Today, we present an article by David Paper and Russandra ProdinProfessor of Economics and Teaching Associate Professor at the University of Houston.

At its May 2023 meeting, the Federal Open Market Committee (FOMC) raised the target range for the federal funds rate (FFR) by 25 basis points to between 5.0% and 5.25%. Rates were then raised by a total of 4.75 percentage points between March 2022 and March 2023, before being at the effective lower bound (ELB) for two years. Apart from the March 2023 Summary of Economic Projections (SEP), the FOMC did not provide any guidance on the future path of FFR.

The Fed is widely believed to be “behind the curve” by not raising rates in 2021 when inflation rises, forcing it to “catch up” in 2022. However, without measuring “on the curve.” In the latest version of our paper, “Policy rules and forward guidance in the wake of the Covid-19 recession’, we compare policy rule mandates with actual and FOMC forecasts for FFR, using data from the SEP from September 2020 to March 2023. The difference between actual or projected FFR.In our post we analyze four policy rules related to the future path of FFR:

this Taylor (1993) The rules for the unemployment gap are as follows,

where is the rule-regulated short-term federal funds rate level, is the inflation rate, is the 2% target inflation level, is the long-run unemployment rate of 4%, is the current unemployment rate, and is the ½% neutral real rate of the current SEP.

Yellen (2012) The balanced approach rule is analyzed, where the coefficient for the inflation gap is 0.5, but the coefficient for the unemployment gap is raised to 2.0.

The balanced approach rule received considerable attention after the Great Recession and became a standard policy rule used by the Federal Reserve.

These rules are non-inertial because the FFR is fully adjusted whenever the target FFR changes. That’s at odds with the FOMC’s approach of steadily raising rates as inflation rises.We specify the rule-based inertial version Clarida, Gary and Gertler (1999),

Where p is the degree of inertia and is the target level of the federal funds rate specified by equations (1) and (2).we set to Bernanke, Keeley and Roberts (2019). Equal to the rate specified by the rule if positive, or zero if the specified rate is negative.

