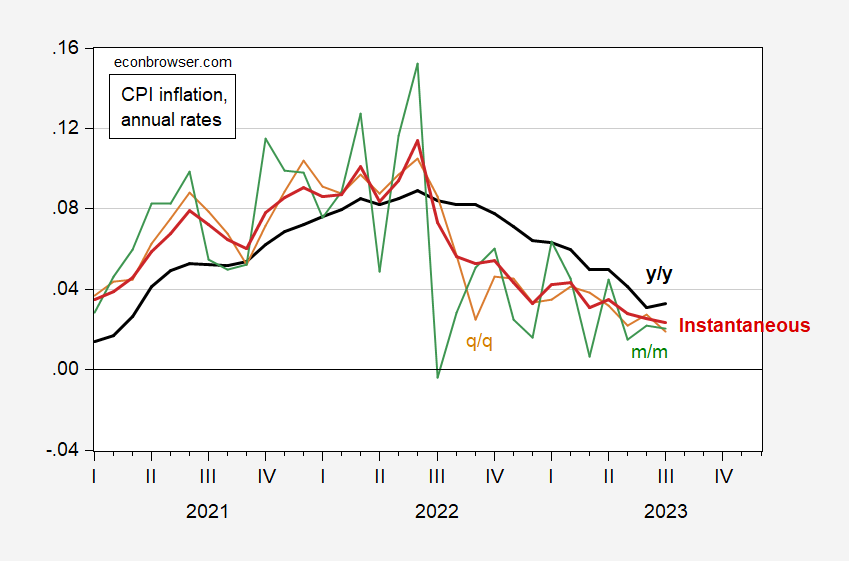

Headline and core year-on-year CPI inflation was slightly below the Bloomberg consensus (0.1%) (below the Cleveland Fed’s immediate forecast of 0.4% mom, see yesterday’s post). Overall, even though the overall year-over-year increase is slight, the trend is still downward.

figure 1: Annualized CPI inflation rate, YoY (bold black), MoM (tan), MoM (green), and instantaneous Eckhout, T=12, a=4 (bold red). Source: BLS and authors’ calculations.

as discussed in Yesterday’s Marketplace article by Justin Ho, the year-on-year calculation does not explain everything. In particular, q/q and m/m fell, as did the instantaneous measure of inflation (essentially a weighted average, weighting more recent m/m inflation).

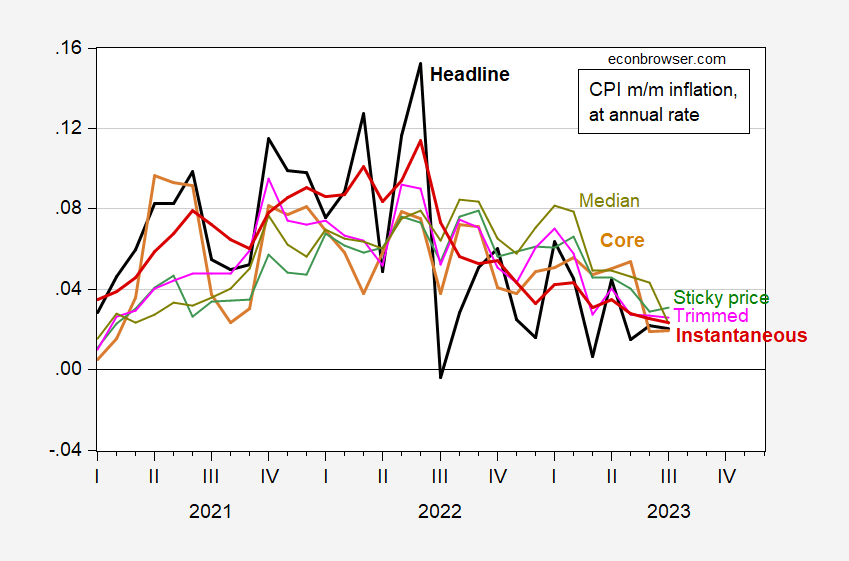

On a monthly basis, other measures that attempt to gauge trend inflation also fell, including the Cleveland Fed’s CPI-adjusted rate and the median rate. The Atlanta Fed’s hold price indicator rose slightly.

figure 2: Annualized MoM headline CPI inflation (bold black), core (bold tan) sticky prices (green), 16% revision (pink), instantaneous per Eckhout, T=12, a=4 (bold red). Sources: Bureau of Labor Statistics, Atlanta Fed, Cleveland Fed, and authors’ calculations.

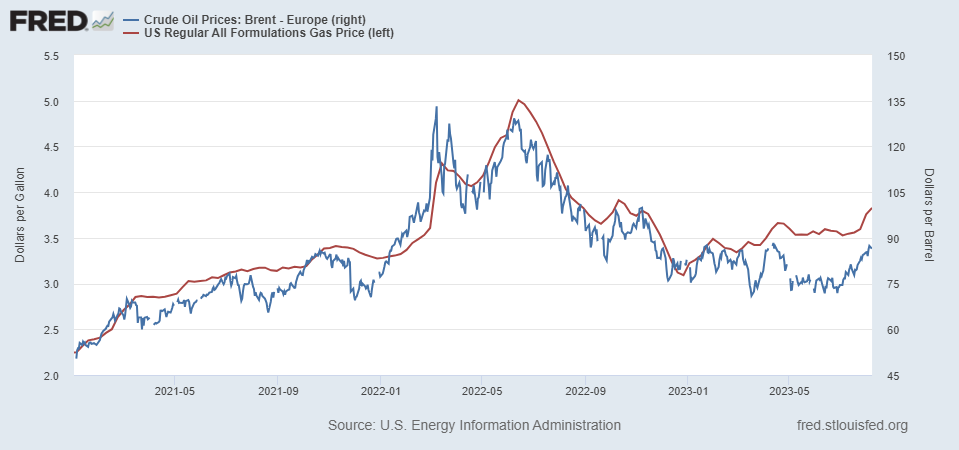

Overall, the launch appears to be largely in line with expectations. Wildcards (short term) may be energy.

Gasoline prices are unlikely to fall much, so the downward pressure on headline inflation is no longer there.

{kind=link}

{kind=link}