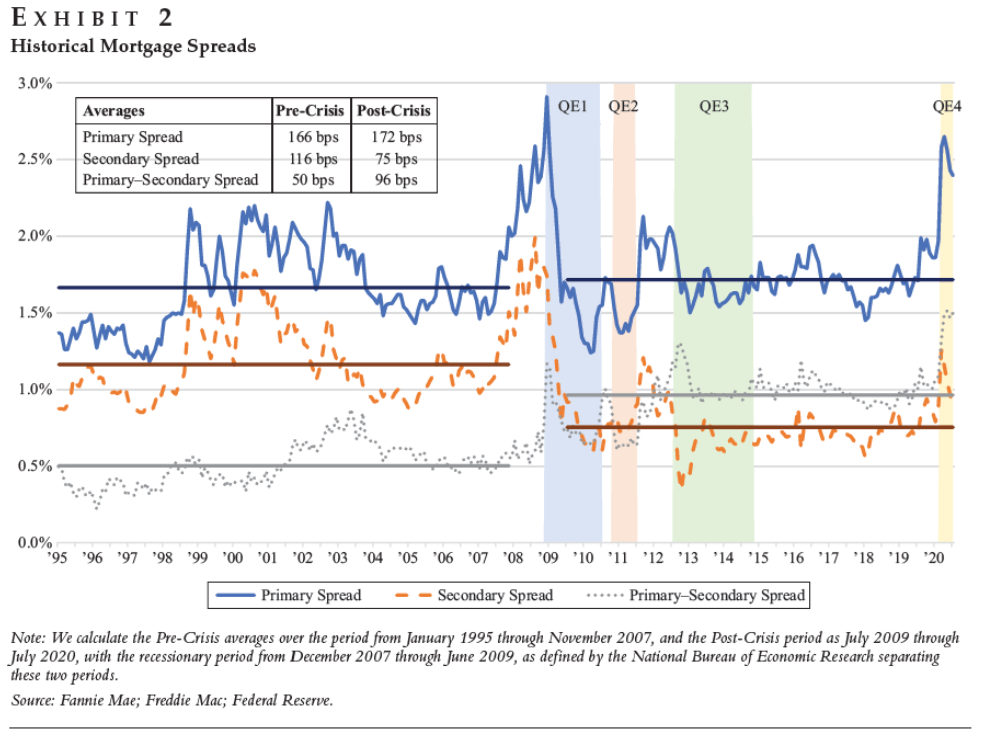

The “prime spread” is the 30-year fixed-rate mortgage rate and the 10-year Treasury rate. The “secondary spread” is the difference between the return on mortgage-backed securities and the 10-year Treasury note. The “subprime spread” is the difference between the 30-year fixed-rate mortgage and the return on mortgage-backed securities.

From summary:

• Mortgage spreads, especially the primary-secondary spread (mortgage rate vs. current MBS coupon yield) remain at historically high levels following the COVID outbreak in the US.

• Increased liquidity in the mortgage-backed securities (MBS) market has coincided with increased MBS purchases by the Federal Reserve, which has historically been associated with lower secondary spreads (current coupon yields on MBS vs. The post-COVID scenario coincided with a surge in Fed MBS purchases followed by a decline in secondary spreads.

• Historically, increases in primary-subprime spreads have been correlated with increased capacity constraints faced by lenders, as measured, for example, by increased output per mortgage-related employee. The continued expansion of primary and secondary school transmission following COVID-19 is consistent with this historical pattern.

{kind=link}

{kind=link}