Assume no recession in the US by February 2023. What are the forecasts for maturities and credit spreads, financial conditions indices, debt service ratios?

First, probabilistic regression estimates, 1985-2023M02:

notes: Bold indicates significance at 10% MSL.

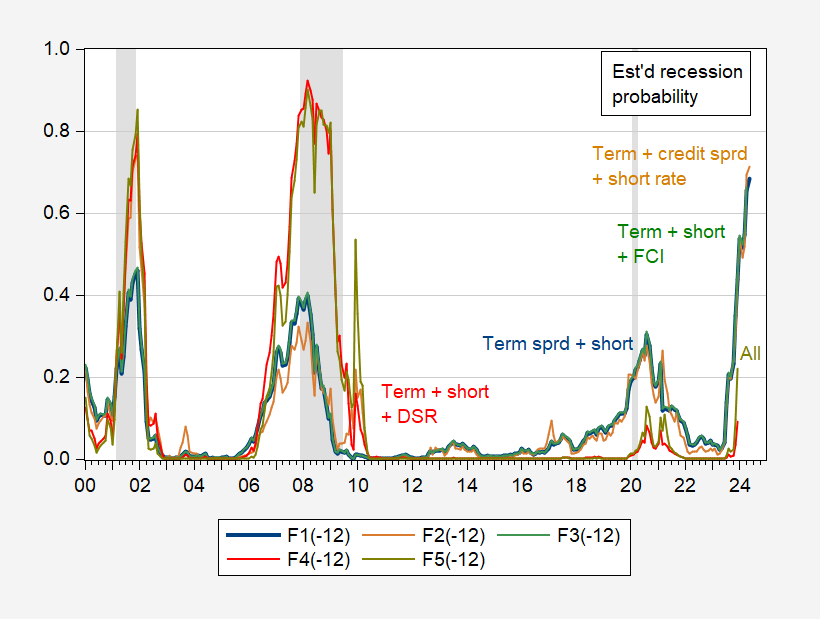

Term spread is 10-year to 3-month Treasury bond spread, short rate is 3-month Treasury bond yield, credit spread is Gilchrist & Zakrajsek (AER, 2012) Excess Bond Premium (EBP), NFCI is Chicago Fed National Financial Conditions Index , DSR is the debt servicing ratio.

Note that adding standard term spreads and short rates with EBP increases the proportion of variance explained, and that EBP has the expected significant sign. Separately, financial stress as measured by the NFCI showed the expected signs and better explained the downturn.Finally, as Borio, Drehmann, and Fan (J. Macro, 2020)the debt service ratio significantly increases the explanatory power of term spreads.

Interestingly, when all three additional financial metrics are summed, only DSR remains statistically significant. The correlation between EBP and NFCI is quite high, whereas DSR is not particularly correlated with EBP and NFCI, so this result is not entirely surprising.

While DSR greatly increases sample fit, it is interesting to consider what this specification means for recession forecasting.

figure 1: Based on term spread plus short rate (bold blue), based on term spread plus short rate (tan), based on term spread plus short rate and NFCI (green), based on term spread plus short rate and DSR (red ) to estimate recession probabilities from term and credit spreads plus short-term rates, NFCI and DSR (yellow-green). Recession peak-to-trough dates as defined by NBER are grayed out. Source: Author’s calculations.

Note that DSR data ends in December 2022, so forecasts based on DSR end in December 2023.

Interestingly, any norm that includes DSR has a much lower probability of recession than the corresponding norm that does not include DSR. For example, the term spread plus short-term rate model suggests a 44% probability by the end of 2023, while a model including all indicators including the DSR suggests a 22% probability.

{kind=link}

{kind=link}