Answer: Yes, and (to a lesser extent) yes.

Consider the current situation.

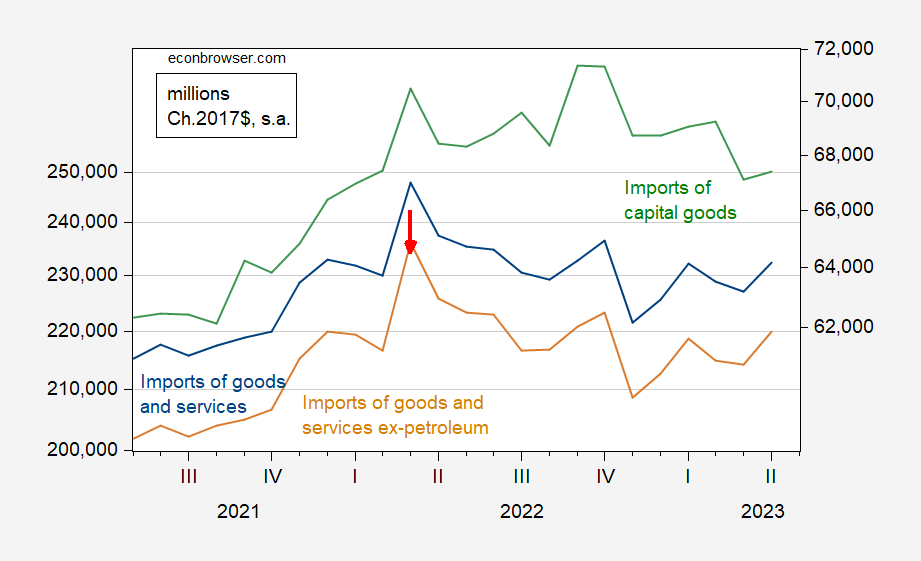

figure 1: Imports of goods and services (blue), imports of goods and services other than petroleum (tan), imports of capital goods (green, right axis), all in millions of Ch. 2017 USD. Source: Bank of America Economics.

Actual imports of goods and services excluding oil peak in March 2022. They and total imports remain below these levels. Capital goods imports – which should reflect more forward-looking behavior – peak in September 2022.

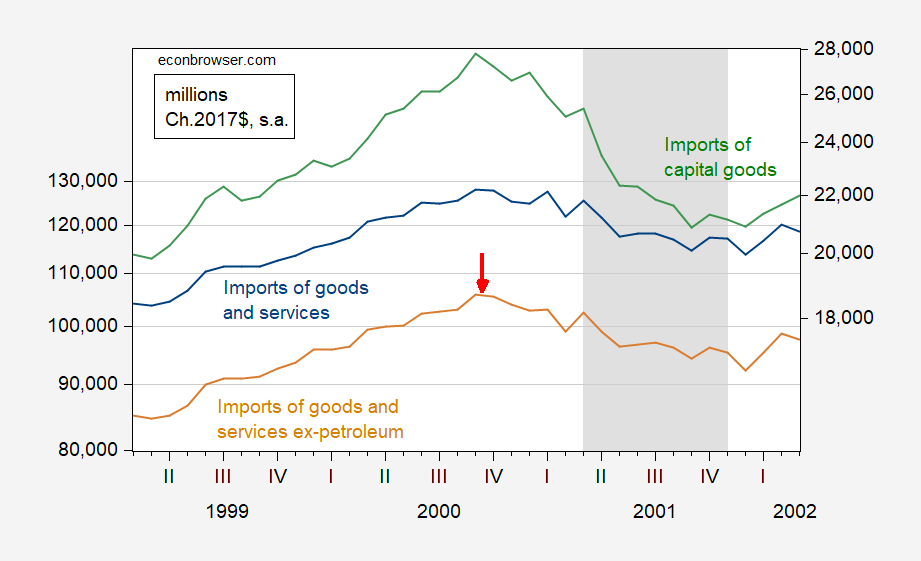

Real imports did peak just before the 2001 recession.

figure 2: Imports of goods and services (blue), imports of goods and services other than petroleum (tan), imports of capital goods (green, right axis), all in millions of Ch. 2017 USD. Dates of peak-to-trough recessions as defined by the NBER are shaded in gray. Sources: BEA, NBER.

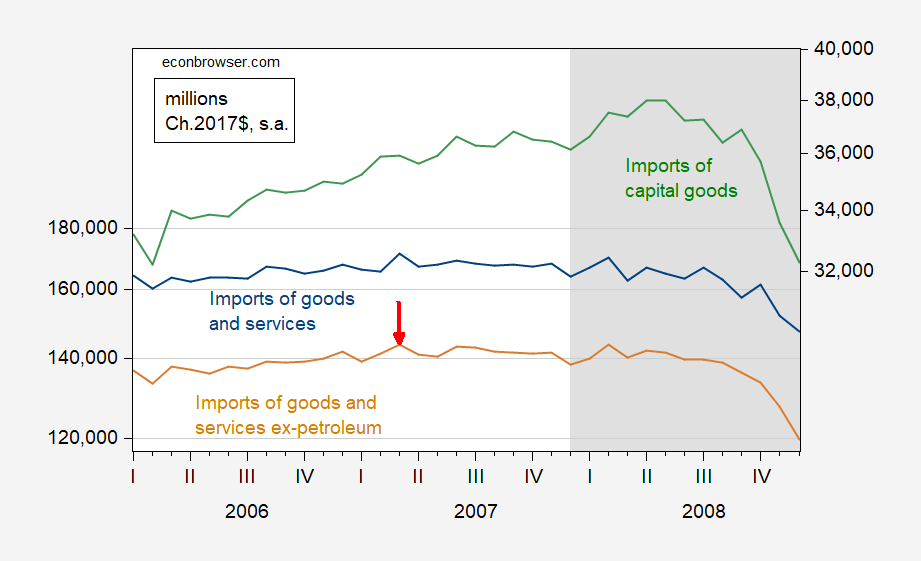

On the other hand, while imports other than oil peaked in March 2007 (technically they actually peaked slightly in February 2008), capital goods peaked in April 2008, the NBER-defined recession almost months.

image 3: Imports of goods and services (blue), imports of goods and services other than petroleum (tan), imports of capital goods (green, right axis), all in millions of Ch. 2017 USD. Dates of peak-to-trough recessions as defined by the NBER are shaded in gray. Sources: BEA, NBER.