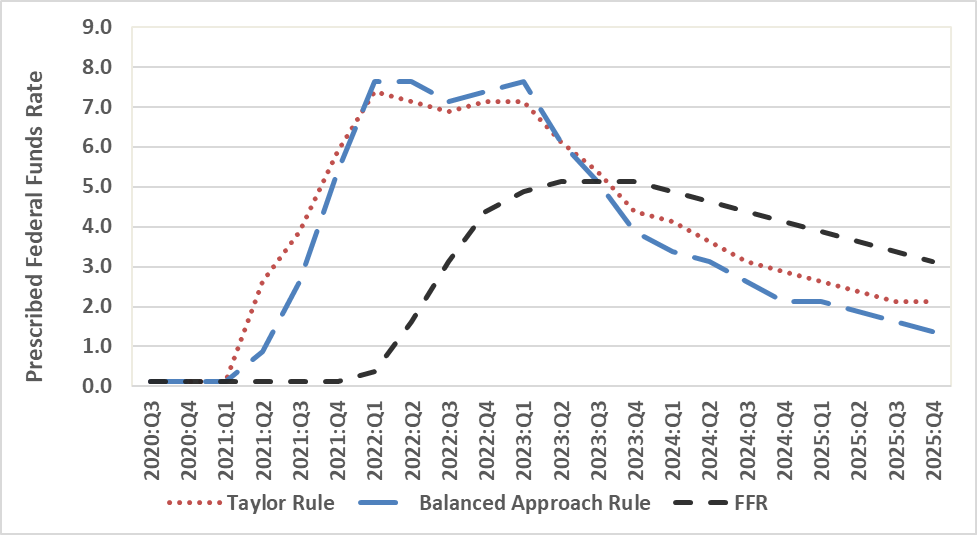

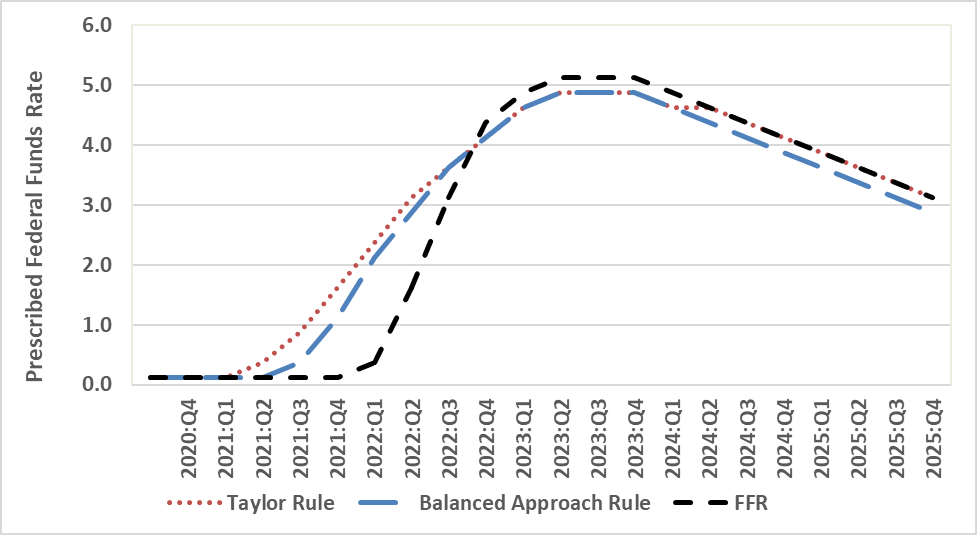

Figure 1 plots the midpoint of the FFR target range from September 2020 to March 2023, and the projected FFR from the March 2023 SEP to June 2023 to December 2025. After exiting the ELB to 0.375 in March 2022, the FFR rose to 5.125 in May 2023 before declining in 2024 and 2025. The figure also depicts policy rule provisions. For the September 2020 to 2023 race, we use real-time inflation and unemployment data available during FOMC meetings. For the period June 2023 to December 2025, we use the March 2023 SEP’s inflation and unemployment forecasts. The difference in FFR specified between inertial and non-inertial rules is much larger than the difference between Taylor and equilibrium method rules.

For non-inertial Taylor and balance method rules, the policy rule specification is reported in Panel A of Figure 1 . They are inconsistent with the FOMC’s approach of slowly raising the FFR as inflation rises. Through March 2021, the ELB’s regulations for both rules are the same. The FOMC is behind the curve starting in June 2021, when the mandated FFR increases from 0.125 for the ELB to 2.625 for the Taylor Rule and 0.875 for the Balanced Approach Rule, while the actual FFR stays with the ELB. Policy rule rules increase sharply in 2021 and peak in March 2022 with Taylor rule at 7.325 and Balanced Approach rule at 7.625 when FFR first rises above the ELB to 0.375. The gap also peaks in March 2022 at 700 basis points for the Taylor rule and 725 basis points for the balanced approach rule. The gap between March 2022 and March 2023 narrowed considerably, as the FFR rose from 0.375 to 4.875, while the mandated FFR barely changed. Looking ahead, the gap between FFR forecasts and policy rule mandates is virtually zero in September 2023, and from December 2023 to December 2025, FFR forecasts are higher than policy rule mandates.

Figure 1, panel A: Fed Funds Rate and Policy Rule Prescription, Non-Inertial Rules

Panel B reports results for inertial Taylor and equilibrium method rules. They are more in line with the FOMC’s approach of slowly raising the FFR as inflation rises. The ELB rules are the same for both rules through March 2021, rising to 0.375 for the Taylor rule by June 2021. The FOMC is behind the curve starting in September 2021, when the mandated FFR increases to 0.875 for the Taylor rule and 0.375 for the balanced approach rule, while the actual FFR stays at the ELB. The gap between policy rule provisions peaks in March 2022 at 200 basis points for the Taylor rule and 175 basis points for the balanced approach rule. At that time, the FFR under the Taylor rule was 2.325, the FFR under the balanced approach rule was 2.125, and the FFR first rose above the ELB to 0.375.

Figure 1, panel B: Fed Funds Rate and Policy Rule Prescription, Inertial Rule

The Fed is no longer behind the curve. The gap narrows steadily, with FFR 25 basis points above both policy mandates by December 2022. The inertia rule provides for a much smoother path of rate hikes from September 2021 to December 2022 than the one adopted by the FOMC. Had the Fed followed the inertial Taylor or Balanced Approach rules instead of the FOMC’s forward guidance, it could have avoided the lagging curve, pivot, and back-on-track pattern of Fed policy in 2021 and 2022. Looking ahead, the gap between FFR forecasts and Taylor Rule mandates remains at 25 basis points between June 2023 and March 2024 and zero between June 2024 and December 2025. The gap between the balanced approach rule provisions remains at 25 basis points through December 2025. The Fed follows the inertial Taylor rule.

This article was sponsored by David Paper and Russandra Prodin.

{kind=link}

{kind=link}