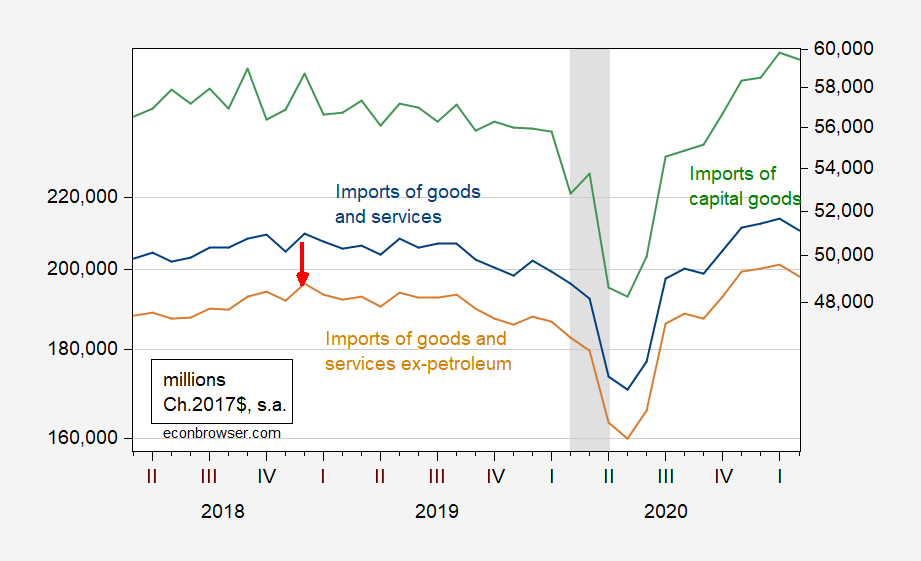

Finally, during the last recession, imports other than oil peaked in December 2018. Imports of capital goods actually peaked in September of that year.

Figure 4: Imports of goods and services (blue), imports of goods and services other than petroleum (tan), imports of capital goods (green, right axis), all in millions of Ch. 2017 USD. Dates of peak-to-trough recessions as defined by the NBER are shaded in gray. Sources: BEA, NBER.

Thus, total real imports are usually a relatively reliable precursor to recession (not necessarily for subcategories such as capital goods), at least in the past three recessions. What about misreporting – that is, when imports fell but no recession occurred. One wants to think about long periods of flat or declining imports, say half a year. On a quick check, there appears to be only one such case – March 2015, and then it took 2.5 years to return to that level. There was no NBER-defined recession then, but as many have pointed out, the manufacturing recession began in December 2014 due to the appreciation of the dollar.

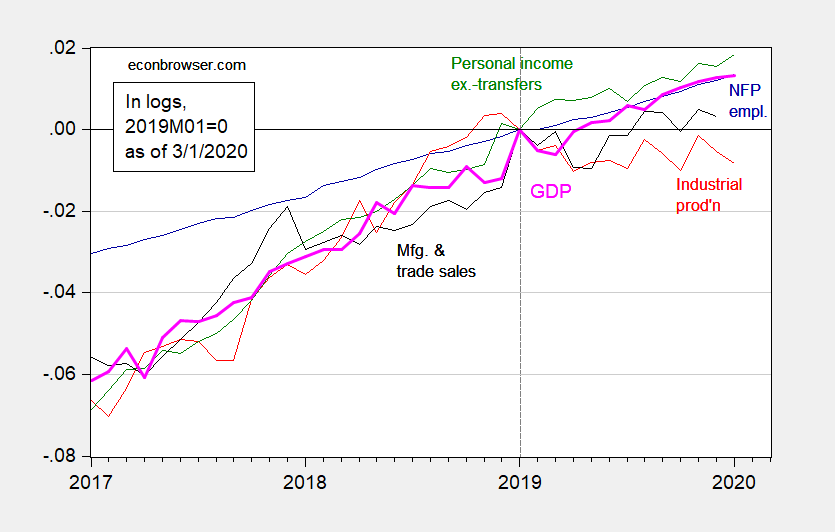

This set of findings suggests that the U.S. would likely have entered a recession had the pandemic not occurred.Below is a graphic of the NBER key series, using real-time data (i.e. data reported through March 1, 2023) (from postal).

Figure 5: 2012 nonfarm payrolls (blue), industrial production (red), personal income excluding transfers (green), 2012 manufacturing and trade sales (black), and 2012 monthly GDP (pink), all Logs are normalized to 2019M01=0. Sources: BLS, Fed, BEA, calculations from FRED, Macroeconomic Advisers (published 2/28), and authors.

Note that sales in the Industrial Production and Manufacturing and Trading sectors are trending sideways.The belief that a recession is imminent is with me Published January 2019noting that the yield curve is close to inverting.

{kind=link}

{kind=link}